PW Consulting: F3 Firefighting Foam Market Poised for Robust Expansion — 11.24% CAGR Projected for 2026–2032

F3 Firefighting Foam Market: Strategic Imperatives for 2026

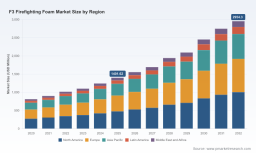

PW Consulting’s new F3 Firefighting Foam Market report provides a decision-grade intelligence package designed to convert regulatory pressure, procurement urgency, and technology evolution into executable strategies for 2026. After five years of rapid adoption and validation activity, the global F3 market is now at an inflection point: from a niche, compliance-driven replacement for legacy PFAS-based foams into a multi-channel, standards-led industrial market. Our analysis—anchored on a 2025 base year—shows the market at roughly USD 1.40 billion in 2025 and growing to approximately USD 1.56 billion in 2026, with a compounded annual growth rate of 11.24% across the 2026–2032 forecast window, and an expected market value approaching the USD 3 billion mark by 2032.

F3 Firefighting Foam Market

Why 2026 Is a Strategic Year for Buyers and Providers

Several simultaneous forces make 2026 a make-or-break year for corporate and public-sector decision-makers:

F3 Firefighting Foam Market

- Regulatory deadlines and prohibitions have shifted from advisory to prescriptive. Key regulatory milestones—spanning defense procurement mandates, civil aviation approvals, maritime exclusions of PFOS-containing foams, and tightened regional chemical restrictions—are compressing timetables for replacement and verification.

- Standards convergence and product certifications have matured. Vendors are now delivering F3 formulations and system approvals that address both mobile/ARFF and fixed-system requirements; certification events in 2025–2026 materially reduce technical uncertainty for high-consequence users.

- Market structure is consolidating around a relatively small set of global technology leaders and strong regional specialists. Our concentration metrics show the top three suppliers account for a meaningful share of commercial spend, while the top five approach a majority position—creating a market where scale, distribution, and certification breadth increasingly determine access to large programmes.

What the Report Delivers: Practical, Executable Intelligence

This is not a theoretical outlook: the report is structured as a toolkit for procurement, operations, and executive teams that must make contractual, capital, and compliance decisions in 2026. Key deliverables include:

F3 Firefighting Foam Market

- Targeted market sizing and scenario modelling—short-, medium- and long-term demand trajectories that map to regulatory enforcement timelines, airfield retrofit cycles, and refinery/fuel-farm asset replacement windows.

- Investment-grade risk maps—jurisdiction-level regulatory risk, liability exposure modelling for legacy AFFF inventories, and a three-tier severity matrix for contamination, remediation, and reputational cost drivers.

- Vendor benchmarking framework—repeatable scorecards that assess certification coverage, proven field performance, supply continuity, formulation maturity, and product lifecycle compatibility with legacy hardware (proportion of systems requiring modification vs plug-and-play replacements).

- Operational transition playbooks—step-by-step protocols for phased agent replacement, rinse-and-commissioning plans for ARFF and fixed-suppression systems, live-training templates, and environmental testing checklists for post-incident sampling.

- Procurement and contract templates—term sheets, performance acceptance criteria, warranty and liability clauses, and supplier qualification checklists tailored for long-tail municipal buyers through multinational energy majors.

- Technology adoption and retrofitting models—capex/opex scenarios juxtaposing full system replacement, hybrid retrofit, and consumable-only strategies over 3–7 year windows.

- M&A and partnership shortlist—data-driven screening of targets and collaborators for strategic buyers seeking to expand geographic reach, certification portfolios, or formulation IP without duplicative R&D spend.

Competitive Landscape: Who Matters and Why

The competitive battlefield is no longer defined purely by chemistry; it now combines certification credentials, channel depth, training capability, and global distribution. Our report profiles the leading global and regional players and synthesises how recent product approvals and launches change procurement dynamics:

- Perimeter Solutions (United States): A commercial leader by virtue of breadth and recent technical approvals. Their SOLBERG EVOLUTION 3% SFFF earning of FM 5130 approval in early 2026 is an inflection event for fixed-system deployability, widening opportunities in hangar and fuel-storage protection where sprinkler compliance has been a sticking point.

- BIOEX (France): An early mover and technical pioneer in fluorine-free formulations with a well-established track record in aviation and military-grade deployments. Their range of aircraft-capable formulations and longstanding certification record make them a reference supplier for policy-driven airport programmes.

