PW Consulting: Electronic Plastic Enclosure Market valued at USD 6,248.5 Million in 2025, set to reach USD 9,395.4 Million by 2032 at a 6.0% CAGR — Asia Pacific, ABS and Consumer Electronics Lead; Top 3 Hold 28.45%

Electronic Plastic Enclosure Market 2026: Strategic Imperatives for Decision-Makers

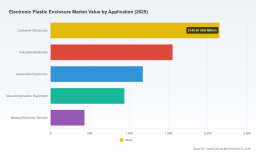

PW Consulting’s latest market research on the Electronic Plastic Enclosure market (base year 2025, forecast period 2026–2032) delivers a pragmatic, strategy-first perspective tailored to executives making allocation, sourcing, product, and M&A decisions in 2026. The report synthesizes historical performance (2020–2025), forward-looking scenarios, and actionable playbooks — grounded in a market that the study measures at USD 6,248.5 Million in 2025 and projects to grow at a compound annual growth rate (CAGR) of 6.0% through the forecast window, reaching approximately USD 9.4 Billion by 2032.

Electronic Plastic Enclosure Market

Why this report matters in 2026

-

Capital allocation clarity: With prolonged supply-chain volatility and raw material price gyrations, finance and corporate development teams require validated topline trajectories and scenario-sensitized margin impacts to prioritize capex, tooling, or acquisition targets. Our report translates macro momentum into investment-ready decision paths.

Electronic Plastic Enclosure Market -

Procurement and sourcing optimization: Procurement leaders face a complex mix of domestic reshoring incentives, tariff pressures, and polymaterial pricing swings. The report provides sourcing playbooks and hedging approaches to protect BOM margins without compromising compliance or cycle time.

Electronic Plastic Enclosure Market -

Product and portfolio strategy: Product teams need to make trade-offs between standard off-the-shelf offerings and higher-margin custom solutions. We map where ergonomics, environmental compliance, and integrated EMI shielding create sustainable differentiation.

High-level market characterization

The market in 2025 sits at USD 6.25 Billion and enters 2026 with steady demand drivers: continued electrification of products, expanded industrial automation, ongoing handset and IoT proliferation, and rising regulatory scrutiny on chemical content and plastic traceability. Our quantitative model, calibrated to observable market flows and supplier reporting, shows a mid-single-digit CAGR through 2032 (6.0%), implying predictable, but not runaway, expansion—creating an environment where strategic moves (e.g., focused product innovation, targeted acquisitions, or supply-chain restructuring) can generate meaningful relative advantage.

Concentration metrics point to a moderately fragmented supplier landscape (CR3 ≈ 28.5%, CR5 ≈ 39.8%), indicating that while recognizable global and regional players exist, there remains ample space for specialty manufacturers and nimble innovators to capture pockets of premium margin and specification-driven demand.

Key industry dynamics shaping 2026 choices

-

Raw materials and cost pressure: Material feedstocks are the proximate driver of short-term margin variability. Recent weeks have shown ABS resin cost upticks tied to upstream turnarounds, while polycarbonate experienced a sharp correction in late 2025 and then price stability. These divergent moves favor manufacturers with flexible bill-of-material strategies and those who can qualify alternate resins quickly.

-

Regulatory and standards tightening: New reporting obligations (for example, national plastics registries) and the expansion of chemical-restriction criteria in global ecolabel frameworks are increasing compliance costs and design complexity. Buyers and OEMs will have to reconcile performance, cost, and end-of-life requirements much earlier in the development cycle.

-

Geopolitical tariff and trade adjustments: Tariff modifications in strategic corridors have demonstrable impacts on landed cost and supply flexibility. The combination of tariffs and logistics costs is raising the value of near-shore manufacturing capacity and forcing strategic segmentation of product families by geography.

-

Customer expectations and product complexity: Demand for enclosures that offer integrated EMI/RFI mitigation, ingress protection, and ergonomic designs has migrated from premium niches to mainstream applications, raising both the bar and the potential for margin capture for providers who can deliver integrated solutions at scale.

Competitive landscape — who matters and why

The competitive map combines global, regional, and specialty providers, each occupying distinct go-to-market and technology positions. Leading players include manufacturers with strong catalog portfolios and rapid-turn custom capabilities, European ergonomics-focused designers, and US-based manufacturers emphasizing domestic production and NEMA-rated outdoor solutions.

-

Polycase (Avon, OH) — Strong US-made positioning with a mix of off-the-shelf and customizable enclosures, recently expanding both product depth and outdoor NEMA-rated offerings. Their incremental product launches in late 2025 and early 2026 underscore a playbook focused on meeting fast-moving industrial and outdoor electronics needs while emphasizing domestic supply resilience.

