PW Consulting: BT Laminate Market to Reach USD 5,243.45 Million by 2032 at a 7.25% CAGR, Asia Pacific Leading with USD 2,246.06M in 2025

BT Laminate Market 2026: Strategic Imperatives for Corporate Decision-Makers

PW Consulting’s latest BT Laminate Market report (base year 2025) frames the industry at a decisive inflection point for corporate strategy. The market reached approximately USD 3,212.45 Million in 2025 and — operating off a 7.25% compound annual growth rate — we project a material expansion through the 2026–2032 forecast window (our model reaches a multi‑billion USD valuation by 2032). For executives, procurement leads, and investors preparing 2026 budgets and strategic roadmaps, the report converts general market momentum into operational actions: where to allocate capex, how to renegotiate supplier contracts, which technical choices to prioritize in product design, and how to stress‑test P&L under persistent cost inflation and supply concentration.

BT Laminate Market

Why 2026 Is Different: Convergence of Demand, Cost, and Concentration

-

Demand dynamics are bifurcating. Macro adoption drivers — cloud/AI acceleration, memory supercycles and ongoing 5G rollouts — are reinforcing long‑term structural growth. Historical market expansion from 2020 through 2025 underscores that trend, and our baseline forecast embeds a continued mid‑single digit CAGR into the next planning cycle.

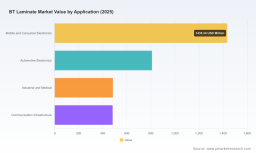

BT Laminate Market -

Input costs and supply shocks are now tangible operational risks. In early 2026 a major BT resin and laminate supplier announced a sweeping price adjustment across core electronic materials — including copper‑clad laminates, prepregs and critical resin sheets — signaling a new phase of cost pass‑through to OEMs and board assemblers. Simultaneously, upstream constraints (notably copper foil, electronic‑grade glass cloth and specialty resins) tightened in late 2025, creating short‑term scarcity that maps directly to lead‑time and inventory exposure.

BT Laminate Market -

Supplier concentration matters. The market exhibits high consolidation: the top three players control the lion’s share of global supply, and the top five players dominate an even larger portion of capacity. This concentration amplifies market power shifts, raises the odds of coordinated price moves, and reduces the margin for error in single‑source supply strategies.

-

Regulatory and product‑engineering forces are additive. Demand for halogen‑free grades and low‑warpage, low‑loss formulations is rising — not just for sustainability reasons, but because performance requirements in advanced packaging and RF applications make these attributes commercially compelling.

What PW Consulting’s Report Delivers — Practical, Transactional, and Board‑Ready

-

Market sizing and scenario engine: a verified baseline (2020–2025 historical series) and an integrated scenario model that runs through 2032. The model is designed to be plugged into corporate financials so CFOs and strategy teams can stress test EBITDA under alternative demand and price trajectories.

-

Supplier risk matrix and concentration analysis: granular profiles of global producers, facility footprints, and a supplier power index that scores availability, price flexibility, and geopolitical exposure. (Note: segment‑level tables and contract‑level assumptions are deliberately gated in the public summary.)

-

Price‑pass‑through and procurement playbook: templates for indexation clauses, staged price adjustment triggers, and supplier co‑investment term sheets. These tools convert the April 2026 price shock into repeatable negotiating playbooks for procurement teams.

-

Product design and material substitution guidance: targeted decision trees for engineers to balance performance (low‑loss, thermal stability, warpage control) against cost and supply risk — including recommended fallback materials and qualification timelines.

-

CapEx and M&A decision framework: a decision matrix that links capacity expansion thresholds to demand milestones, and an M&A scoring model to identify mid‑market consolidation targets that would deliver manufacturing scale or front‑end resin technology.

-

Regulatory roadmap and sustainability checklist: compliance timelines and supplier audit templates to accelerate adoption of halogen‑free and environmentally preferable laminates without sacrificing reliability.

Competitive Landscape — Who Moves the Market and Why It Matters

The BT laminate value chain is anchored by legacy chemical innovators, regional large‑scale laminators, and specialist high‑frequency suppliers. Key players shape technology direction, pricing dynamics and quality benchmarks:

-

Mitsubishi Gas Chemical (MGC) — the originator of BT resin technology — remains a benchmark for low‑warpage, halogen‑free and next‑generation low‑loss grades. Their recent product accolades and an announced price adjustment in 2026 underscore both technological leadership and the market impact when a major supplier moves on cost.

