PW Consulting: SiC and TaC Coated Graphite Market Poised for Rapid Expansion — 11.2% CAGR Projected Through 2032

SiC and TaC Coated Graphite Market: Strategic Imperatives for 2026 — PW Consulting Industry Brief

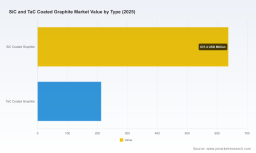

PW Consulting’s latest market research on SiC and TaC coated graphite delivers a practical, decision-ready perspective for executives preparing strategic moves in 2026. Built on an expanded historical series (2020–2025) and a detailed forecast window (2026–2032), the study synthesizes market-size trajectories, competitive structures, supply-chain vulnerabilities, and executable go-to-market options. Our analysis shows sustained expansion driven by semiconductor and compound‑semiconductor manufacturing growth: the global SiC and TaC coated graphite market rose from USD 512.14 Million in 2020 to USD 850.00 Million in 2025, and is forecast to reach USD 1,787.12 Million by 2032 — a compound annual growth rate (CAGR) of 11.2% across the 2026–2032 forecast horizon.

SiC and TaC Coated Graphite Market

Key macro takeaways

-

Robust market expansion: After rapid recovery and growth through 2020–2025, the market enters a high-growth phase driven by accelerating demand in high-temperature and epitaxial processing equipment. Our forecast models indicate sustained double‑digit growth at an 11.2% CAGR through 2032.

SiC and TaC Coated Graphite Market -

Consolidated supplier base: Market concentration is meaningful — the top three and top five suppliers together account for a dominant share of supply — reinforcing that incumbent suppliers with validated coating processes and qualified customer relationships maintain structural advantages.

SiC and TaC Coated Graphite Market -

Supply-chain sensitivity: Tariff actions and raw-material policy moves are material near‑term risk factors that can alter landed costs and supplier competitiveness as of 2026; companies should model tariff scenarios and raw-material availability into procurement and pricing strategies.

-

Technology and product differentiation matter: SiC and TaC coatings are not commodities — proprietary CVD processes, coating uniformity, adhesion, and tailored geometries are primary determinants of customer qualification and lifetime value.

Why this report matters for 2026 decision‑makers

-

Capital allocation and capacity planning: The market size trajectory and scenario outputs enable CFOs and plant planners to justify or defer capital investments with a clear view of mid‑cycle and structural demand. With the market nearly doubling across the forecast period, incremental capacity investments can yield attractive payback — if timed and targeted correctly.

-

Supplier and technology selection: Procurement leaders will find our supplier benchmarking and qualification matrices useful when designing multi‑source strategies that balance cost, qualification time, and technical performance. The study highlights which technical differentiators shorten qualification cycles and which supplier investments (e.g., CVD capacity, process control) materially reduce incumbent lock‑in risks.

-

M&A and partnership playbooks: For corporate development teams, the research identifies pockets of consolidation opportunity and the commercial levers that increase enterprise value — from vertical integration of coating capabilities to bolt‑on acquisitions that broaden process portfolios or increase regional footprint.

-

Regulatory and tariff scenario planning: With a reinstated tariff landscape affecting both natural and synthetic graphite inputs, the report equips legal, trade, and sourcing teams with scenario analyses that quantify tariff impact on unit economics and recommend hedging and near‑sourcing responses.

Competitive landscape — who matters and why

The competitive picture combines legacy materials specialists, integrated graphite players, and a growing set of regional coatings specialists. Incumbents with long qualification histories and validated CVD capabilities continue to set the bar for performance and purity, while smaller, agile firms compete on customization, lead time, and price.

-

Toyo Tanso Co., Ltd. (Japan) — A leading CVD‑coating practitioner offering SiC and TaC product families. Their announced capacity expansion for TaC products reflects a strategic emphasis on higher‑temperature applications where TaC’s superior heat resistance is valued by advanced device manufacturers.

-

SGL Carbon (Germany) — Known for industrial scale and a strong pedigree in SiC coated graphite for wafer processing and crystal growth; competitive advantage lies in integrated materials know‑how and global manufacturing footprint.

-

Schunk Xycarb Technology (Schunk Group) (Netherlands/Germany) — A major supplier to microelectronics with broad product coverage across susceptors, carriers, and consumables; their scale and product breadth make them a preferred partner for larger OEMs.

