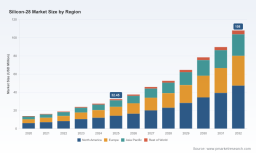

PW Consulting: Silicon 28 Market set to surge from $32.45 Million in 2025 to $108 Million by 2032 at an 18.74% CAGR

Silicon‑28 Market: Strategic Imperatives for 2026 — PW Consulting’s Silicon 28 Market (Silicon‑28) Report Preview

Executive summary

The Silicon‑28 market has transitioned from a specialist research input into a strategic industrial material. PW Consulting’s Silicon 28 Market report (base year 2025; historical coverage 2020–2025; forecast 2026–2032) synthesizes commercial, technological and geopolitical forces that will shape buyer and investor choices in 2026. Our analysis projects a robust expansion path — the market expanding from the 2025 baseline to a materially larger market by 2032 at a compound annual growth rate of 18.74%. This trajectory underpins near‑term procurement, development and policy decisions across quantum computing, advanced semiconductor research and precision metrology.

Silicon 28 Market

Market trajectory: what the headline numbers mean for decision makers

By 2025 the market reached a clearly investable scale, and our modeling indicates continued acceleration through the forecast window. A sustained CAGR near 19% implies that organizations that delay supply‑chain commitments or development programs risk being priced out of critical early production windows, or facing protracted qualification timelines with limited vendor leverage. These macro numbers are the foundation of scenario planning: they quantify the pace at which demand for isotopically engineered silicon will move from pilot projects to recurring production flows.

Silicon 28 Market

Why this report matters for 2026 planning

- Timing: 2026 is a pivot year for many buyers — qualification cycles, supplier selection and pilot runs initiated now will determine 2027 production readiness.

- Supply security: high growth increases the premium on assured access to material; our report maps supplier capacity, contractual terms, and practical mitigation strategies.

- Technology roadmaps: isotopic supply availability directly affects device performance tradeoffs in quantum processors and next‑generation semiconductor metrology; integrating isotopic availability into product roadmaps is now a competitive necessity.

- Regulatory and geopolitical exposure: sourcing pathways and safeguarding obligations will affect lead times and provider selection; our analysis provides a practical lens for compliance and risk management.

What’s inside the PW Consulting Silicon 28 Market report (practical content)

The report is designed as an operator’s toolkit for C‑suite executives, procurement leaders, R&D heads and investors. Highlights include:

Silicon 28 Market

- Demand scenarios and sensitivity analysis that translate headline growth into procurement volumes under conservative, base and aggressive adoption curves for 2026–2032.

- Supply‑chain mapping and vendor scorecards focused on technical readiness, capacity ramp profiles, regulatory transparency and commercial terms.

- Technology readiness and qualification roadmaps for downstream device manufacturers — what to test, when to lock suppliers, and how to sequence pilot → qualification → production.

- Contracting playbooks: template negotiation levers, recommended contract durations, acceptance testing protocols and options for price linkage or volume guarantees.

- Capex and investment case models for vertically integrated strategies (conversion facilities, recovery processes, and localized finishing) that show where on‑balance‑sheet investment reduces long‑term exposure.

- Risk heatmaps covering raw‑material price volatility, inspection/safeguards regimes, export controls and concentration risk with recommended mitigation actions.

Competitive landscape — what industry structure means for buyers and partners

The market is concentrated and supplier positioning matters. A small number of established and emerging providers control the bulk of commercial capability; this concentration has profound implications for pricing power, lead times and qualification complexity. PW Consulting’s analysis evaluates each of the principal commercial players across technology approach, vertical integration, geographic footprint and customer focus.

- ASP Isotopes Inc. — An early commercial entrant using an aerodynamic separation approach. Recent operational milestones and customer contracts mark 2025–2026 as a commercialization inflection. For buyers, ASP’s ramp trajectory creates the first real option to source commercially produced high‑enrichment supplies outside long‑standing national programs.

- Orano Stable Isotopes — Centrifuge‑based enrichment coupled with downstream conversion partnerships. Orano’s value proposition is reliability and integration into established industrial channels, attractive for firms prioritizing traceability and conversion services.

