PW Consulting: Marine Bunker Oil Market to Reach USD 274.05 Billion by 2032, Expanding at a 4.72% CAGR (2026–2032)

Marine Bunker Oil Market: Strategic Imperatives for 2026 — PW Consulting Insights

Executive snapshot

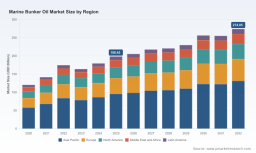

The marine bunker oil market is moving from episodic volatility to structural transition. After rebounding strongly through the early 2020s — with global revenue expanding from roughly USD 120.5 billion in 2020 to about USD 198.5 billion in 2025 — the sector now faces converging pressures from tighter regulation, shifting fuel mixes, and trading/physical bottlenecks. Our new PW Consulting Marine Bunker Oil Market report projects the market to continue growing through 2032, reaching an estimated USD 274.1 billion by the end of the forecast window under a blended CAGR of approximately 4.72% (forecast period: 2026–2032). For executives making capital allocation and supply-chain choices in 2026, this report translates those macro trajectories into actionable commercial, operational and regulatory playbooks.

Marine Bunker Oil Market

Why 2026 is a pivot year

-

Regulatory tightening that came into force in 2025 and early 2026 (notably amendments to MARPOL Annex VI, updated SOLAS flashpoint requirements and revised ISO 8217 specifications) has elevated compliance and testing from back-office hygiene items to frontline operational risks. These changes increase both the cost of non-compliance and the commercial value of reliable, certified supply chains.

Marine Bunker Oil Market -

Supply dynamics are increasingly regionalized. Record-high bunker premiums in Asia and reported refuelling constraints at major ports in early 2026 underscore how port-level logistics and inventory management can materially affect voyage economics and chartering decisions.

Marine Bunker Oil Market -

The product mix is shifting: compliant low‑sulfur fuels (and blends incorporating bio-components) are proliferating alongside traditional residual grades, creating fresh compatibility, testing and emissions-management challenges for ship operators and suppliers alike.

Key implications for corporate decision‑makers

-

Procurement and supplier strategy must become scenario-driven. With average bunker prices across major ports near USD 958/mt in early April 2026 and localized premiums spiking, fixed-price contracts, indexed hedging and diversified supplier panels are no longer optional — they are core risk management instruments. Our report includes scenario matrices that map procurement choices to balance-sheet and P&L outcomes across reasonable price paths.

-

Compliance readiness is now a competitive cost center. The SOLAS and MARPOL amendments have made pre-bunkering declarations and flashpoint verification mandatory in many jurisdictions. Operators who invest in standardized sampling protocols, accredited lab networks and digital chain-of-custody systems reduce voyage delays and avoid punitive consequences.

-

Operational flexibility matters more than ever. Fleet operators face trade-offs between fuel-switching costs, scrubber retrofits, and potential port/route redesigns driven by new ECAs (including recent designations for the Norwegian Sea and the Canadian Arctic). Our analysis quantifies break-even horizons for fuel-conversion investments under multiple fuel-price and emissions-policy scenarios.

-

Commercial contracts should internalize quality risk and interoperability. As biodiesel blends and alternative fuels enter bunkering pools, the probability of incompatibility incidents increases. Contractual templates and supplier scorecards in our report help legal, operations and chartering teams allocate and price that risk.

Competitive landscape: convergence of traders, majors and specialists

The bunker market remains fragmented by supplier counts even as a set of global and regional players exert strong influence. Market concentration at the top end is modest (CR3 approximately 18.4% and CR5 roughly 26.8%), which means there is room for meaningful differential advantage through network reach, product quality, and integrated services.

-

Independent specialists — exemplified by longstanding names such as Bunker Holding, Peninsula Petroleum, Minerva Bunkering and regional independents — continue to compete on agility, port-by-port relationships and tailored logistics. Their strength lies in physical delivery expertise and the ability to marshal trading counterparties quickly in tight supply windows.

-

Integrated majors (Shell Marine, BP Marine, ExxonMobil, Chevron, TotalEnergies) leverage refining and terminal footprints to offer scale, credit and bundled solutions that appeal to large liners and energy-aware buyers. These firms are focusing investment on lower‑emission fuels and expanded bunkering infrastructure to defend long-term global contracts.

-

Commodity traders and specialist groups (Vitol, Trafigura, World Kinect, the regional state-backed suppliers and leading Asian houses) are bridging trading liquidity with logistics, enabling rapid repositioning of volumes while expanding into financing, ship-to-ship services and blended fuel products.

