PW Consulting Report: Amorphous Metal Sheets Market to Reach USD 4.10 Billion by 2032 at 9.4% CAGR — Asia Pacific Commands $1.16B Share

Amorphous Metal Sheets Market: Strategic Intelligence for 2026 Decision-Making

PW Consulting's new market brief on the Amorphous Metal Sheets market crystallizes the sector's fast-moving dynamics and delivers practical, decision-ready analysis for corporate leaders planning 2026 initiatives. Building on a rigorous historical review (2020–2025) and a seven-year forecast horizon (2026–2032), the report situates amorphous metal sheets within the intersecting cycles of electrification, industrial efficiency, and supply-chain geopolitics.

Amorphous Metal Sheets Market

Why this report matters for 2026

-

Clear macro trajectory: The global market expanded from USD 1,390.22 Million in 2020 to USD 2,185.40 Million in 2025, and PW Consulting projects continued expansion at a compound annual growth rate (CAGR) of 9.4% through the 2026–2032 forecast window. By 2032, we estimate the market will approach USD 4,099.1 Million (USD Million basis).

Amorphous Metal Sheets Market -

Strategic inflection: 2026 is a pivotal year—policy moves, tariff shifts, and material-technology releases will materially influence sourcing, capital allocations, and product roadmaps. Executives who align procurement, R&D, and market entry timing to these inflections will capture disproportionate value.

Amorphous Metal Sheets Market -

Consolidation and concentration: The market exhibits meaningful concentration (CR3 ~58.4%; CR5 ~72.15%), indicating that a small set of suppliers controls the majority of capacity and technology pathways. This asymmetry shapes supplier negotiation power, M&A optics, and strategic partnership design.

What we analyzed—and what we deliberately withhold

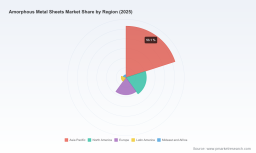

The report synthesizes primary interviews, plant-level capacity assessments, vendor product roadmaps, material science advancements, and macro-policy overlays to produce actionable recommendations. To maintain a “trailer” approach—demonstrating the depth of our work while encouraging access to the full dossier—we surface high-confidence, decision-relevant insights but intentionally withhold granular subsegment revenue splits and detailed regional/application breakdowns. These proprietary subsegment tables and scenario worksheets are available in full through PW Consulting’s report portal.

Core findings: market dynamics and drivers

-

Demand drivers: Growth continues to be driven by energy-efficiency adoption (transformers and motors), electrified transportation, and expanding power-electronics footprints in industrial and consumer applications. The value proposition—lower core losses and higher permeability relative to many crystalline alternatives—underpins long-term replacement and new-build demand.

-

Supply-side developments: Rapid solidification metallurgical routes (primarily iron-based alloys with boron and silicon additions) remain the dominant production technology. Capacity investments by major regional producers are accelerating, creating a near-term oversupply risk in certain segments while shifting bargaining dynamics in others.

-

Policy and trade shocks: Regulatory incentives for CO2 reduction and energy efficiency favor amorphous materials, but trade measures introduced in 2026—most notably strengthened tariffs on metal products—introduce a bifurcated outcome for global sourcing strategies. Firms will need to model landed-cost sensitivity to tariff scenarios when setting sourcing and localization plans.

Competitive landscape: who sets the pace

The sector combines established global leaders, vertically integrated regional champions, and technology-driven niche specialists. PW Consulting’s competitive map identifies three broadly distinct supplier archetypes: high-volume producers focused on power distribution cores; advanced-materials firms commercializing bulk metallic glass and precision components; and vertically integrated players targeting large industrial customers and OEM partnerships.

-

Metglas Inc. (Conway, SC, USA) — Market-leading capabilities in amorphous ribbon and sheet production via rapid solidification. Strengths include proven transformer and motor applications, deep IP on ribbon metallurgy, and established customer relationships in power equipment manufacturing.

-

Proterial, Ltd. (Tokyo, Japan) — A major player in laminated and bonded amorphous ribbon technologies, with recent product development focused on high-density motor core materials for xEV drivetrains. Proterial’s engineering-led go-to-market is tailored to OEM co-development agreements.

-

VACUUMSCHMELZE GmbH & Co. KG (Hanau, Germany) — Specialist in high-permeability Fe- and Co-based amorphous materials and stamped parts for precision electronics and power applications. VAC’s strength lies in application engineering and delivering stamped and formed parts at scale.

-

Key China-based manufacturers (Qingdao Yunlu, AT&M, SAT, others) — These firms combine scale investments with cost competitiveness and are increasingly moving up the value curve through capacity expansion and quality upgrades to serve distribution transformer and motor markets.

