PW Consulting: Bio-Based Superabsorbent Polymers (SAP) for Hygiene Products to Expand at 13.98% CAGR, Reaching USD 1.07 Billion by 2032

Bio-Based Superabsorbent Polymers for Hygiene Products: Strategic Imperatives for 2026

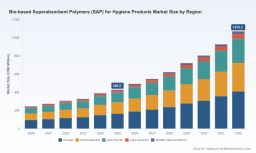

As sustainability commitments harden across consumer goods and retail, bio-based superabsorbent polymers (bio-SAP) have moved from niche R&D projects to commercial inflection. PW Consulting’s new market study—built on a 2020–2025 historical baseline and projecting through 2026–2032—shows a rapidly expanding opportunity: the global bio-based SAP market grew to an estimated USD 428.5 Million in our 2025 base year and is forecast to exceed USD 1 billion by the end of the 2032 horizon, tracking at a compound annual growth rate of approximately 14% through 2032. For leaders making strategic decisions in 2026, this trajectory changes fundamental priorities across procurement, manufacturing, product development, and M&A.

Bio-Based Superabsorbent Polymers (SAP) for Hygiene Products Market

Why this report matters for 2026 decision-makers

-

Timing: The market is leaving the experimental phase. Multiple technologies have reached manufacturing-compatibility milestones, and several large hygiene brands have begun product integrations and pilots. That makes 2026 a pivotal year to move from testing to scale or risk losing preferred supplier status.

Bio-Based Superabsorbent Polymers (SAP) for Hygiene Products Market -

Value chain implications: Transitioning to bio-SAP is not a simple supplier swap. It requires re-evaluating feedstock sourcing, cost-to-serve assumptions, certification pathways, and conversion-line readiness. Our study translates those implications into a prioritized decision agenda for 2026.

Bio-Based Superabsorbent Polymers (SAP) for Hygiene Products Market -

Risk-reward calibration: While bio-based alternatives address regulatory and consumer pressures, they carry distinct cost and supply dynamics versus acrylic-based incumbents. The report quantifies these trade-offs and models plausible volatility scenarios to inform pricing and contracting strategies.

Practical contents you can act on

-

Market sizing and high-level growth scenarios—covering 2020–2025 history and 2026–2032 forecasts—showing where demand and strategic value concentrate at the aggregate market level.

-

Technology readiness and manufacturability assessments for the core bio-SAP chemistries, including starch- and cellulose-derived systems, bio-acrylic routes, and bio-inspired chemistries such as polyaspartic approaches.

-

Supply-chain and cost model frameworks that let procurement teams stress-test supplier proposals under different feedstock and logistics shocks.

-

Regulatory and certification pathways (including mass-balance and traceable biomass certifications) mapped against market adoption scenarios and consumer claims that hold up to audit.

-

Commercial playbooks: partner-selection criteria, pilot-to-scale checklists, manufacturing retrofit vs. greenfield decision trees, and sample contract language to allocate performance and supply risk.

-

Strategic M&A and partnership screeners for buyers looking to accelerate capability via asset acquisition or equity partnerships, and an innovation sourcing matrix for R&D teams.

Note: The report provides granular region- and application-level datasets and proprietary supplier scorecards behind the paywall. We intentionally withhold those split-level figures here to protect competitive value—access to the full dataset and interactive models is available on the report landing page.

Competitive landscape — who’s shaping commercialization in 2026

-

ZymoChem (San Leandro, CA): A notable mover with a scalable 100% bio-based, biodegradable SAP validated on industrial diaper manufacturing lines. Their product positioning emphasizes direct drop-in replacement with industrial performance validation—an important credential for OEMs and converters.

-

NAGASE (Tokyo) / Nagase ChemteX / Nagase Viita: Advancing high-biomass content bio-based SAP technologies with production techniques moving toward commercial launches. Their approach targets sanitary products with an emphasis on mass-producible formulations.

-

Planet Smart Products (London): Marketed as a 100% bio-based, biodegradable and microplastics-free SAP that is compatible with existing manufacturing lines—positioned for brands seeking immediate claims-based differentiation.

-

Lygos (USA): Focused on bio-inspired chemistries such as polyaspartic acid approaches that aim to balance absorbency with a lower environmental impact compared to traditional polyacrylic SAPs.

-

AquaSol Corporation (USA): Commercial starch-based SAPs targeted at personal care categories, emphasizing sustainable high-performance absorption.

