PW Consulting Forecast: Glycerophosphoric Acid Calcium Salt Market to Hit USD 347.27 Million by 2032 at a 5.42% CAGR, Led by Asia‑Pacific’s USD 83.9M in 2025

Glycerophosphoric Acid Calcium Salt Market: Strategic Insights for 2026 Decision-Makers

PW Consulting’s latest market briefing on the Glycerophosphoric Acid Calcium Salt (commonly referred to as calcium glycerophosphate) market delivers a pragmatic roadmap for executives making portfolio, sourcing, and regulatory decisions in 2026. Anchored in a comprehensive assessment covering the historical window 2020–2025 (base year 2025) and a detailed forecast to 2032, this analysis combines macro growth metrics with operational playbooks designed to convert intelligence into near-term actions.

Glycerophosphoric Acid Calcium Salt Market

Executive snapshot: why this matter now

-

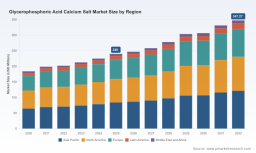

The market has demonstrated steady expansion from an estimated USD 184.15 Million in 2020 to approximately USD 240.0 Million in the base year 2025, reflecting resilient end-market demand across nutrition, oral care, and pharmaceutical applications.

Glycerophosphoric Acid Calcium Salt Market -

PW Consulting’s forecast model projects continued growth through the 2026–2032 horizon, with a compound annual growth rate (CAGR) of 5.42%, culminating in a market size above USD 340 Million by 2032. This trajectory implies recurring, addressable opportunities for suppliers, formulators, and ingredient innovators.

Glycerophosphoric Acid Calcium Salt Market -

Market concentration is moderate: the top three firms account for roughly two-fifths of supply and the top five approach just over half of the market, a structure that creates both consolidation opportunities and tactical niches for differentiated entrants.

What the 2026 strategist needs from a market report

In our conversations with C-suite and business unit leaders, three needs consistently surface: reliable macro sizing to justify investment, pragmatic segmentation to direct commercial effort, and executable supply/regulatory playbooks that reduce time-to-market. This report is deliberately crafted around those priorities:

-

Verified market sizing and growth scenarios (base year 2025; forecast period 2026–2032) with sensitivity analyses under alternative demand and pricing trajectories.

-

Actionable segmentation frameworks that prioritize go-to-market choices by application-grade and channel economics—without exposing proprietary split tables in this release; full segment-level detail is available in the subscription report.

-

Supplier and customer mapping that connects competitive positioning with contract levers, lead times, and certification footprints necessary for pharmaceutical, nutraceutical, food, and oral-care pathways.

-

Regulatory monitoring and risk matrices aligned to recent developments, including food additive status and pharmacopeial compliance, plus mitigation strategies for cross-border market access.

Market trajectory and drivers

The market’s upward trend to USD 240.0 Million in 2025 reflects several converging dynamics: sustained demand for calcium fortification in specialty nutrition and supplements, renewed investment in evidence-backed oral-care actives for anti-caries and anti-plaque claims, and the ongoing use of calcium glycerophosphate in targeted pharmaceutical formulations. Our forecast to 2032 presumes a continuation of these drivers, with expected CAGR at 5.42% under the baseline scenario.

Key demand catalysts we tracked include: product innovation in infant and functional nutrition, formulary substitutions where organoleptic or bioavailability advantages matter, and regulatory confirmations that reduce commercialization friction for food and cosmetic uses. The 2026 regulatory environment is particularly supportive: recent affirmations of GRAS status and ongoing recognition in compendial sources reduce compliance costs for many applications—while still placing a premium on suppliers who can demonstrate consistent pharmacopeial or GMP credentials.

Competitive landscape — who matters and why

The competitive field blends specialized manufacturers with regional exporters and branded ingredient houses. Core market players we profile in the full report include: Global Calcium Pvt Ltd, Bihani Chemical Industries Pvt. Ltd., Dr. Paul Lohmann GmbH & Co. KG, ISALTIS (France), NutriScience Innovations (USA), and several established chemical suppliers based in North America and India. These participants differ on three strategic dimensions:

-

Regulatory and quality positioning — Some firms emphasize pharmacopeial compliance and pharma-grade certifications (e.g., USDMF, EU-GMP, ANSM GMP), enabling access to infant nutrition and pharmaceutical formulations; others compete on cost and food-grade credentials for large-volume fortification use-cases.

-

Format and technical differentiation — Manufacturers supply dry powders, concentrated solutions, and specialized grades tailored for oral-care or infant nutrition. Players offering a broad grade set (pharmaceutical, food, oral-care) are better positioned to capture cross-segment demand.

-

Supply-chain reach and customer intimacy — Global exporters from India, specialty producers in Europe, and branded suppliers in the U.S. form a complementary geography of supply. Companies with certified manufacturing sites and traceable quality systems command price and contract advantages among regulated customers.

