PW Consulting Forecast: High‑Purity Methyl Acetate Market to Expand at a 5.48% CAGR Through 2032

High Purity Methyl Acetate Market: Strategic Outlook for 2026 — Executive Release by PW Consulting

PW Consulting’s latest market intelligence on High Purity Methyl Acetate is designed for decision-makers who must convert chemical-market signals into decisive corporate action in 2026. This executive release outlines the strategic value of our full report for CEOs, CFOs, Heads of Procurement, R&D leads, and M&A teams. We provide a high-level view of the market trajectory, the critical supply‑side and demand‑side dynamics shaping next‑stage investments, and the commercial playbooks that will matter in a market that remains both technically demanding and commercially attractive. To preserve competitive integrity, this release intentionally excludes the granular regional and application tables contained in the full study — those work products are available on the report page.

High Purity Methyl Acetate Market

Market snapshot and near‑term trajectory

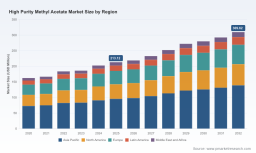

High purity methyl acetate has moved from niche specialty chemical to a strategically relevant solvent and intermediate across coatings, adhesives, electronics cleaning and pharmaceutical synthesis. On a consolidated basis the global market expanded from USD 162.45 Million in 2020 to USD 213.12 Million in 2025, reflecting steady demand recovery and increasing adoption of higher‑specification grades. Our forecast framework projects a continuation of that trend through the forecast horizon (2026–2032) at a compound annual growth rate (CAGR) of 5.48%, taking the market to an estimated USD 309.62 Million by 2032.

High Purity Methyl Acetate Market

Those topline numbers mask a complex mix of drivers: regulatory tailwinds for low‑VOC chemistries, ongoing substitution into precision applications where purity matters, and commercial pressure from feedstock volatility. For corporates planning capex, supply agreements, or M&A in 2026, the key question is not whether the market grows, but how to capture margin and secure high‑quality supply while managing exposure to raw material cycles.

High Purity Methyl Acetate Market

Key market dynamics that will determine 2026 outcomes

-

Feedstock sensitivity and margin pressure: Methanol and acetic acid together represent the dominant portion of production cost for methyl acetate (sector analysis indicates roughly 60–70% of production cost). High‑purity grades require additional purification steps, which amplify input‑price pass‑through and margin variability for producers that cannot secure advantaged feedstock or scale purification efficiently.

-

Recent commodity volatility: Supply disruptions and operating adjustments in China have lifted acetic acid pricing into early 2026. Market reporting in March 2026 showed Chinese acetic acid averages at ~4,140 RMB/ton (a notable move versus late‑March prior levels), supported by higher methanol benchmarks — factors that increase short‑term cost pressure for producers globally and prompt buyers to revisit inventory and hedging strategies.

-

Premiums for high‑purity specifications: End users in pharmaceuticals, electronics, and precision coatings increasingly demand grades with ultra‑low water and impurity profiles. Sector analysis indicates premium pricing bands for high‑purity methyl acetate can be in the 25–30% range versus standard grades. That premium creates a two‑tier market dynamic: investment‑intensive specialist suppliers versus volume‑oriented commodity players.

-

Regulatory advantage: Methyl acetate continues to benefit from VOC‑exempt status under US EPA rules, underpinning demand in environmentally sensitive formulations. This regulatory profile accelerates adoption in low‑VOC coatings and cleaning fluids where performance and compliance must be balanced.

Competitive landscape — strategic positioning and implications

The high‑purity methyl acetate market exhibits moderate concentration. The top three suppliers account for material portions of formal commercial supply, with the top five collectively controlling a majority share — a structure that favors integrated producers and specialist grade providers. Against this backdrop, several supplier archetypes emerge:

-

Integrated, specialty chemical majors — Companies such as Eastman Chemical and Celanese supply high‑purity grades marketed for coatings, adhesives, and pharmaceutical intermediates. Their advantages: downstream formulation know‑how, regulatory certification pipelines, and distribution scale. Eastman’s urethane‑grade product and Celanese’s market positioning as a supplier of the highest‑purity intermediates exemplify this archetype.

-

Global life‑science and analytical suppliers — Merck (MilliporeSigma) and Thermo Fisher serve the ultra‑high‑purity, lab and pharma segments where trace‑impurity control and documentation (e.g., GMP, analytical certificates) are non‑negotiable. These players compete more on technical service, traceability, and logistics than on commodity pricing.