-

Established chemical incumbents (BASF, Nippon Shokubai, ADM and others): Bringing scale, certification pathways, and biomass-balanced product lines—these suppliers are moving to hybrid strategies that combine renewable feedstocks with conventional supply chains to limit commercial risk.

-

Other innovators (A&B Smart Materials and regional specialists): Targeting both hygiene and non-hygiene applications where biodegradability or circularity claims add tangible value.

Recent industry movements validate that the market is transitioning from lab to line: leading innovators have announced product launches and industrial-scale validations, and hygiene brands have reported pilot integrations that reduce product-level carbon footprints while maintaining performance metrics. These developments sharpen both the commercial and operational imperatives for OEMs and suppliers in 2026.

Market dynamics that will determine winners

-

Cost and feedstock volatility: Bio-based SAP production still carries a measurable cost premium versus conventional acrylic-based materials at current supply conditions. Volatility in agricultural feedstocks and intermediary feedstock pricing can cascade into supplier pricing and margin pressure for converters and brands. Effective 2026 strategies must therefore incorporate hedging, multi-sourcing, and value sharing.

-

Manufacturing compatibility: A subset of bio-SAP chemistries now demonstrate compatibility with standard hygiene production lines, but not all formulations are equal in handling characteristics or in how they interact with core design and acquisition layer systems. Conversion-line trials and acceptance protocols are essential gatekeepers to broader adoption.

-

Certification and claims management: Traceability and certification (e.g., ISCC-style mass-balance approaches) are emerging as de facto requirements for brands that want to make sustainability claims. Certification timelines and audit burdens should be factored into commercialization schedules.

-

Competitive concentration and supplier strategy: While new entrants bring innovation, established chemical players retain scale and downstream relationships. The market exhibits mid-range concentration dynamics that make selective partnerships and joint development agreements particularly effective for rapid scale-up.

Actionable recommendations for 2026

-

Prioritize pilot-to-scale pathways now. Where product trials are successful, plan staged scale commitments with contingent purchase terms linked to demonstrated line yield and performance.

-

Run blended-sourcing strategies. Combine incumbent suppliers with strategically chosen bio-SAP partners to reduce single-source risk while gaining learning at scale.

-

Embed certification planning in procurement. Treat certification timelines as a procurement deliverable; delay in certification can impose commercial penalties downstream.

-

Stress-test cost models under volatility scenarios. Build P&L sensitivity models that stress agricultural feedstock prices and logistics shocks to understand when bio-SAP becomes dilutive vs. value-accretive.

-

Invest in manufacturing readiness. Minor line retrofits and operator training often unlock disproportionate value; prioritize engineering assessments that quantify retrofit vs. new-capex outcomes.

-

Design product claims defensibly. Align marketing claims with the most rigorous certification available and audit evidence from production pilots to avoid reputational risk.

-

Use M&A and JVs strategically. For companies seeking speed-to-market, minority investments, off-take agreements, or capacity JV structures can de-risk scale commitments while securing advantaged access.

-

Develop consumer-facing narratives tied to measurable benefits. Sustainability alone is insufficient—link biodegradability, reduced microplastics risk, or verified carbon reductions to value propositions that consumers and retailers will pay for.

How PW Consulting’s report supports your 2026 playbook

-

Decision-ready models: Interactive cost and scenario models that help procurement, finance, and R&D quantify trade-offs and inform contract terms.

-

Supplier scorecards: Comparative technology and commercial readiness assessments with recommended engagement strategies for each supplier archetype.

-

Implementation tools: Pilot acceptance protocols, retrofit checklists, and contract language templates tailored to bio-SAP adoption.

-

Executive briefings: Board- and C-suite-ready summaries that distill the strategic value, costs, and timing implications for different adoption pathways.

2026 is a year for decisive action: the market is large enough to matter, growing at a high-teens pace, and populated with credible technology paths and commercial entrants. PW Consulting’s Bio-Based SAP for Hygiene Products study converts that complexity into a structured path from pilot to procurement, enabling organizations to capture first-mover advantages while managing scaling risks. For access to the full datasets, regional and application-level splits, and downloadable decision-support models, visit the PW Consulting report page.

For detailed analysis of this topic, please visit the official page: Bio-Based Superabsorbent Polymers (SAP) for Hygiene Products Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.