-

Precision and BMG specialists (Heraeus Amloy, Amorphology, Liquidmetal, Orbray) — Focused on bulk metallic glass processing, injection molding, and high-precision components for aerospace, medical, and specialty industrial applications. Their innovations unlock new use-cases where strength-to-weight and corrosion resistance are critical.

Recent strategic moves reinforce these dynamics: Qingdao Yunlu commissioned major new ribbon production lines in August 2024 to expand capacity substantially; Proterial launched a laminated bonded amorphous ribbon for high-efficiency xEV motor cores in May 2024; and LightPath Technologies completed an acquisitive step into amorphous materials processing in January 2026. Each event alters capacity balance, technology trajectories, or capability portfolios, and should be stress-tested in procurement and partnership scenarios.

Risk vectors and scenario planning

-

Tariff and trade risk: In April 2026, U.S. trade policy adjustments increased tariffs on metal products and derivatives. Buyers and suppliers must evaluate three scenarios—status quo, escalatory tariff regime, and negotiated tariff relief—and quantify their impact on landed costs, lead times, and total cost of ownership for amorphous sheet-based assemblies.

-

Raw material and upstream stability: Iron-based amorphous alloys rely on steady availability of metallurgical feedstocks; global crude steel production trends through late 2025 suggest stable upstream availability, but localized disruptions or price spikes in alloying metalloids (e.g., boron) could compress margins.

-

Technology substitution risk: While amorphous sheets are favored for efficiency, competing low-loss crystalline alloys and soft magnetic composites are advancing. OEMs should quantify lifetime energy savings against premium material cost and assembly complexity to determine adoption thresholds.

-

Concentration and supplier risk: High CR3/CR5 concentration metrics indicate procurement exposure to key suppliers. Diversification strategies—dual sourcing, backward integration, and long-term offtake contracts—are pragmatic mitigants.

Actionable recommendations for 2026

-

Prioritize TAR (Total Acquisition & Retention) modeling: Integrate tariff-probability-weighted scenarios into supplier selection and capital budgeting. For high-volume applications (e.g., distribution transformers, motor cores), a 3–5% shift in landed cost can justify reshoring or joint-venture investments.

-

Pursue hybrid supply strategies: Combine relationships with high-quality global leaders and capable regional producers to balance cost, security, and innovation access. Where possible, secure long-term offtake agreements tied to collaborative R&D milestones.

-

Embed materials intelligence into product roadmaps: Product managers should develop parallel design-for-amorphous and design-for-crystalline architectures to preserve optionality as material availability and relative pricing evolve.

-

Accelerate co-development with precision BMG specialists for differentiated components: For high-value segments (aerospace, medical, specialty industrial), partnering with bulk metallic glass suppliers can yield performance advantages and new IP.

-

Operationalize carbon and efficiency claims: Use validated loss-reduction metrics to support regulatory filings, green procurement objectives, and end-customer ROI cases—this will yield faster adoption where energy-efficiency incentives exist.

Report contents: what you’ll find inside

PW Consulting’s full report includes:

-

Quantitative market model (2020–2032) with scenario-sensitive forecasts and sensitivity matrices (presented in USD Million).

-

Segment-level analysis across region, material chemistry, and end-application with growth drivers and constraints (note: detailed subsegment tables are available in the full report only).

-

Supplier benchmarking and capability heatmaps, including plant-capacity audits, quality certifications, and technology roadmaps for key vendors.

-

Commercial playbooks—sourcing negotiation levers, tax and tariff mitigation options, and M&A target lists ranked by strategic fit.

-

Scenario planning templates for tariff, raw material shock, and technology substitution events, with recommended actions tied to board-level decision calendars for 2026.

Concluding counsel

For executives and investors, the strategic question in 2026 is not whether the amorphous metal sheets market will grow—the macro trajectory is clear—but how to position to capture disproportionate margin and strategic advantage as the market matures. Suppliers with scale, validated low-loss technologies, and flexible manufacturing footprints will win volume; buyers who rigorously model tariff exposure, diversify supplier risk, and embed material choice into product architecture will preserve margin and competitiveness.

PW Consulting’s Amorphous Metal Sheets Market report provides the quantitative models, supplier intelligence, and scenario tools necessary to make those decisions with confidence. For access to the full dataset—complete segment-level splits, supplier scorecards, and downloadable scenario workbooks—please visit our report page or contact our industry desk to arrange a briefing and bespoke modeling workshop.

For detailed analysis of this topic, please visit the official page: Amorphous Metal Sheets Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.