Notable recent developments that change the strategic calculus include ISALTIS’s product listing update (Nov 2025) adding an anti-plaque cosmetics application, indicating an evolution of oral-care use-cases, and a February 2026 update to the FDA food-substance database confirming GRAS status in common food matrices. These moves reduce commercialization tail risk for food and cosmetic claims but raise the bar for suppliers to substantiate GMP-level quality where required.

Regulatory and raw-material dynamics

A practical element of our analysis is the mapping of regulatory clarity to commercial opportunity. Calcium glycerophosphate is affirmed as GRAS under U.S. federal regulations for nutrient supplementation when produced under good manufacturing practice. It also aligns with Food Chemicals Codex specifications as a direct food substance. On the manufacturing side, the salt is typically produced by neutralizing glycerophosphoric acid with a calcium source (e.g., calcium hydroxide or calcium carbonate)—a process detail that influences capital intensity, impurity profiles, and supplier selection.

For 2026, companies should prioritize suppliers with documented compliance to local pharmacopeias and, where applicable, certifications such as EU-GMP or ANSM pharma GMP. This approach reduces time-to-qualification for premium channels (infant nutrition and pharmaceuticals) and allows buyers to extract margin premiums or win innovation partnerships.

Strategic implications and prioritized actions for 2026

PW Consulting recommends a three-tiered decision framework for 2026 planning horizons: Secure, Differentiate, and Scale.

-

Secure (Q1–Q2 2026)—De-risk supply and regulatory exposure. Undertake dual-sourcing for critical grades, audit supplier quality systems against relevant pharmacopeias, and codify change-control requirements into contracts. This is especially critical given the moderate market concentration: the top suppliers control meaningful share, and single-source dependence creates negotiation vulnerabilities.

-

Differentiate (Q2–Q4 2026)—Invest in grade and application differentiation. Where feasible, co-develop application-specific grades (e.g., mouth-care optimized formulations or low-impurity pharma grades) with suppliers that hold GMP or USDMF dossiers. Marketing claims enabled by third-party certifications—backed by targeted clinical or laboratory evidence—unlock premium positioning in crowded supplement and oral-care categories.

-

Scale (2026 onward)—Prioritize scalable routes to market. For growth-oriented players, leverage contract manufacturing partnerships that allow capacity expansion without full greenfield investments. Consider bolt-on acquisitions to secure upstream feedstock or downstream formulation capabilities if price arbitrage and integration synergies are validated by due diligence.

Commercial playbooks — go-to-market, pricing, and contracting

Our fieldwork and procurement interviews highlight practical levers buyers and sellers can deploy in 2026:

-

Price-indexed contracts that blend fixed and variable elements to account for feedstock volatility and preserve margin on both sides.

-

Certifications and traceability requirements embedded into master supply agreements to shorten qualification cycles for regulated customers.

-

Co-marketing and technical-support clauses for supplier partners that co-invest in evidence generation for specialty claims (e.g., anti-plaque efficacy or infant nutrition bioavailability).

How PW Consulting’s report converts insight into action

The full report is structured to move teams from information to implementation. Modules include quantitative demand models (scenario-based sizing to 2032), detailed segmentation matrices with commercial and margin overlays, supplier dossiers with capability heatmaps, regulatory watchlists tied to commercial risk, and an executable playbook for procurement and product leadership. Importantly, the segmentation and channel economics sections are designed to be operational: sample scorecards, supplier shortlists, and a baker’s dozen of negotiation tactics tailored to grade and application.

We intentionally refrain from publishing granular segment percentages and proprietary contract templates in this public bulletin to protect the commercial value for subscribers. Those detailed matrices are available through the report portal and are essential for teams preparing FY-2026 budgets or tactical sourcing events.

Conclusion — what to prioritize in 2026

Calcium glycerophosphate represents a stable, growing ingredient market with attractive niches for companies that can combine certified quality, application-specific technical support, and flexible sourcing strategies. The base-year sizing and a 5.42% CAGR to 2032 underscore a market that is neither speculative nor static—there is room for sustained product innovation and disciplined consolidation.

For 2026, the single most impactful steps are: lock down compliant, auditable supply for regulated channels; invest selectively in product differentiation backed by third-party certification and evidence; and structure commercial agreements to preserve optionality while aligning incentives across the value chain.

Next steps and how to access the full intelligence

PW Consulting has packaged the complete analyses, supplier profiles, regulatory dossiers, and executable playbooks into a single market report optimized for strategic and commercial teams. To access the full dataset—complete segmentation tables, supplier scorecards, and contract templates—visit our report page or contact your PW Consulting representative. For decision-makers preparing operating plans for 2026, this report is built to shorten the path from insight to action.

For detailed analysis of this topic, please visit the official page: Glycerophosphoric Acid Calcium Salt Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.