PW Consulting: Aluminum Silicate Ceramic Market Poised to Hit USD 1,948.14 Million by 2032, Backed by a 6.12% CAGR

Aluminum Silicate Ceramic Market 2026 Strategic Preview — A PW Consulting Executive Brief

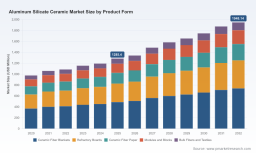

PW Consulting’s latest Aluminum Silicate Ceramic Market report translates five years of historical performance and seven-year forecasts into a decision-grade playbook for corporate leaders planning 2026 actions. The market has expanded materially from the early 2020s and, with a compound annual growth rate (CAGR) of 6.12% across the 2026–2032 forecast window, is projected to approach the upper end of USD scale by 2032. Our analysis combines rigorous market-sizing, scenario-led forecasting, supply-chain risk mapping, and competitor intelligence to provide the tactical instruments executives need to convert market momentum into lasting advantage — while preserving the full granularity of segmentation and proprietary datasets for report subscribers.

Aluminum Silicate Ceramic Market

Why 2026 Is a Strategic Inflection Point

Several converging forces make 2026 a pivotal year for companies exposed to aluminum silicate ceramics. Industrial customers are accelerating investments in energy-efficiency and high-temperature insulation, regulators are tightening emissions and efficiency standards, and advanced manufacturing markets (electronics, power modules, and aerospace) continue to demand higher-performance ceramic components. At the same time, feedstock dynamics and synthetic process dependencies create a pronounced supply-side sensitivity. The net result is a market that is growing steadily, that requires targeted capital allocation, and that rewards proactive supply-chain and product differentiation strategies.

Aluminum Silicate Ceramic Market

What the Report Delivers — Practical, Executable Outputs

- Robust market sizing and trend analysis with a verified historical series and scenario-based forecasts to 2032 (base year 2025).

- A decision-ready strategic framework for procurement, manufacturing footprint, and product roadmap prioritization that senior executives can operationalize within 90–180 days.

- Supply-chain heatmaps and a supplier-risk index linked to feedstock exposure (kaolin, kyanite, bauxite) and synthetic mullite production constraints.

- Competitive positioning matrices and M&A screening criteria tailored to small- and mid-cap consolidation plays.

- Pricing and margin sensitivity models, including hedging and long-term contracting playbooks for raw materials.

- Regulatory impact assessment and low-carbon pathway options (including geopolymer binder adoption) that quantify trade-offs between CAPEX and lifecycle emissions.

- Operational checklists for scaling production, quality control, and certification steps that reduce time-to-market for advanced silicate products.

Interpreting the Numbers: Growth Outlook and Strategic Consequences

Our top-line market model shows clear expansion through the forecast horizon. After a period of recovery and compounding growth in the early 2020s, the industry reached a sizeable market base in 2025; applying the mid-single-digit CAGR to the forecast window demonstrates both the resilience of base industrial demand and the incremental impact of adjacent growth drivers (advanced electronics, electrified transportation thermal management, and retrofit insulation projects). For executives this implies that greenfield investments and brownfield capacity upgrades can be accretive — but only if they are paired with disciplined scenario planning to address cyclical variations and raw-material volatility.

Aluminum Silicate Ceramic Market

Supply-Chain and Raw-Material Dynamics

Aluminum silicate ceramics sit at the intersection of mineral availability and advanced materials processing. The production profile for synthetic mullite and related aluminosilicate formulations depends on kaolin, kyanite, and bauxite inputs, exposing manufacturers to geographic concentration and feedstock price swings. Recent market signals in late 2025 highlighted short-term price movement and moderation in some demand segments, underscoring the need for diversified procurement strategies.

Practical risk mitigations we recommend include securing multi-year contracts with indexation to transparent benchmarks, selective backward integration where volumes and margins support it, and active development of secondary raw-material sourcing pools (including recycled and by-product streams). In parallel, high-priority R&D efforts should target process routes that reduce reliance on the most constrained feedstocks and improve yield per kilogram of input.

Competitive Landscape — Who Matters and Why

The aluminum silicate ceramics market is characterized by a mix of global diversified technical-ceramics leaders, specialized fiber and refractory producers, and regional manufacturers with strong cost positions. The three largest firms account for roughly one-third of the market, while the top five approach roughly half — a concentration profile that shapes M&A and partnership dynamics. Key strategic profiles include:

- CoorsTek Inc. — A global leader in engineered technical ceramics, strengthening capacity and portfolio breadth through targeted facility investment and IP-defense outcomes that expand access to strategic markets.

