PW Consulting: Palm Kernel Shell Market to Expand at a 6.0% CAGR Through 2032 as Asia‑Pacific Drives Demand

Palm Kernel Shell (PKS) Market 2026: Strategic Imperatives from PW Consulting’s New Industry Brief

As global decarbonisation efforts and thermal fuel diversification progress into 2026, Palm Kernel Shells (PKS) have moved from an obscure milling residue to a strategic biomass commodity. PW Consulting’s latest market brief — underpinned by an expanded empirical dataset covering 2020–2025 and a forecast through 2032 — synthesises the near-term operating realities and pragmatic decision levers that corporate energy buyers, traders, and upstream producers must factor into their 2026 plans.

Palm Kernel Shell (PKS) Market

Headline market context

The global PKS market was valued at approximately USD 1,250 Million in 2025 and is projected to grow to roughly USD 1,879.5 Million by 2032. Our modelling anticipates a compound annual growth rate (CAGR) of about 6.0% across the 2026–2032 forecast window. The market’s recovery and steady expansion over 2020–2025 (from about USD 950.5 Million to USD 1,250 Million) reflects both an increase in structured demand (co-firing and dedicated biomass power) and growing industrial adoption where fuel-switching supports emissions objectives.

Palm Kernel Shell (PKS) Market

Why this matters for 2026 decision-making

- Procurement & contracting: Price volatility and supply-side policy interventions are already reshaping contracting horizons. Buyers should treat 2026 as a transitional year to shift from spot-centric sourcing to blended contracts that balance flexibility with supply security.

- Certification & eligibility: Market access into premium markets — notably Japan and certain European feed-in tariff corridors — increasingly depends on verifiable third-party sustainability credentials. Compliance planning for 2026 procurement cycles must include time and capital for certification alignment.

- Supply-chain resilience: Logistics, stocking, and moisture/protection practices materially affect delivered calorific performance and operational uptime for end users; near-port processing and covered storage are operational differentiators.

- Strategic M&A and partnership timing: Mid-market consolidation and expansion by processing-focused players create discrete windows for bolt-on acquisitions and long-term offtake alliances.

Drivers shaping 2026 supply and demand

Three intertwined dynamics will frame commercial choices this year:

Palm Kernel Shell (PKS) Market

- Policy and incentive design: Export levies and import eligibility rules are no longer peripheral. For example, Indonesia’s export tax and levy package — implemented as part of broader commodity taxation measures — materially affects landed cost for international buyers and incentivises greater value-addition locally. Likewise, Japan’s METI is tightening third-party environmental certification requirements for biomass used under FIT schemes, which alters which supply lines are commercially viable.

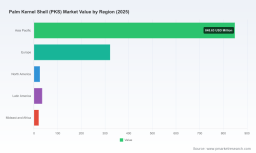

- Resource availability and logistics: PKS remains a byproduct of palm oil milling with concentrated physical supply in Southeast Asia. Industry estimates indicate global PKS availability from Indonesia and Malaysia alone is in the multi-million ton range annually; aligning production seasonality, port throughput, and processing capacity is essential to avoid mid-year shortages or inventory gluts.

- Commercial maturation: The PKS value chain is professionalising. Processors and aggregators are investing in drying, screening, pelletising, and covered stockyards to deliver repeatable fuel quality. End users increasingly price-in quality characteristics (moisture, foreign material, calorific value) rather than accepting commodity-grade variance.

Competitive landscape — strategic positioning of core players

The market displays moderate concentration: the top three suppliers account for roughly 42.5% of the market (CR3), and the top five near 58.2% (CR5). That structure supports both scale advantages and opportunities for niche differentiation. Our brief organises supplier strategies into four archetypes and highlights representative companies.

- Traders and integrated buyers with Japanese market focus: Iwatani Corporation exemplifies an off-taker/trader that sources across Indonesia and Malaysia, emphasises certified supply chains (e.g., GGL), and invests in in-house quality analytics to meet stringent buyer specifications. Such players act as demand-side stabilisers in premium markets.

- Processing and value-add specialists: Bio Eneco and NISSIN BIO ENERGY typify firms investing in processing capacity — drying, screening, pelletisation, and covered stockyards — to reduce moisture and contaminants and serve export markets with predictable fuel characteristics. Bio Eneco’s recent capacity expansion programs indicate a push to capture long-term industrial and power-plant contracts.

- Scalable European and global suppliers: CM Biomass Partners operates as a high-density biomass supplier, positioning PKS alongside other solid biofuels and emphasising handling, uniformity, and sustainability credentials to industrial and utility buyers in diverse geographies.