-

Isola Group and Panasonic — global materials and electronics incumbents — each provide a broad portfolio bridging automotive, telecom and consumer applications, and thus act as natural partners for OEMs seeking stable multi‑tier sourcing.

-

Shengyi (SYTECH), Kingboard, Nan Ya, and large regional laminators — deliver scale for high‑volume PCB and packaging needs and are the primary capacity pools in Asia. Their production rhythms often determine lead‑times and regional availability.

-

Rogers, ITEQ, Ventec, Sumitomo Bakelite, Doosan, and Elite Material — focus on specialty RF/microwave, automotive‑grade and high‑reliability laminates; their roadmaps determine how quickly advanced grades (low loss, high Tg, halogen‑free) move from lab to production.

Collectively, these firms’ product roadmaps, capacity plans and pricing strategies are the levers that will shape 2026 outcomes. Our report synthesizes public announcements, patent filings, recent awards, and pricing notices into an actionable supplier playbook for 2026 negotiations.

Strategic Recommendations — Actions to Take in 2026

-

C‑Suite (Strategy & Finance): Re‑calibrate growth corridors using our scenario engine; embed a price‑inflation stress case into budgeting (including the potential for episodic supplier price adjustments) and set clear threshold triggers for capex and M&A deployment.

-

Procurement: Implement multi‑tier contracting with clearly defined indexation clauses tied to upstream commodity baskets (copper foil, glass cloth, resin indices). Negotiate capacity reservation options where strategic and prioritize suppliers with demonstrated low‑warp, halogen‑free capability.

-

Supply Chain & Operations: Revisit safety stock policies (short‑cycle critical sub‑components), diversify glass‑cloth and copper foil sources, and fast‑track dual‑sourcing for critical product families. Use our supplier risk heatmap to prioritize audits and qualification investments on a 90/180 day cadence.

-

Product & Engineering: Prioritize design choices that allow material flexibility (e.g., tolerance envelopes that accept alternative CCL or prepreg sources) and build qualification roadmaps for halogen‑free and low‑loss grades to avoid last‑minute redesigns.

-

M&A & Corporate Development: Target transactions that deliver either vertical integration into specialty resin/cloth supply or horizontal consolidation in regional laminators that can be upgraded to low‑loss, halogen‑free production. Use our M&A scoring rubric to screen targets against price risk mitigation and time‑to‑market criteria.

Scenario Planning Snapshot — Rapid Decision Triggers

-

Base Case (embedded in our forecast): Continuation of current growth trajectory with mid‑single digit CAGR; scarcity episodes are managed via short‑term price pass‑through and tactical inventory adjustments.

-

Upside (accelerated memory/AI demand): Lead‑time extension and selective shortages become chronic; recommend accelerated capex partnerships and prioritized long‑term supply contracts with price escalation floors tied to explicit capacity commitments.

-

Downside (soft consumer electronics demand + trade headwinds): Demand compression pressures pricing and underutilizes recent capacity expansions; recommend temporary inventory normalization, flexible contract terms, and re‑scoped R&D spend toward higher‑margin specialty grades.

How to Use This Report in Your 2026 Decision Cycle

Leaders should integrate the PW Consulting BT Laminate Market report into three distinct governance forums in 2026:

-

Quarterly executive strategy reviews — to update the scenario outlook and capital deployment triggers;

-

Annual procurement RFP cycles — to embed new indexation and capacity reservation language; and

-

Product roadmap sign‑offs — to align materials qualification timelines with commercial launch plans and regulatory compliance milestones.

The report ships with an executive dashboard and the underlying financial model so teams can run bespoke what‑if analyses aligned to corporate KPIs. Note that the public summary here highlights key directional findings; the full report contains the definitive dataset, regional and application breakdowns, supplier‑level price sensitivity models and downloadable templates for immediate use in negotiations and board materials.

Next Steps

If your 2026 planning requires defensible scenarios, procurement playbooks, or a prioritized supplier mitigation plan, PW Consulting’s BT Laminate Market report is tailored to convert industry insight into executable decisions. To access the complete dataset, segmentation tables and interactive model, visit the PW Consulting report page or contact our industry team for a tailored brief and model walk‑through.

For detailed analysis of this topic, please visit the official page: BT Laminate Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.