PW Consulting: Anechoic Chamber Material Market Projected to Reach USD 1.19 Billion by 2032

PW Consulting Releases Strategic Preview: Anechoic Chamber Material Market Outlook for 2026 Decision-Making

Executive snapshot

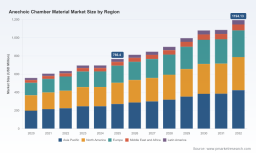

PW Consulting today publishes a strategic preview of our forthcoming Anechoic Chamber Material Market report (base year 2025, historical coverage 2020–2025, forecast 2026–2032). The global market for anechoic chamber materials has demonstrated sustained expansion through the last half-decade and is positioned for steady growth as testing, certification, and defence modernization programs accelerate worldwide. Our top-line findings show the market increased from roughly USD 558 million in 2020 to about USD 766 million in 2025, and under our central forecast it continues to expand at a compound annual growth rate (CAGR) of 6.54% across 2026–2032, trending toward an approximately USD 1.19 billion market by 2032.

Anechoic Chamber Material Market

Why this preview matters for 2026 strategic choices

- Timing capital and procurement: Companies planning chamber builds or absorber upgrades in 2026 face a market that is growing moderately but subject to episodic raw-material-driven cost pressure. The decisions you take this year on procurement windows, supplier qualification, and inventory buffers will materially affect both unit economics and project schedules.

- Technology and compliance alignment: Rapid shifts in test standards, coupled with stricter fire and chemical regulations, mean manufacturers and test labs must balance acoustic and RF performance against certification risk—especially for polyurethane-based absorbers.

- M&A and partnership targeting: With discernible clustering among a small set of established vendors and a mix of specialist and systems integrators, 2026 is a year for selective consolidation or strategic alliances to capture larger turnkey projects in aerospace, defence, and telecom infrastructure testing.

Market trajectory and what it tells executives

The market’s trajectory reflects three reinforcing dynamics: (1) steady demand growth from telecommunications, automotive (including EV and ADAS testing), and aerospace/defence testing programs; (2) technology evolution toward hybrid absorber systems that reconcile broadband performance with fire and environmental regulation requirements; and (3) supply-chain pressure concentrated on polymer feedstocks. Our model—built on bottom-up project pipelines, vendor capacity capture, and scenario stress-tests—shows the market expanding at a mid-single-digit CAGR (6.54%) in the forecast window. That pace creates both margin opportunities for differentiated suppliers and procurement risk where raw-material bottlenecks remain unresolved.

Anechoic Chamber Material Market

Supply‑side dynamics: raw materials, standards and cost inflation

- Polyurethane dependency: Carbon-loaded polyurethane foam remains the dominant substrate for broadband pyramidal and hybrid absorbers. Production of this foam depends on TDI and polyols as key feedstocks. Recent supply constraints in TDI have transmitted price volatility into absorber material cost structures and installation budgets.

- Regulatory overlay: Fire-safety and chemical-content regulations are a persistent gating factor for large builds. ASTM E84 Class A fire performance, REACH/RoHS chemical compliance, and EMC/ immunity standards shape material selection; hybrid designs (polymer + ferrite tiles) are increasingly utilized to meet both electromagnetic performance and regulatory constraints.

- New materials and substitutes: In 2025–2026 the market saw entrants and formulations focused on polypropylene-based absorbers and upgraded foam chemistries targeted at improved fire performance and lower life‑cycle environmental risk. Adoption varies by application and certification needs.

Competitive landscape: structure, leaders and strategies

The sector remains moderately concentrated, with the top three firms accounting for a meaningful share of installed capacity and the top five exhibiting even broader influence—creating a marketplace in which specialist supplier capabilities and turnkey system integrator models coexist. That structure favours firms that can combine absorber formulation expertise with chamber engineering and project management.

Anechoic Chamber Material Market

- Industry specialists with deep materials IP, such as those producing pyramidal, convoluted and hybrid foam absorbers, continue to command premium project pipelines in defence and high-performance telecom testing. These vendors leverage carbon-loaded polyurethane expertise and long-standing engineering relationships with government and prime contractors.

- Systems integrators and chamber builders differentiate via turnkey offerings—combining RF/EMC absorber materials, acoustic treatments, shielding and installation services—winning larger, complex builds where single‑vendor accountability reduces procurement friction.

- Global electronics groups and ferrite manufacturers support testing ecosystems with tile-based and mixed absorber solutions, often used in applications where ferrite-based performance and thermal stability are priority features.

Notable market actors (examples of strategic positioning)

- Long-established absorber manufacturers with specialized foam formulations and turnkey chamber solutions lead in bespoke defense and high-performance telecom applications.

