PW Consulting: Green Geopolymer Concrete Market Poised to Reach USD 41,105.49 Million by 2032 at 25.01% CAGR — Asia Pacific Leads with USD 3,842.9 Million

Green Geopolymer Concrete Market: Strategic Playbook for 2026 — PW Consulting Insights

PW Consulting’s latest market intelligence report on Green Geopolymer Concrete positions the material class not as a niche alternative, but as a strategic lever for decarbonizing construction value chains. Based on a rigorous review of market dynamics through the base year 2025 (historical coverage: 2020–2025) and a forward-looking forecast for 2026–2032, our modelling indicates a sustained compound annual growth rate of 25.01%. The global market (USD, revenue unit: Million) stood at USD 8,620.45 Million in 2025 and is projected to expand to USD 41,105.49 Million by 2032. For corporate leaders planning capital deployments in 2026, these macro trajectories argue for immediate, prioritized strategy work on adoption, procurement, and capability building.

Green Geopolymer Concrete Market

Why this matters for 2026 decision-makers

Green geopolymer concretes combine materially lower embedded carbon with performance attributes—chemical resistance, fire performance, rapid strength gain—that can unlock both sustainability and lifecycle cost benefits. The rapid projected market expansion is being driven by three convergent forces: tightening carbon regulation in developed markets, rising corporate net-zero commitments across real estate and infrastructure developers, and accelerating commercial readiness from material producers. Together these forces create a narrow window in 2026 for first-movers to capture procurement advantages, secure low-carbon precursors, and shape emerging standards.

Green Geopolymer Concrete Market

What PW Consulting’s report delivers — practical, executable intelligence

-

Actionable commercial frameworks: supplier diligence templates, procurement negotiation scorecards, and contract clauses (including quality, supply continuity, and carbon guarantees) tailored to geopolymer precursors and mixes.

Green Geopolymer Concrete Market -

Techno-economic models: comparative capex/opex and lifecycle cost scenarios contrasting geopolymer solutions with OPC-based mixes under different carbon pricing and regulation assumptions through 2032.

-

Pilot-to-scale playbook: blueprinted trial designs, instrumentation and QA/QC protocols, acceptance criteria mapping, and municipality engagement scripts to accelerate approval cycles.

-

Regulatory and standards map: jurisdictional readiness assessment and certification pathways (including fireproofing and structural approvals) with recommended tactics for achieving compliance in priority markets.

-

Risk and mitigation heatmaps: precursor supply volatility, ingredient quality variability, performance uncertainty in extreme environments, and recommended contractual and inventory hedging techniques.

-

Commercial go-to-market templates: target use-cases, stakeholder engagement sequences for contractors and owners, and value communication frameworks for EPCs and asset managers.

Market trajectory and strategic inflections

The forecasted scale-up to over USD 41 billion by 2032 is not linear: adoption accelerates as certification pathways, supply chains and demonstrator projects converge. In practical terms for 2026, this means three near-term inflection points for companies to monitor and act on:

-

Precursor security: securing long-term offtake or strategic inventories of fly ash/slag and alternative precursors to manage feedstock risk.

-

Certification and code integration: investing in or partnering for product certification and approvals to shorten time-to-bid in public and private tenders.

-

Commercial pilots linked to lifecycle economics: structuring pilots so their outcomes feed directly into whole-life procurement decisions rather than isolated technical demonstrations.

Competitive landscape — capabilities that matter

The competitive map shows a mix of specialist technology developers, large building-material incumbents, and vertically integrated new entrants. Market concentration metrics indicate the sector remains fragmented (CR3 and CR5 levels point to material room for consolidation and platform plays). Key archetypes and capabilities that differentiate winners include:

-

Technology-first specialists: companies offering proprietary geopolymer binders or systemized mixes optimized for extreme environments and niche use-cases. Their advantage is rapid product development velocity and deep application know-how.

-

Project-capable integrators: firms that combine mix technology with on-the-ground deployment services, certifications and logistics—reducing adoption friction for contractors and owners.

