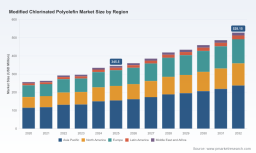

PW Consulting: Modified Chlorinated Polyolefin Market to Hit USD 528.15 Million by 2032 (Base Year 2025) at 6.28% CAGR — Asia‑Pacific Leads with USD 155.32M, Top‑3 Hold 42.5%

PW Consulting Releases Strategic Intelligence Brief: Navigating the Modified Chlorinated Polyolefin Market Ahead of 2026

PW Consulting today publishes an executive intelligence brief derived from our full market research report on the Modified Chlorinated Polyolefin (MCPO) market. Designed specifically for strategic decision-makers who must allocate capital, prioritize R&D, and structure commercial plays in 2026, the brief synthesizes multi-year market dynamics, supplier positions, regulatory pressure points, and practical toolkits that translate insight into action.

Modified Chlorinated Polyolefin Market

Why this report matters for 2026 decision cycles

MCPO sits at the intersection of chemical processing, specialty coatings, and automotive materials engineering. Our market model—anchored to a 2025 base year—shows sustained expansion from a mid‑single-digit market in the early 2020s to a larger, more mature market by the late 2020s. The base market reached USD 345.5 Million in 2025, and our forecast through 2032 projects a compound annual growth rate (CAGR) of 6.28% during the 2026–2032 horizon. That trajectory signals a market that is predictable enough for long‑range investment yet dynamic enough to reward timely portfolio shifts and operational agility.

Modified Chlorinated Polyolefin Market

For corporate leaders planning CAPEX, sourcing strategies, or M&A in 2026, the value of this report is not only in the headline growth numbers but in the operational layers beneath them. Our deliverables translate market growth into actionable scenarios—what capacity investments make sense under different raw‑material price regimes, which formulations reduce regulatory exposure, and how to prioritize channels to capture incremental share.

Modified Chlorinated Polyolefin Market

High‑level market dynamics you need to track

- Upstream volatility shapes margin corridors. Production economics for MCPO are tightly coupled to polyolefin feedstock (PP/PE) and chlorine derivatives. Price swings in crude and downstream petrochemicals propagate through manufacturers’ cost structures, creating windows of margin compression and occasional arbitrage opportunities for integrated players.

- Regulation and sustainability are rewiring demand profiles. Global VOC and chlorine‑use regulations are accelerating adoption of waterborne dispersions and low‑VOC chemistries. Firms that can reformulate or offer validated waterborne alternatives are positioned to protect premium end‑market access—particularly in automotive and architectural coatings—while reducing compliance risk.

- Concentration and competitive positioning. The market displays measurable concentration: the top three players command a meaningful share, and the top five further extend market control. This structure favors quality‑driven competition (formulation, technical service) and makes targeted partnerships or distribution arrangements an efficient route to scale in regional pockets.

Operational takeaways for the 2026 planning season

We translate market insight into a focused set of actions you can adopt in 2026. The full report provides model inputs and scenario outputs; here is an executive summary of the operational imperatives:

- Hedge and secure feedstock exposure. Manufacturers should develop a two‑pronged strategy: near‑term hedging (derivative and contract term strategies) combined with longer‑term vertical integration or strategic supply agreements for polypropylene/PE and chlorine derivatives.

- Accelerate waterborne and low‑VOC product development. Regulatory momentum is a predictable driver across major markets. Prioritize R&D that reduces VOC and eliminates regulated additives, paired with application‑specific validation (automotive primers, printing inks, adhesives) to shorten qualification cycles with OEMs and formulators.

- Deploy a segmentation‑based commercial playbook. Not all end‑markets grow at the same rate or require identical technical support. Use a value‑based selling approach—identify high margin application pockets, anchor with technical trials, and scale via distribution partnerships in adjacent geographies.

- Price management and service differentiation. When raw material pressures compress margins, firms that can rapidly adjust product blends, packaging, and technical service offerings will retain share—especially where coating formulators require fast qualification and supply certainty.

- Strategic M&A and alliances. Given the concentration profile, bolt‑on acquisitions that add waterborne capabilities, regional distribution networks, or specialty application expertise are effective ways to jumpstart growth while minimizing greenfield risk.

Competitive landscape: how leading players are shaping the market

Our competitive analysis profiles companies that set technical and commercial benchmarks in MCPO. Understanding their strategic postures helps in forming targeted counter‑moves or partnership proposals.