-

Regional large‑scale producers — Companies with integrated acetate value chains (example: large Chinese producers with patented synthesis routes and integrated acetate capacities) can leverage upstream integration to compete on cost while also investing in electron‑ and pharma‑grade purification lines to move up the value chain.

-

Specialty European chemical players — Incumbents such as BASF and Wacker operate in specialty applications and emphasize compliance, technical support, and application development for coating and adhesive formulators.

Strategic implications for incumbents and market entrants are clear: scale alone is insufficient. Control of feedstock, targeted investments in purification and analytical capability, and differentiated go‑to‑market propositions for regulated end‑markets are the levers that will determine winner take‑more outcomes in 2026–2028.

What PW Consulting’s full report delivers (practical, transaction‑grade outputs)

Our full High Purity Methyl Acetate Market report is purpose‑built to inform 2026 capital and commercial decisions. Deliverables include (excerpt):

- Validated market sizing and a 2026–2032 forecast model with scenario toggles (base, downside, upside) and sensitivity to acetic acid/methanol price paths.

- Price‑pass‑through and margin simulation tool that quantifies the impact of feedstock moves on producer EBITDA under alternative purification cost assumptions.

- Supplier scorecards and a capacity heatmap showing certification coverage (GMP, REACH, ISO) and electron/pharma/electronics grade availability across the supplier universe.

- Practical playbooks: procurement hedging templates, supplier qualification checklists for high‑purity purchases, and a regulatory compliance matrix tailored to coatings, electronics, and pharma uses.

- M&A and partnership shortlist with commercial rationale, integration risk checklist, and expected synergy ranges — including bolt‑on and capacity consolidation scenarios.

- Commercial go‑to‑market strategies for both producers and distributors: account segmentation, margin waterfall design, and premium capture tactics for high‑purity positioning.

To respect competitive sensitivity, the granular regional and application‑level breakout tables, price curves, and supplier‑level volumes are retained for report subscribers and are not reproduced in this release.

Priority strategic recommendations for 2026

-

Lock in feedstock exposure. Given the outsized share of production cost held by methanol and acetic acid, buyers and producers should revisit forward purchase agreements, index‑linked contracts, and blended sourcing strategies to stabilize input cost volatility during 2026 market dislocations.

-

Invest selectively in purification capability. Producers targeting premium segments should prioritize investments in advanced distillation, adsorption and analytical QC systems to protect margin and meet pharma/electronics documentation requirements.

-

Differentiate through regulatory positioning. Use methyl acetate’s VOC‑exempt status to co‑develop low‑VOC solutions with formulators and to drive specification switches where performance parity exists.

-

Prioritize strategic partnerships over broad expansion. For mid‑sized players, joint ventures with upstream acetate producers or tolling agreements with certified purification specialists can unlock access to premium demand without full greenfield capex risk.

-

Adopt scenario‑led capex planning. Develop at least three capex scenarios linked to commodity price paths and premium capture rates; only proceed with high‑capex projects where payback is demonstrated under conservative margins.

-

Prepare M&A playbooks focused on niche purity leaders. Consolidation opportunities exist where small specialist producers, with certified grades and client lists in regulated industries, can be integrated into larger platforms to scale margins and distribution.

Why this report matters for boards and operating committees in 2026

The convergence of sustained demand growth (our model projects a multi‑year CAGR of 5.48% through 2032), feedstock uncertainty, and segmental premium opportunities creates a narrow window in 2026 for value creation. Companies that align procurement, technical investment, and commercial strategy now will be able to convert structural premium channels into durable margin expansion while mitigating the downside of commodity cycles.

PW Consulting’s report turns macro trends into executable interventions: quantifiable margin protection tactics, supplier selection frameworks for high‑purity procurement, and M&A playbooks tested across price and demand scenarios. For corporate executives who must prioritize a small set of high‑impact bets, the report provides both the numbers and the road map to act.

Next steps

Executives seeking the full dataset, detailed regional and application breakouts, supplier volume tables, and access to the interactive sensitivity model should consult the PW Consulting report page for subscription and licensing details. Our advisory team is available to provide tailored briefings, model walkthroughs, and bespoke diligence for planned transactions or capex projects in 2026.

PW Consulting — turning chemical market complexity into strategic advantage.

For detailed analysis of this topic, please visit the official page: High Purity Methyl Acetate Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.