- Integrated palm producers capturing byproduct value: Major plantation and milling groups (examples include Golden Agri-Resources, Musim Mas, Bumitama, Wilmar, IOI, Sime Darby, KLK, First Resources, and Asian Agri) are exploiting PKS as an internal energy source and as a commoditised product for export. These groups benefit from feedstock control, vertical logistics, and sustainability reporting to support buyer due diligence.

Strategically, buyers should understand whether potential suppliers are primarily processors, integrated producers, or traders: each profile implies different credit, quality, and supply risk. For example, processors can offer tighter quality specs and shorter lead times near ports; integrated producers provide large volume security but may prioritise captive use over long-term commercial exports during tight seasons.

Recent developments and market signals (selected)

- March 2026 — APCASI leveraged International Biomass Expo 2026 in Tokyo to reinforce Indonesia–Japan PKS trade ties and highlighted the scale of Japan-directed flows; industry forums emphasised market stability and export promotion efforts.

- February 2026 — Bio Eneco commissioned a substantial new biomass processing plant in Peninsula Malaysia, signalling capital commitment to export-grade PKS production and a focus on Japan-bound logistics corridors.

- January 2026 — Bio Eneco formalised a supply MoU targeting power-plant procurement and broadened its presence at regional environmental technology shows, indicating both commercial pipeline growth and regulatory positioning.

- Late 2025 — Leading integrated producers published sustainability accounts detailing PKS recovery and utilization as part of circular energy strategies, underscoring reputational and compliance motivations behind supply-side behaviour.

Practical, actionable deliverables in PW Consulting’s report

Our market brief is designed as a decision-ready toolkit for 2026. Key operational modules include:

- Market sizing and medium-term forecasts, with scenario analysis (base, downside, and accelerated adoption) calibrated to policy, price, and logistics assumptions.

- Supply-chain heatmaps and seasonality charts that identify choke points in processing, port capacity, and stockyard availability.

- A certification and compliance playbook that aligns supplier credence schemes (GGL, ISCC, SBP, RSB and equivalents) with buyer eligibility criteria in target markets.

- Procurement templates and contracting structures — including blended tenor recommendations, inventory hedging strategies, and quality dispute clauses — that translate market insight into executable RFP language.

- Counterparty risk matrices and credit frameworks tailored to processors, integrated producers, and aggregators, with recommended credit enhancement and inventory-management clauses.

- Investment and M&A scorecards identifying value-creation levers in processing assets, logistics hubs, and cross-border trade platforms.

Importantly, the brief purposefully refrains from publishing raw segment-level tables in this release. Readers seeking the granular regional, type, and application splits that drive procurement and investment modelling should consult the full report and dataset available through the official source — these pages contain the proprietary segmentation and pricing matrices used in our scenario work.

Risk considerations and near-term scenarios

Key risks that will test strategies in 2026 include:

- Policy shocks: Changes in export taxation or sudden tightening of import eligibility can create transitory price spikes and force contractual renegotiations.

- Certification lag: Suppliers and aggregators that fail to achieve recognised third-party credentials in time may be excluded from FIT-driven demand pools, eroding their revenue mix.

- Logistics and weather: Moisture-related quality degradation during transit and inadequate port handling can impose operational penalties on buyers and reduce delivered calorific value.

Successful 2026 strategies will combine diversified supplier portfolios, active certification roadmaps, and investment in near-port value-addition to preserve margins while meeting environmental compliance thresholds.

How PW Consulting recommends organisations act in 2026

- Audit your eligibility exposure: Map which of your off-takers or subsidy regimes require specific sustainability credentials and quantify the cost/timing to reach those standards across your supplier set.

- Rebalance procurement tenors: Transition to a mix of medium-term contracts with indexed clauses and a controlled spot allocation for opportunistic purchases.

- Prioritise supply partners with covered storage and processing capabilities to minimise moisture and fines exposure — these operational features increasingly command price premia.

- Engage early on certification partnerships: For buyers targeting FIT or premium green markets, co-invest in supplier certification journeys where commercially sensible to secure preferential access.

- Use the CR3/CR5 concentration lens: Evaluate whether your exposure to top suppliers aligns with your risk appetite; consider diversifying suppliers or entering strategic partnerships to reduce single-counterparty concentration risk.

Next steps

PW Consulting’s PKS market brief offers a synthesis of traction points and execution-ready recommendations for 2026. For full segmentation tables, supplier-by-supplier profiles, proprietary price sensitivity models, and downloadable procurement templates, please consult the complete report on our website. The public executive brief is designed to demonstrate analytical depth and strategic direction; the full dataset provides the granular inputs required to operationalise procurement, compliance, and investment decisions in 2026.

PW Consulting remains available for bespoke workshops and rapid due-diligence engagements to translate the brief’s insights into tailored action plans for energy buyers, processors, and investors moving decisively into the PKS market this year.

For detailed analysis of this topic, please visit the official page: Palm Kernel Shell (PKS) Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.