-

Emerging entrants and regional champions — including newly ranked suppliers that broke into top lists in 2025 — illustrate how local market knowledge and niche port coverage can deliver outsized commercial outcomes. Competitive jockeying will increasingly center on digital bunkering offers, compliance attestation, and blended product traceability.

Recent market signals and their strategic weight

-

Bunker House Petroleum’s entry into the top supplier rankings for 2025 signals the rising importance of focused port strategies and the ability to scale local operations quickly.

-

Mandatory declarations on flashpoint compliance and the updated Bunker Delivery Note requirements have turned fuel quality attestation into a gating item for bunkering across many jurisdictions.

-

Regulatory action expanding ECAs and tightening NOx/SOx limits changes route optimization and fuels procurement calculus — both for owners/operators and for the suppliers who serve them.

-

EMSA’s commissioned research into biodiesel‑bunker blends highlights an underappreciated environmental and operational risk vector that will shape product development and liability frameworks over the next three years.

What the PW Consulting Marine Bunker Oil Market report delivers

Our report is designed as a practitioner’s toolkit for 2026 decision cycles. It combines top-down forecasting with actionable, bottom-up modules that translate market movements into implementable steps:

-

Scenario-driven market forecasts (2026–2032) with sensitivity testing against fuel‑price and regulatory shocks, enabling finance teams to stress-test balance-sheet and cash-flow outcomes.

-

Procurement playbooks that include contract terms, hedging templates, supplier pre-qualification checklists and tender evaluation scorecards — all calibrated to minimize delivery disruption and quality risk.

-

Port & logistics diagnostics (node-level assessment methodology) that identify chokepoints in storage, ship-to-ship capacity and last‑mile delivery reliability — critical for voyage planning and strategic inventory placement.

-

Compliance and operations manuals covering sample protocols, chain-of-custody, accredited laboratory networks and digital certification architectures aligned to SOLAS/MARPOL/ISO expectations.

-

Investment & retrofit modelling for fuel conversion, scrubber economics and alternative fuel readiness — providing clear CAPEX/OPEX payback horizons under multiple regulatory scenarios.

-

Competitive playbook profiling the leading suppliers with decision matrices for selecting partners based on credit, footprint, product portfolio and value‑added services (financing, blending, emergency supply).

-

Commercial negotiation aids and post-merger integration checklists for acquirers seeking bolt-on supply networks or terminal positions in strategic hubs.

How executives should use the report in 2026

-

Direct procurement teams to adopt the report’s procurement scorecards immediately and run supplier pre-qualification on any contracts expiring within 18 months.

-

Embed the compliance modules in voyage-operation SOPs to avoid costly port delays and regulatory penalties stemming from flashpoint or documentation shortfalls.

-

Use the scenario and retrofit models to re-evaluate capital plans for fuel-conversion investments; in many instances small changes in price or ECA designation accelerate break-even by years.

-

Leverage the competitive profiles to design an active supplier diversification strategy that blends majors’ scale with independents’ agility and regional specialists’ port access.

Note on data disclosure — the “trailer” approach

This release shares the market trajectory and the strategic implications intended to guide 2026 decisions. Detailed, port-level pricing, full segmentation tables, and confidential supplier performance metrics are intentionally not disclosed here. The full report contains the granular splits, node-level analytics and proprietary scoring that large operators and financiers use for contract pricing, tender design and M&A evaluation. Access to those datasets and appendices is provided through our subscription portal and bespoke advisory engagements.

Conclusion

The marine bunker oil market in 2026 is defined by the interplay of evolving regulation, persistent price pressure in key hubs, and a product mix that is both more complex and more consequential for ship operations than a decade ago. With global market size having nearly doubled from 2020 to 2025 and a projected path to roughly USD 274 billion by 2032 under a mid-single-digit CAGR, firms that move quickly to operationalize compliance, diversify supply, and model fuel-transition economics will capture measurable advantages. PW Consulting’s Marine Bunker Oil Market report maps those choices into concrete actions — from procurement templates and compliance playbooks to investment models and competitive intelligence — enabling executive teams to make confident, defensible decisions in 2026.

Next steps

-

Download the executive report summary and request a demo of the data dashboards at PW Consulting’s insights portal.

-

Contact our advisory team for a 30‑minute briefing tailored to your fleet, port exposure or trading operations.

For detailed analysis of this topic, please visit the official page: Marine Bunker Oil Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.