-

Input-supply differentiators: producers that secure low-carbon precursors through captive positions or long-term partnerships, thereby controlling a key element of cost and carbon intensity.

Representative players include innovators who have commercialized zero-cement mixes and specialty shotcrete, progressive manufacturers partnering on activators and admixtures for approved projects, and regional producers converting industrial by-products into standardized geopolymer precursors. Recent developments—such as certifications for spray-applied fireproofing, model social-housing deployments using earth-friendly mixes, and the launch of zero-cement shotcrete—illustrate how technical validation and project-level visibility are converging to lower buyer risk.

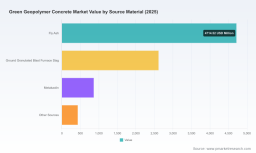

Supply-side dynamics and precursor considerations

Precursor availability and price dynamics are the single most operational risk to scaling geopolymer supply chains. In several jurisdictions, policy measures and industrial trends are already changing the precursor landscape—some markets are seeing policy-driven increases in utilization which improve availability and can depress precursor pricing, while others are experiencing tightening driven by competing uses in ready-mix and legacy markets. For 2026 planning, firms should assume continued regional divergence: some sourcing corridors will be competitive and low-cost; others will require forward contracting, blending strategies or investment in alternative precursors (metakaolin, thermally activated clays, or engineered by-products).

Regulatory drivers and standardization

Carbon pricing mechanisms and border-adjustment frameworks are altering investment math. Where carbon regulation and compliance costs bite, geopolymer solutions gain a valuation premium via avoided emissions. Additionally, approvals from national authorities and recognized certification bodies have begun to de-risk structural and fire-performance claims—opening procurement in regulated social housing and infrastructure corridors. For firms bidding on projects in 2026, proactive regulatory engagement and documented LCA evidence are no longer optional; they are procurement table stakes.

Practical recommendations for 2026 — an 8-point strategic checklist

-

Run three parallel pilots: structural, precast, and sprayed applications—each with clear commercial acceptance criteria and lifecycle cost readouts.

-

Secure precursor optionality: execute a mix of medium-term offtake agreements and strategic inventory to cover project pipelines.

-

Pursue targeted certifications: prioritize fire and structural approvals relevant to your priority markets and use-cases.

-

Build an integrated supply assurance function: combine quality control, logistics planning and supplier development to stabilize mix performance at scale.

-

Price for carbon: incorporate carbon costs into bid models and develop value-capture mechanisms (e.g., green premia, EPC incentives).

-

Partner for scale: leverage alliances with admixture and activator specialists to accelerate mix standardization and reduce on-site variability.

-

Design procurement clauses for variability: include performance-linked payments and remediation paths to manage novel-material risk.

-

Invest in capability uplift: training programs for contractors and inspectors to reduce execution errors and adoption friction.

How PW Consulting supports implementation

Our report is built for doers. Beyond market sizing and scenarios, it includes contract templates, pilot protocols, LCA baselines, and supplier scorecards firms can adapt immediately. Clients receive a tailored workshop to translate the report’s playbook into a 12–24 month operational roadmap aligned with their project pipeline and regulatory exposure.

Conclusion — the 2026 window

The scale-up of green geopolymer concrete is moving from proof-of-concept to procurement reality. With a projected market accelerating at a 25.01% CAGR through 2032, and with headline-scale forecasts indicating a multi‑billion-dollar opportunity by the end of the decade, 2026 is a pivotal year. Firms that convert market insight into procurement commitments, certification pathways, and operational readiness will capture outsized advantage. Firms that wait for broader commoditization risk paying a premium to catch up.

For the detailed segmentation, supplier benchmarking, and downloadable implementation toolkits that underpin this analysis, PW Consulting invites readers to access the full report and client briefings on our source page. The published dataset includes granular forecasts, scenario assumptions, and proprietary models designed to support board-level investment decisions and detailed procurement strategy.

For detailed analysis of this topic, please visit the official page: Green Geopolymer Concrete Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.