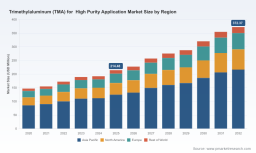

PW Consulting: High‑Purity Trimethylaluminum (TMA) Market Poised to Reach USD 372.37 Million by 2032 on an 8.2% CAGR

Trimethylaluminum (TMA) for High-Purity Applications: Strategic Imperatives for 2026 — PW Consulting Market Brief

Executive snapshot

As the semiconductor, LED, and photovoltaic value chains accelerate advanced deposition and passivation processes, demand for ultra-high-purity trimethylaluminum (TMA) is entering a structurally higher growth phase. PW Consulting’s latest market study — covering historical performance (2020–2025), using 2025 as the base year, and projecting through 2032 — maps the commercial, technical, and regulatory levers companies must act on in 2026. Our analysis projects a mid-single-digit to high-single-digit compound annual growth profile (CAGR 2026–2032) and shows a clear trajectory from a robust 2025 base toward materially larger addressable volumes by the end of the forecast period.

Trimethylaluminum Tma For High Purity Application Market

Why 2026 is a strategic inflection point

-

Technology cadence: Advanced atomic layer deposition (ALD) and metal-organic chemical vapor deposition (MOCVD) process nodes are compressing qualification cycles and increasing precursor purity requirements — raising the bar beyond legacy quality controls.

Trimethylaluminum Tma For High Purity Application Market -

Supply-chain economics: Primary aluminum feedstock volatility and trade policy dynamics are propagating through to TMA unit economics, making procurement strategy and supplier contracting central to margin resilience.

Trimethylaluminum Tma For High Purity Application Market -

Concentration-driven leverage: The market remains concentrated among a handful of large producers, creating both counterparty risk and pricing dynamics that buyers, financiers, and integrators must explicitly price into 2026 plans.

Market trajectory and what it means for 2026 decisions

PW Consulting quantifies the sector’s evolution on a candid, actionable basis. From 2020 to 2025 the market expanded steadily off a solid base, and our forecast through 2032 models continued expansion consistent with an 8.2% CAGR across the forecast window. Practically, this means companies should plan for materially larger procurement volumes, longer qualification pipelines, and higher capital intensity for ultra-pure handling infrastructure over the coming three-to-six years. For procurement and operations teams, the implication is clear: 2026 is the year to move from reactive sourcing to a proactive, scenario-based buying posture.

Competitive landscape: who matters and why

The market’s supplier ecosystem combines global majors with regional specialists. A small set of vertically integrated producers command substantial share and scale, while a growing roster of specialized vendors competes on purity, logistics, and application-specific service. The market concentration metrics underscore this: the top three suppliers collectively exert meaningful influence over the market, while the top five consolidate an even larger portion of supply — a structure that shifts bargaining power, capacity risk, and innovation leadership toward incumbents.

-

Large integrated players bring scale, regulatory experience, and multi-site redundancy that suit high-volume ALD/CVD demand and complex long-term contracts.

-

Specialized high-purity producers differentiate on impurity control, vapor delivery performance, and responsiveness to semiconductor qualification cycles — factors that matter for advanced-node fabs and optoelectronic OEMs.

-

Regional suppliers are leveraging cost and logistical advantages to serve local fabs, but buyers should stress-test qualification timelines and continuity of supply for any regional-only source.

Notable supplier profiles — strategic takeaways

-

Albemarle Corporation: A high-volume producer with multiple high-purity grades and significant production footprint in the U.S., suitable for large-scale ALD and solar supply agreements; offers scale and multi-site redundancy as negotiation levers.

-

Nouryon: Focuses on semiconductor-grade, application-specific TMA solutions and integrated manufacturing — a profile attractive to electronics OEMs demanding consistent ultra-high purity.

-

NAGASE and Dockweiler: Deliver ultra-low-impurity and vapor-phase performance; their strengths are in advanced qualification support and global technical logistics.

-

American Elements, Hunan Heaven, Jiangsu Nata, Argosun, Lake Materials: A mix of global and regional suppliers that broaden the sourcing universe; these firms enable redundancy but require careful due diligence on quality systems and export-compliance.