- Saint-Gobain Ceramics & Plastics (CeramTec grouping) — A broad-based advanced-ceramics producer with deep capabilities in refractory and technical silicates, offering scale and channel reach to industrial end-markets.

- KYOCERA Corporation — A technology-driven player prioritizing high-performance alumina and silicate solutions for electronics and automotive applications; recent facility expansions reinforce its strategic posture.

- Morgan Advanced Materials and CeramTec GmbH — Specialists in insulation and fiber-based products, well-positioned for thermal and refractory applications requiring stringent performance.

- Chinese manufacturers such as Luyang Energy-Saving Materials and Taisheng New Material Technology — Cost-competitive producers of fiber and refractory products, influencing global supply dynamics and serving large regional demand pools.

- Boutique and specialty suppliers (ACM, LSP Industrial Ceramics, C-Mac, International Syalons, Aremco) — These firms supply tailored components and materials for high-value applications and R&D customers.

Recent industry developments reinforce these positions: strategic capacity expansions and new manufacturing lines by several leading producers in 2025–2026 have shifted near-term supply balances and signaled continued confidence in electronics- and industrial-driven demand. For dealmakers, this environment creates opportunities for bolt-on acquisitions to shore up capability gaps and for joint-venture structures to spread capital intensity.

Regulation, Decarbonization, and Market Opportunity

Regulatory frameworks emphasizing energy efficiency and lower emissions are a clear growth vector for aluminum silicate ceramic fibers and high-performance insulation. Additionally, geopolymer binders based on alkali-activated aluminosilicates offer a low-carbon alternative to conventional binders in construction applications — producing materially lower lifecycle CO2 in certain formulations. These forces convert compliance into competitive differentiation for suppliers that can demonstrate verified emissions reductions and circular-material pathways.

Companies that proactively align product development, certification, and customer procurement programs with decarbonization targets are positioned to capture premium contracts from large industrial consumers and infrastructure programs focused on lifecycle performance.

Strategic Recommendations for 2026 Decision-Makers

- Prioritize investment in scalable fiber and blanket capacity where margin capture is highest, but deploy through staged capital projects with clear go/no-go gates tied to order-book signal strength.

- Diversify raw-material sourcing and institute long-term supply agreements indexed to transparent benchmarks; evaluate strategic stockpiles for high-risk feedstocks.

- Accelerate R&D in low-carbon binders and process efficiencies; quantify lifecycle gains for customer propositions and regulatory compliance.

- Pursue targeted M&A to acquire specialty capabilities (e.g., thermal shock resistance, multilayer substrates) that shorten time-to-market for advanced applications.

- Implement a pricing playbook that blends contracted volumes, indexed spot exposure, and value-based pricing for differentiated products.

- Build a certification and quality roadmap to win in regulated and safety-critical markets (aerospace, defense, energy).

- Operationalize scenario planning and rolling 12–24 month stress-testing of capacity and margin under alternative raw-material price and demand-growth assumptions.

How to Use This Report

PW Consulting’s report is designed for senior leaders in strategy, corporate development, procurement, and operations. It provides executable analytics for capital planning, sourcing decisions, M&A screening, and product strategy — together with downloadable models and a repository of vendor profiles and validation checklists. Importantly, the report preserves full segmentation, regional, and application-level detail within proprietary appendices; we intentionally omit those line-item splits in this public preview to protect the analytical integrity of our licensed datasets.

To extract maximum value in 2026, teams should combine the report’s quantitative scenarios with on-the-ground commercial intelligence from sales and supplier partners, and immediately commence the top two actions identified in the report: (1) a 90-day supplier-risk review focused on feedstock concentration, and (2) a 180-day product roadmap aligning R&D investments with low-carbon and high-temperature insulation opportunities.

Conclusion — Turning Forecasts into Advantage

Aluminum silicate ceramics present a compelling, structurally growing market that rewards disciplined capital allocation, proactive supply-chain management, and early adoption of sustainability pathways. With a verified market base entering 2026 and a projected mid-single-digit CAGR through 2032, the strategic imperatives are clear: de-risk feedstock exposure, invest selectively in capability upgrades, and pursue partnerships that accelerate product differentiation. PW Consulting’s full report delivers the data, tools, and scenario models to make those choices with confidence. For access to the detailed segmented tables, regional and application splits, and the complete competitive dataset, consult the full report on PW Consulting’s website.

For detailed analysis of this topic, please visit the official page: Aluminum Silicate Ceramic Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.