-

Mersen (France), Semicorex (China), Semicera (China), VeTek (China), SIAMC Advanced Materials (China) — These suppliers represent a mix of global OEMs and regional specialists that win business through local responsiveness, tailored engineering services, and competitive lead times.

-

US-based suppliers (e.g., Stanford Advanced Materials, MWI, Bay Carbon) — Provide geographically proximate supply and specialized product lines that reduce qualification friction for North American customers.

Recent strategic moves underscore evolving dynamics: Materion’s acquisition of tantalum manufacturing assets (completed mid‑2025) signals investor interest in complementary refractory and coating businesses, while Toyo Tanso’s earlier capacity expansion highlights differentiated product strategy focused on high‑temperature TaC demand. Taken together with tariff and raw‑material developments, these moves create both risk and opportunity for incumbents and new entrants alike.

Market risks and regulatory context

-

Tariff environment: A 25% tariff on natural flake graphite scheduled to take effect in January 2026 — combined with an existing 25% tariff on certain synthetic graphite inputs — materially affects landed cost structures. Firms should reassess sourcing, near‑sourcing, and inventory strategies in light of these measures.

-

Raw‑material concentration and quality variance: Dependence on specific graphite feedstocks leads to variability in coating performance and qualification cycles; tighter upstream controls and supplier audits will be increasingly important.

What the report contains — practical, actionable modules

PW Consulting’s deliverables are structured to be directly operationalized by strategy, procurement, product, and BD teams. The report includes:

-

Market sizing and forecasting with transparent methodology — historical series (2020–2025) and scenario‑based forecasts to 2032, underpinned by equipment‑level demand drivers.

-

Supplier benchmarks and qualification playbooks — comparative assessments of coating technologies, process control capabilities, qualification timelines, and service models.

-

Supply‑chain risk maps — tariff sensitivity analysis, raw‑material dependency charts, and logistics stress tests with mitigation options.

-

Go‑to‑market templates — pricing levers, lead‑time optimization, and OEM engagement tactics tailored to different customer archetypes.

-

M&A and investment frameworks — valuation levers for acquisition targets, synergy tests, and integration checklists focused on coating assets.

-

Technology roadmaps and product transition scenarios — guided pathways for investing in TaC vs SiC capabilities, retrofit strategies for existing fleets, and R&D prioritization matrices.

Strategic recommendations for 2026

-

For suppliers: Prioritize qualification speed and reproducibility. Invest in process analytics, standardized qualification packages, and customer‑collaborative testbeds that shorten approval cycles and justify premium pricing.

-

For OEMs and fab‑owners: Build flexible sourcing arrangements with layered supply — a primary qualified partner, a validated secondary source, and local buffer stock — to insulate throughput from tariff or shipping shocks.

-

For investors and acquirers: Target assets that expand coating capabilities (e.g., TaC CVD lines) or provide margin uplift through value‑added services (repair/repair‑and‑return, refurbishing, and loyalty programs). Integration playbooks should focus on cross‑selling into established OEM relationships.

-

For procurement teams: Run immediate tariff impact simulations and renegotiate long‑lead contracts where indexation or pass‑through clauses are absent. Consider near‑sourcing or inventory hedging for the 2026 tariff inflection point.

How to use the full PW Consulting report

This briefing is a strategic preview: it presents the macro trajectory, competitive contours, and practical levers that matter in 2026. The full report contains granular data, proprietary segmentation, vendor scorecards, and downloadable financial models that enable scenario testing and bespoke decision support. We intentionally withhold core sub‑segment and regional granularity here to preserve the strategic value of the full dataset and models accessible from PW Consulting’s report page.

Executives planning capital deployment, supplier selection, or M&A activity for 2026 will find that the report converts market intuition into executable tactics — from which assets to prioritize for capacity expansion, to how to structure supplier agreements that survive tariff and raw‑material shocks. For detailed tables, segmentation breakdowns, and the interactive forecast model, please consult the full SiC and TaC Coated Graphite Market report available from PW Consulting.

Contact PW Consulting’s Advanced Materials practice to request an executive briefing, bespoke scenario modelling, or supplier due diligence packages to support your 2026 decision cycle.

For detailed analysis of this topic, please visit the official page: SiC and TaC Coated Graphite Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.