- Eastman Chemical Company (Kingsport, TN) — Eastman’s portfolio spans solvent and water‑reducible CPO grades, positioning it as a full‑spectrum supplier for adhesion promoters used in coatings, inks, and adhesives. Its emphasis on waterborne dispersions and low‑VOC formulations aligns with regulatory shifts, making it a key innovator and a natural partner for formulators seeking compliance and performance.

- Nippon Paper Industries (Tokyo) — Through its SUPERCHLON® range, Nippon Paper addresses adhesion on polyolefin substrates with acid‑modified chemistries. The company’s heritage in specialty resins and longstanding presence in automotive primer channels gives it credibility in technical qualification processes—an advantage for customers who need proven track records.

- NAGASE America (distribution of Hardlen CPO) — As a distributor with access to multiple production sources, NAGASE provides flexible supply formats (pellet, solvent, water‑based) and can accelerate regional penetration for manufacturers without local production. Its role underscores the commercial importance of distribution networks in shortening time‑to‑market for new grades.

- PhibroChem (partnering with Nippon Paper) — PhibroChem’s long‑standing distribution partnership demonstrates how alliances can extend the reach of technical brands into target markets while offering local sales and technical service—critical for application‑driven adoption.

- Toyobo (Osaka) — Toyobo’s HARDLEN® series, including MAH‑modified CPOs, highlights the technical differentiation that maleic anhydride modification can provide for adhesion on low‑energy surfaces. Toyobo’s strength is in niche technical leadership and innovation pathways that serve demanding adhesive and coating claims.

- iSuoChem (Guangzhou) — As a regional manufacturer supplying solvent‑soluble and modified grades, iSuoChem exemplifies the competitive pressure from low‑cost, high‑flexibility producers that can quickly customize grades for local ink, coating, and plastic converters.

Across these players, successful strategies converge on three themes: deep technical validation, diversified supply formats (solvent and waterborne), and channel partnerships that accelerate specification into production. Your 2026 playbook should assess competitors on these axes rather than simple price alone.

What the full report contains — practical tools and templates

In keeping with PW Consulting’s focus on decision utility, the full report goes beyond narrative to include operational assets you can deploy immediately:

- Scenario‑based financial models that stress test CAPEX and margin outcomes under alternative raw‑material price paths and regulatory timelines.

- Supplier scorecards and procurement negotiation playbooks that translate concentration metrics into sourcing strategies—when to negotiate, when to partner, and when to integrate.

- Technical risk matrices mapping VOC and chlorine regulation exposure by product family, with a migration roadmap to waterborne formulations and low‑concern chemistries.

- Go‑to‑market templates for regionally differentiated rollouts, including channel economics, qualification milestones for OEMs, and sample‑to‑production timelines.

- Commercial sensitivity analyses (price elasticity, pass‑through rates) to inform pricing policy during feedstock price shocks.

- M&A screening criteria and integration checklists focused on capability gaps (e.g., waterborne R&D, regional distribution, application labs).

How to use this intelligence in your 2026 planning calendar

Embed the report’s outputs into the next three planning rituals:

- Budgeting and CAPEX approvals (Q1 2026): Use our scenario models to calibrate investment size and phasing—prioritize flexible, modular capacity where price volatility is highest.

- Product roadmap and R&D prioritization (Q2 2026): Fast‑track waterborne and low‑VOC variants targeted at the highest value applications and validate with co‑development pilots.

- Commercial execution (Q3–Q4 2026): Implement segmented commercial playbooks—leverage distributor partnerships for faster geographic reach while deploying direct technical service in strategic OEM accounts.

Next steps and access to proprietary datasets

This brief intentionally highlights the strategic contours of the MCPO market but stops short of publishing the granular regional and application splits, supplier share tables, and the full set of scenario outputs. Those datasets and our proprietary models are accessible through the full report and interactive dashboards available on our site. For companies preparing concrete 2026 action plans—sourcing, product development, or M&A—we recommend commissioning the detailed dataset package and a one‑day executive workshop with our consulting team to map the report findings to your balance‑sheet and portfolio choices.

PW Consulting’s Modified Chlorinated Polyolefin Market report provides the combination of market visibility, risk calibration, and practical playbooks necessary to convert 2026 uncertainty into strategic advantage. To request the full report, model access, or a tailored briefing, please contact our industry practice team.

For detailed analysis of this topic, please visit the official page: Modified Chlorinated Polyolefin Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.