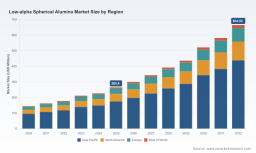

PW Consulting: Low‑Alpha Spherical Alumina Market to Surge from USD 265.4 Million in 2025 to USD 664.9 Million by 2032 (14.02% CAGR) as Asia‑Pacific Leads with USD 174.8M and Top 3 Hold 82.45%

Low Alpha Spherical Alumina Market: Strategic Imperatives for 2026 — PW Consulting Insight Brief

As demand for advanced semiconductor packaging and high-performance thermal management materials intensifies, low alpha spherical alumina has emerged from niche specialty material status to a strategic supply-chain lever for semiconductor OEMs, materials formulators, and capital allocators. PW Consulting’s latest market research — the Low Alpha Spherical Alumina Market Report (base year 2025, forecast 2026–2032) — synthesizes seven years of historical data and a seven-year forecast horizon to deliver actionable guidance for strategic decision-making in 2026. The market is on a sustained trajectory, with a compound annual growth rate (CAGR) of 14.02% through the forecast window; the industry-wide revenue scale expands materially between the 2025 baseline and 2032, underscoring both near-term opportunity and medium-term restructuring risks for suppliers and buyers alike.

Low Alpha Spherical Alumina Market

Market Snapshot: Momentum and Macro Tailwinds

From 2020 through 2025 the market accelerated, driven by surging demand for low-alpha fillers in advanced semiconductor packaging, thermal interface materials (TIM), and other high-reliability electronic applications. Our model shows a clear inflection at the 2024–2025 boundary as next-generation memory and high-speed communication substrate programs moved from development to qualification and early production phases. Looking ahead, the forecast to 2032 incorporates conservative scenarios for adoption curves in HBM-class memory, EV power modules, and high-frequency PCB designs — resulting in a robust projected expansion of total market value over the 2026–2032 window at the stated 14.02% CAGR.

Low Alpha Spherical Alumina Market

- Market dynamics are being driven by three converging forces: accelerated qualification cycles from semiconductor OEMs, material substitution in thermal management systems, and rising importance of alpha-particle control to limit soft-error rates in advanced nodes.

- Concentration metrics show a highly consolidated supply base; the top three producers account for a dominant portion of the market, with the top five players further reinforcing supply-side concentration. This creates both supply vulnerability and strategic pricing power for incumbents.

- Raw-material and trade dynamics are materially influencing near-term cost structures. Recent moves in aluminum-hydroxide pricing and legacy metal-tariff regimes are adding volatility that procurement teams cannot ignore.

Why This Report Matters for 2026 Decision Cycles

For leadership teams preparing budget cycles, capital plans, or M&A roadmaps in 2026, this report bridges technical granularity and commercial strategy with a practical toolkit. We do not simply enumerate suppliers; we provide scenario-based supply-risk modeling, qualification-timeline templates tailored to semiconductor OEM procurement windows, and a commercially actionable supplier-scorecard that maps technical capability, production readiness, geographic diversity, and qualification stage. In markets where qualification lead times can determine multi-year revenue outcomes, understanding the interplay of technical grade, particle morphology, and supply footprint is essential — and that is precisely what our report delivers.

Low Alpha Spherical Alumina Market

- Procurement leaders gain an executable playbook for multi-sourcing and demand hedging tied to qualification milestones rather than ad-hoc spot purchasing.

- Product and packaging teams receive a decision matrix to prioritize material trade-offs between thermal performance, packing density, and alpha-ray counts for different application classes.

- Investors and M&A teams get a focused lens on value-creation levers — capacity scarcity, IP in low-alpha production processes, and customer stickiness created by long qualification cycles.

Competitive Landscape: Capabilities and Strategic Postures

The low alpha spherical alumina ecosystem combines specialty chemical incumbents, high-purity materials innovators, and rapid-scaling regional producers. Our competitive analysis profiles the technical differentiators and commercial strategies of leading players, emphasizing where partnerships, capacity investment, or technology licensing could be decisive.

- Admatechs Co., Ltd. (Japan) — Recognized for high-purity synthesis routes and vaporized metal combustion (VMC) technology, Admatechs targets ultra-low alpha solutions aimed at advanced HBM memory programs. Their R&D intensification into HBM3/HBM4-grade ranges signals intent to protect share at the high end of the value chain.