- Rosatom (ECP) — A state backstop with adapted technologies from large‑scale isotope programs. For some customers, Rosatom represents a resilient supply source; yet geopolitical and procurement constraints must be weighed into any sourcing decision.

- Silex Systems — Technology innovation centered on novel separation methods; a potential source of disruptive cost reductions over the medium term and a candidate for strategic partnerships focused on scale and sustainability.

- BuyIsotope (Neonest AB) — Specialist supply for research and metrology markets, including material forms and small‑lot fulfillment; suited to precision applications where bespoke forms or documentation are required.

- URENCO Stable Isotopes — Large‑scale centrifuge capability adapted for silicon, with a supplier profile that emphasizes scale and industrial reliability for customers seeking high‑volume solutions.

- Isoflex USA — Flexible, custom enrichment services aimed at variable enrichment levels and tailored quantities; a practical option for phased qualification programs.

Recent company developments — notably commercial ramp announcements, sample shipments and supply agreements — are reshaping competitive dynamics and shortening timelines for commercial adoption. PW Consulting synthesizes these moves into practical sourcing pathways and contingency plans.

Market dynamics and risk drivers

Several cross‑cutting dynamics determine near‑term commercial outcomes:

- Raw‑material and feedstock context: Inputs and intermediates such as silicon tetrachloride and polysilicon show price and availability volatility that affect unit economics and timing of conversion investments. Buyers should model sensitivity to feedstock price swings as part of procurement decisions.

- Regulatory oversight and safeguards: Some enrichment facilities operate under international safeguards and oversight regimes; compliance obligations and inspection schedules will influence logistics, inventory policies and supplier selection.

- Concentration risk: High market concentration among top providers creates a buyer dependence that necessitates active contingency planning, including dual‑sourcing strategies, stockpiling policies and potential vertical integration.

- Export controls and geopolitics: Access to certain suppliers may be constrained by export controls or geopolitical considerations, affecting lead times and contractual certainty.

Strategic playbook for 2026 (what to do now)

Organizations should treat 2026 as a decisive year for building durable advantage around isotopically engineered silicon. PW Consulting recommends a prioritized set of actions:

- Secure staged supply commitments: Begin with small pilot lots for qualification, linked to conditional ramp options that preserve flexibility while securing initial lead times.

- Qualify in parallel: Run parallel qualification programs with at least two supplier archetypes (large integrated supplier and agile specialist) to reduce single‑point exposure.

- Embed supply risk into product roadmaps: Adjust launch timelines and performance targets to reflect realistic supplier qualification and delivery windows.

- Invest in conversion or finishing partnerships: Where margins or supply security justify it, pursue strategic investments in conversion capacity or long‑term conversion contracts to internalize bottlenecks.

- Engage regulators early: For firms operating across borders, proactive engagement with export control and safeguards authorities shortens approval cycles and reduces transaction risk.

- Use hedging and inventory levers: Incorporate feedstock price hedging, multi‑year contracts and inventory buffers into procurement strategies to manage input volatility.

How corporate leaders and investors should use this report

For boards and strategy teams, the report converts market momentum into executable choices: what to buy, when to invest, which partners to prioritize and how to quantify the tradeoffs between agility and certainty. For procurement and supply‑chain leaders, it provides the negotiation playbooks and supplier scorecards needed to execute deals that preserve optionality. For R&D and product teams, the qualification roadmaps and risk matrices translate supplier timelines into realistic product launch plans. For investors, the report lays out structural winners, potential bottlenecks and capital deployment pathways that will create or erode value over a multi‑year horizon.

Next steps

This preview conveys the strategic framing and practical priority areas that PW Consulting’s full Silicon 28 Market report delivers. To access detailed supply‑side capacity tables, vendor scorecards, full scenario models and the proprietary segmentation that guided our forecasts, please visit the report page. The full dataset and appendices are essential for operational procurement decisions and board‑level approvals in 2026.

For detailed analysis of this topic, please visit the official page: Silicon 28 Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.