- National Foam (United States): Combining product innovation with field training capacity, National Foam’s introduction of low-concentration AR-SFFF options and an active Global Firefighting School creates a differentiated proposition—packaging product supply with operational training and live-fire validation services.

- Angus Fire, Dr. Sthamer, Dafo Fomtec, Oil Technics: Each brings regionally strong product lines with combinations of ICAO/EN/IMO approvals and marine or industrial specialization—critical for multinational buyers that need consistent supply and approval coverage across jurisdictions.

- Hiller, GPS International, HD Fire Protect and other regional players: These suppliers provide important cost and logistics advantages in niche markets—marine, coastal refineries, and municipal procurement programmes where rapid response and local stocking are decisive.

Collectively, the market exhibits moderate concentration: the leading three vendors hold a substantial single-digit-to-low double-digit share of commercial value, and the top five approach a controlling position. For large procurement programmes, supplier qualification now requires both technical proofs and evidence of global production resilience.

Regulatory and Operational Dynamics That Will Shape 2026 Spend

Our dynamics chapter synthesises the hard policy levers transforming demand:

- Defense and aviation procurement: Mandatory phase-outs and DoD/ICAO/MIL-SPEC alignments are accelerating replacement cycles, turning one-off pilots into enterprise-level rollouts.

- Maritime regulation: International maritime prohibitions on certain PFAS compounds in fixed and portable systems drive ship- and platform-level retrofits starting in 2026.

- State and regional bans: Fragmented subnational rules—particularly in high-liability states—create procurement complexity but also concentrated pockets of urgent replacement demand.

- Environmental liability and remediation costs: Organizations holding legacy AFFF inventories face near-term choices around disposal, storage, and documentation—each with balance-sheet implications that our cost models quantify.

How Executives Should Use This Report in 2026

For executives and procurement leaders, the report converts market intelligence into actionable steps:

- Align procurement cycles to certification windows. Where suppliers are achieving new approvals, synchronise purchasing to avoid specification mismatches and costly rework.

- Build hybrid deployment strategies. For high-consequence assets, combine validated F3 agents with targeted hardware retrofits and staged commissioning to keep operational risk within tolerance.

- Contract for performance, not chemistry. Shift supplier contracts toward measurable knockdown, vapor-sealing, and environmental-release performance metrics rather than proprietary ingredient lists.

- Pre-position training and verification budgets. Field performance and operator confidence are critical; include live-fire and in-situ acceptance testing in CAPEX plans to accelerate fleetwide acceptance.

- Stress-test supply chains and liabilities. Use our supplier scorecards and contamination exposure matrices to prioritise vendors for long-term agreements and insurance-backed warranties.

What You Will Not Find in the Press Brief—And Why

Following our “trailer” principle, this announcement highlights strategic insights and the types of granular analysis contained in the full report, but it deliberately omits the proprietary, cell-level segmentation numbers and regional/application-specific revenue breakdowns that buyers rely on for contracting and budgeting. These fine-grained tabulations—essential for bid preparation and capital allocation—are reserved for subscribers and licensed clients who require validated datasets, source-level assumptions, and scenario-specific sensitivity files.

Next Steps: How to Access the Full Intelligence Package

PW Consulting’s F3 Firefighting Foam Market report is designed to be operational from day one. For senior teams preparing 2026 procurement cycles, the report provides the templates, scorecards, and contract language necessary to translate regulation into deliverable programmes. To access the complete dataset, supplier-by-supplier benchmarking, and the downloadable operational playbooks, please consult PW Consulting’s official report page or contact our market-access desk for a brief on how the dataset aligns with your asset portfolio.

Closing Perspective

Transition to F3 is no longer a compliance checkbox; it is a complex programme of technical validation, operational change, and commercial negotiation. With the market growing at an 11.24% compound annual rate across the 2026–2032 forecast window, organizations that combine disciplined procurement, rigorous supplier selection, and field-led acceptance testing will convert transition costs into durable reductions in environmental risk and future liability. PW Consulting’s report equips decision-makers with the strategic roadmap and the operational tools required to lead that transition in 2026—without having to rediscover lessons that early adopters have already learned in the field.

For detailed analysis of this topic, please visit the official page: F3 Firefighting Foam Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.