- European and Asia‑based chamber specialists compete on modularity and cost-effectiveness for commercial test labs and component-level measurement rooms.

- Manufacturers that can demonstrate compliance to fire and chemical standards, and who have invested in new material portfolios (including PP‑based or Class‑A certified foams), are capturing specification-conditional orders.

Specific vendor case studies and objective supplier scorecards are included in the full report; the preview omits granular competitive shares here to preserve the integrity of that benchmarking work and to direct buyers to our full deliverable.

Recent developments shaping 2026 procurement windows

- Trade-show technology showcases in early 2026 highlighted advances in absorber geometry and hybrid WAVASORB-style solutions for antenna and propagation testing—these signal vendor readiness to meet next‑generation telecom test specifications.

- New material launches in late 2025 introduced polypropylene RF-absorbing formulations aimed at improved fire behavior and lower environmental impact—an important option for clients constrained by Class A fire requirements.

- Certification achievements in 2025 confirmed that foam formulations can now meet stricter ASTM fire classifications—opening new procurement pathways for facility owners held back by safety mandates.

- Industrial capacity expansions in radar and defense manufacturing have driven opportunistic demand for associated absorber materials, creating localized procurement competition and schedule risk for 2026 projects.

What the PW Consulting report delivers (practical, decision‑ready content)

Clients purchasing the full report will receive hands-on materials tailored for boardroom and procurement teams preparing 2026 strategies:

- Market sizing and validated scenarios: an auditable top-down and bottom-up sizing model across historical (2020–2025) and forecast (2026–2032) periods, including sensitivity runs for raw-material shocks and regulatory tightening.

- Supply-chain maps and vulnerability heatmaps: multi-tier supplier networks for foam, ferrite, and hybrid components, with lead-time and substitution risk scoring to inform inventory and dual‑sourcing policies.

- Regulatory and standards playbook: a compliance checklist (ASTM E84, REACH, RoHS, and relevant EMC standards) and recommended material choices by certification profile.

- Commercial and pricing playbook: margin pocket analysis, suggested procurement clauses for long‑lead raw materials, and contracting templates for fixed‑price versus index‑linked supply agreements.

- Competitive supplier scorecards: technology capability, quality certifications, geographic delivery footprints, and partnership readiness—presented as anonymized benchmarks in the public preview.

- Use‑case roadmaps: customer journeys and buying criteria across major end‑use sectors (telecom, automotive, aerospace/defence, consumer electronics, healthcare) that inform product roadmaps and go‑to‑market prioritization.

- M&A and partnership targets: screening of near-term acquisition or JV targets with commercial rationale for scale, IP, or geographic entry—valuations and integration considerations are included for clients engaging in diligence.

How to use this intelligence in 2026

- Procurement leaders should lock in staged purchase agreements in the first half of 2026 where possible, with indexation clauses tied to polymer feedstock indices and explicit SLA remedies for delivery delays.

- Product and R&D teams must prioritize hybrid absorber formulations and non‑TDI polymer routes to reduce certification friction and raw-material exposure.

- Corporate development should consider targeted acquisitions of niche absorber makers or chamber integrators to gain immediate project backlog and engineering capability, rather than greenfielding capacity.

- Test labs and OEMs should re-evaluate room upgrade timelines against regulatory milestones—Class A fire compliance is already shaping procurement specifications and can be a gating factor for capital projects.

Methodology and credibility

PW Consulting’s analysis is grounded in proprietary primary interviews with material suppliers, chamber integrators, and corporate buyers; triangulated with public filings, trade-show reporting, and confidential deal flow insights. Our market model integrates project-level bill-of-materials, vendor capacity constraints, and macroeconomic drivers. To preserve competitive value for subscribing clients, the preview deliberately omits the granular segment-level figures and supplier rankings—these are available in full with licensing.

Concluding guidance: what to decide in 2026

2026 is a pivotal year for organizations that must align certification timelines, procurement strategy, and product roadmaps. The market is neither hyper‑volatile nor stagnant; it offers predictable growth with episodic supply-side shocks and regulatory events that can amplify cost and schedule risk. Executives who adopt a dual-track approach—simultaneously securing supply for near-term projects while investing in material diversification and strategic partnerships—will convert the market’s steady growth into durable commercial advantage.

To access the full suite of models, supplier scorecards, and actionable playbooks that underpin this preview, visit the PW Consulting report page and request the Anechoic Chamber Material Market report (base year 2025). Our team is prepared to provide tailored briefings for executive committees, procurement teams, and corporate development groups evaluating 2026 initiatives.

For detailed analysis of this topic, please visit the official page: Anechoic Chamber Material Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.