Supply-chain, raw materials, and regulatory dynamics

Three external dynamics are simultaneously reshaping commercial math and operational risk for TMA stakeholders:

-

Feedstock price pressure: Primary aluminum price moves influence TMA upstream cost. Market participants should model sensitivity to aluminum spot volatility when structuring multi-year supply contracts and pass-through provisions.

-

Regulation and safety compliance: Aluminum alkyls, including TMA, are subject to stringent safety and environmental standards across major jurisdictions. Compliance complexity increases total landed cost and favors suppliers with mature EH&S systems and documented REACH/OSHA track records.

-

Trade and tariff context: Aluminum trade measures continue to affect regional feedstock access and cost profiles, translating into asymmetric cost pressure across producers and geographies. Strategic buyers must account for tariff exposure in origin selection and inventory strategy.

What PW Consulting’s report delivers — practical, executable content

Our market study is built as an executive-to-operational toolkit for leaders making procurement, R&D, investment, and M&A decisions in 2026. Without disclosing the proprietary segmentation tables reserved for the full report, highlights include:

-

Actionable sourcing playbooks — negotiated terms, contract structures, and escalation clauses designed to manage price volatility and continuity risk for high-purity precursors.

-

Supplier prioritization matrix — a decision framework combining capacity, quality systems, geographic resilience, and regulatory compliance to create preferred-supplier portfolios.

-

Technical readiness assessments — checklists and test protocols for qualification of vapor-delivery performance, particulate and metal impurity thresholds, and compatibility with ALD/MOCVD toolsets.

-

Risk & mitigation framework — concentration-risk stress tests, inventory optimization models, and contingency playbooks for material disruptions or geopolitical shocks.

-

Commercial benchmarking — negotiation levers, contract durations, and pricing index approaches tailored to different buyer archetypes (high-volume OEMs, regional fabs, specialty integrators).

-

Investment and M&A scorecards — capability gaps, capex profiles, and integration roadmaps for firms considering vertical integration or strategic minority investments.

Six priority moves for 2026

-

Implement tiered sourcing strategies: Define primary, secondary, and qualified contingency suppliers with explicit qualification timelines and supply ramp triggers.

-

Negotiate price collars and indexed contracts: Protect margins without sacrificing flexibility by embedding transparent pass-throughs for primary aluminum and energy components.

-

Invest in qualification acceleration: Allocate budget to parallelize supplier validation and in-house testing — reduce time-to-qualify by optimizing sample flows and acceptance criteria.

-

Strengthen compliance and audit readiness: Prioritize suppliers with demonstrable REACH/OSHA compliance, robust incident response, and upstream traceability.

-

Run scenario planning on concentration risk: Quantify financial exposure to the loss of a major supplier and model inventory, dual-sourcing, and captive production responses.

-

Leverage strategic partnerships: Consider co-development or long-term offtake arrangements with producers that can scale purity and delivery systems aligned to your roadmaps.

How investors and corporate strategists should react

For investors evaluating materials, specialty chemicals, or semiconductor supply-chain plays, the mid-to-late decade upside is underpinned by technology-driven purity demand and limited new-build feedstock capacity. For corporate strategists, the recommendation is to treat TMA not as a commoditized input but as a strategic raw material requiring cross-functional governance (procurement, process engineering, quality, and legal). Early action in 2026 will unlock disproportionate operational insulation and provide competitive differentiation on wafer yield and product reliability.

Conclusion — the signal in the noise

The TMA market for high-purity applications is maturing into a risk-weighted growth opportunity. PW Consulting’s study provides a pragmatic playbook for 2026 that blends market sizing, concentration analysis, supplier assessments, and operational levers into a single decision-ready resource. While we deliberately reserve detailed segment-level tables and proprietary supplier scoring behind the full report to preserve commercial integrity and client value, the strategic contours are clear: rising purity requirements, concentrated production, feedstock volatility, and tightening regulation make 2026 the year to move from tactical procurement to a strategic, risk-aware sourcing posture.

Next steps

To translate these insights into a 90-day operational plan or a three-year strategic program tailored to your organization, request access to PW Consulting’s full market report and the accompanying implementation annex. Our advisory team is available to run a bespoke workshop that maps the report’s findings to your supplier base, qualification pipeline, and investment priorities.

For detailed analysis of this topic, please visit the official page: Trimethylaluminum Tma For High Purity Application Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.