-

Bud Industries (Willoughby, OH) — Broad catalog reach with industrial-grade ABS offerings and a focus on practical features for sheltering electronics in varied commercial settings. New IP67-rated ABS launches demonstrate a deliberate move upmarket into more demanding ingress-protection segments.

-

Hammond Manufacturing (Guelph, ON) — A hybrid player with both plastic and metal alternatives, notable for EMI/RFI shielding options and a diversified product set that serves customers seeking substitution between materials for performance or compliance reasons.

-

OKW Enclosures (Germany, US presence) — Differentiates on industrial design, ergonomics, and tailored solutions for handheld and panel-mounted electronics. Their focus is higher-value users where appearance and human factors are part of the buying decision.

-

Specialists and OEM-focused firms — Companies such as New Age Enclosures, Productive Plastics, and Toolless capture distinct niches: rapid prototyping and low-to-moderate volumes, thermoforming for large-format equipment, and tooling-free approaches that reduce time-to-market for medical and lab devices.

Recent industry moves — product introductions targeting environmental robustness and expanded size ranges — reveal that incumbents are balancing catalog breadth with selective upmarket feature additions rather than pursuing radical consolidation. For 2026, the structural implication is clear: scale matters for cost competitiveness, but targeted feature-led differentiation remains an effective margin play.

Strategic playbook for executives

-

Right-shore your supply base: Re-evaluate the share of near-shore production for critical SKUs, especially where tariffs or lead-time risk materially elevate total landed cost. Prioritize suppliers that can demonstrate material traceability and compliance reporting to meet emerging registry requirements.

-

Material agility and BOM governance: Build options into designs for alternative polymers and validated suppliers. Use materials cost-sensitivity models (included in the full report) to set dynamic price-adjustment clauses and to calculate hedging thresholds for ABS vs. polycarbonate exposure.

-

Product tiering and margin management: Segment your product portfolio into clear tiers: commodity off-the-shelf, configured off-the-shelf, and fully custom, and assign go-to-market and margin targets accordingly. Invest selectively in tooling for segments with predictable volume and payback under multiple market scenarios.

-

Regulatory-first design: Integrate chemical content limits and reporting needs into early-stage design specs to avoid costly rework. Certification and ecolabel compliance can be monetized in regulated procurement channels and premium corporate accounts.

-

M&A and partnership radar: Look for tuck-in targets that add complementary materials expertise (e.g., polycarbonate vs. ABS), unique process capabilities (thermoforming, toolless), or regional fulfillment nodes. Given the market’s moderate concentration, targeted acquisitions can be an efficient route to scale in specific niches.

What PW Consulting’s full report delivers (practical highlights)

The published study is intentionally operational. It includes:

-

A calibrated market model (2020–2032) with sensitivity and scenario outputs for pricing, material supply shocks, and tariff outcomes to test investment cases.

-

Supplier benchmarks that cover manufacturing footprint, lead times, customization capabilities, and compliance posture — designed for procurement shortlists and RFP preparation.

-

Commercial playbooks for product teams, including margin models, recommended pricing levers, and decision matrices for tooling vs. catalog strategies.

-

Regulatory impact assessments and implementation checklists (traceability, reporting, chemical restrictions), enabling legal and quality teams to prioritize remediation paths.

-

Scenario-tested M&A filters—financial and operational criteria to identify targets that deliver faster time-to-value within 12–24 months.

Note: In keeping with our “trailer” principle, this release deliberately presents the strategic insights and high-level numerical backbone while withholding granular segmentation and proprietary supplier valuations. Those data-rich sections are available within the full report and the interactive model to registered clients.

How to use this research in 90 days

-

Week 1–2: Run our topline scenario for your product mix to quantify exposure to ABS and polycarbonate price paths and to set trigger points for contractual renegotiation.

-

Week 3–6: Shortlist alternative suppliers from the supplier benchmarks for pilot qualification; prioritize partners that can demonstrate compliance reporting and rapid sample cycles.

-

Month 2–3: Rework the product roadmap for high-potential segments, sanction tooling investments where the market model shows resilient volume under downside scenarios, and launch one to two design-for-compliance initiatives.

Conclusion — strategic vantage for 2026

2026 presents a window where disciplined strategic moves will outpace flat-footed reactive responses. With moderate market growth and a fragmented competitive landscape, the highest-return actions are seldom about scale alone: they hinge on material agility, regulatory foresight, and tight alignment between procurement and product strategy. PW Consulting’s report equips leaders with the models and tactical playbooks to convert market clarity into concrete margin and growth outcomes.

To access the full dataset, granular segmentation, supplier heatmaps, and exclusive scenario models that underpin these insights, please visit the report page on PW Consulting’s website and download the complete Electronic Plastic Enclosure Market study.

For detailed analysis of this topic, please visit the official page: Electronic Plastic Enclosure Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.