- Denka Co., Ltd. (Japan) — A strategic incumbent with commercial-scale production for low alpha spherical alumina positioned for thermal-conductive molding compounds. Denka’s public commercial production milestone and stated medium-term sales objectives indicate a go-to-market focus on next-generation memory and communications substrates.

- Resonac Holdings (formerly Showa Denko) — Leveraging fusion-separation expertise to supply high-purity bead forms used across thermal fillers and abrasive segments; their historical role as a low-alpha base-material provider gives them an upstream advantage for integrated supply solutions.

- Imerys (USA) — A materials-engineering player emphasizing optimized particle size distribution for high thermal conductivity and packing density, with product applications spanning electronics thermal management to mobility and EV battery systems.

- Regional and emerging suppliers (China, Europe) — A group of rapidly scaling manufacturers are securing qualification wins and building production footprints to serve local advanced-packaging demands. Their volumes and commercial agility will be a critical source of competitive tension in the coming 18–36 months.

While the market is concentrated, several strategic vectors can shift competitive balance: control of ultra-low U/Th processing pathways, closed-loop quality assurance protocols for alpha counting, and the ability to demonstrate consistent batch-to-batch performance under production-scale rheological and thermal-stress conditions.

Supply-Chain and Raw-Material Considerations

Supply-side economics remain sensitive to aluminum-hydroxide feedstock pricing and regional alumina logistics. Recent commodity movements — including material-price softening in Northeast Asia and regional import patterns in the U.S. — have lowered near-term input costs for preparative chemistries, but the sector remains exposed to geopolitical and trade-policy noise (notably tariff regimes that influence regional premiums). Energy costs at precipitation facilities and bauxite supply volatility continue to create localized price dispersion that downstream formulators must model into total cost-of-ownership analyses.

- Operational teams should run sensitivity analyses that link feedstock price scenarios to gross margins at typical filler loadings; small shifts in input cost can materially change supplier economics given the technical processing required to achieve low-alpha specifications.

- Manufacturers and OEMs should evaluate qualification timelines against potential supply disruptions; dual-sourcing strategies and staged localization are practical mitigations that appear in our recommended playbooks.

What’s Inside the Report (Practical & Operational Deliverables)

PW Consulting’s report goes beyond static market charts to provide operationally relevant deliverables that procurement, R&D, and corporate strategy teams can act upon immediately. Key inclusions are:

- Scenario-based demand forecasting and cash-flow impact models for adoption waves in advanced packaging and TIM markets.

- Supplier scorecards and qualification-roadmap templates that map technical milestones to commercial ramp timelines.

- Cost-sensitivity and feedstock-exposure heat maps, linking aluminum-hydroxide and alumina price variants to margin outcomes.

- M&A and partnership heatmaps identifying acquisition targets, technology licensing opportunities, and potential JV structures to secure supply in priority regions.

- Regulatory and trade-impact assessment focused on tariff and import dynamics, including contingency measures for rapid sourcing shifts.

We intentionally withhold granular supplier share tables and specific application-level splits in this summary to guide readers to the full report, where complete data tables, supplier financial overlays, and granular segmentation analyses are available for subscribers.

Strategic Recommendations for 2026

Based on our analysis, organizations should prioritize three strategic moves in 2026:

- Institutionalize qualification cadence into procurement strategies: Move from opportunistic purchases to milestone-based sourcing contracts tied to sample yield and long-term reliability data.

- Invest selectively in upstream integration or long-term supply agreements: Given market concentration and the technical threshold for ultra-low-alpha production, securing feedstock and processing capacity offers asymmetric risk mitigation.

- Align product roadmaps with material capabilities: Packaging and thermal-management teams should co-develop material requirements with suppliers early in the design cycle to reduce time-to-market and avoid costly re-qualifications.

Final Word — The Strategic Trade-Off

Low alpha spherical alumina sits at the intersection of materials science and supply-chain strategy. The technical performance premium for ultra-low alpha grades commands longer qualification cycles and supply scarcity, while more commoditized grades compete on cost and capacity. For 2026 planning rounds, executives must weigh the strategic value of specification-driven differentiation against the operational complexities of securing consistent, qualified supply. PW Consulting’s Low Alpha Spherical Alumina Market Report provides the empirical backbone and tactical playbooks to inform those trade-offs — and to convert material science into measurable commercial advantage.

For complete data tables, supplier share breakdowns, application-level segmentation, and downloadable procurement templates, access the full report on our website or contact PW Consulting’s industry desk for a tailored briefing.

For detailed analysis of this topic, please visit the official page: Low Alpha Spherical Alumina Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.