PW Consulting Forecast: Mold Flux for Continuous Casting Market Hits USD 564.3 Million in 2025, Poised for 3.85% CAGR Through 2032

Mold Flux for Continuous Casting Market — Strategic Outlook for 2026

PW Consulting is pleased to publish an executive synthesis of our new market study on Mold Flux for Continuous Casting. As senior strategic advisors and the firm’s lead industry analysts, our objective in this pre-release is to outline the practical value this study delivers to executives making decisions in 2026 — highlighting the commercial imperatives, competitive levers, and risk mitigants that matter most — while preserving the report’s proprietary detail to drive direct engagement with the full publication.

Mold Flux For Continuous Casting Market

Headline market context

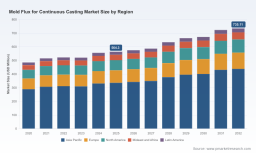

The mold flux for continuous casting market is modest in absolute scale but strategically important to steelmakers worldwide. After a period of gradual expansion between 2020 and 2025, the market reached an estimated USD 564.3 Million in 2025 (base year). Our forecast through 2032 assumes a compound annual growth rate (CAGR) of 3.85% (forecast period 2026–2032), with the market projected to exceed the mid-seven-hundred million USD range by the end of the horizon. These headline metrics reflect a market characterised by steady end-market demand, pockets of technology-driven premiumisation, and evolving regulatory constraints that disproportionately influence product formulation and supply chains.

Mold Flux For Continuous Casting Market

Why 2026 is a pivotal planning year

-

Operational recalibration after investment cycles: Several global suppliers and regional integrators entered the recent cycle with capex and plant expansions intended to shorten lead times and localise supply. 2026 is the year many of those initiatives translate into procurement and sourcing decisions.

Mold Flux For Continuous Casting Market -

Regulatory and formulation inflection: A clear industry shift toward low‑fluorine and fluorine‑free alternatives — and the parallel development of carbon‑free powders tailored for ultra‑low‑carbon steels — is moving from R&D into production. Compliance and equipment longevity concerns are now material contributors to product selection.

-

Supply‑side concentration and strategic positioning: Market concentration metrics indicate a moderately consolidated supply base, creating both opportunities for challengers and incentives for incumbents to pursue M&A, partnerships, or targeted capability expansion to access specialty formulations and regional steel clusters.

What our report delivers to decision-makers

-

Actionable market sizing and scenarios — Our model integrates historical data (2020–2025) with bottom‑up demand drivers to provide a probabilistic forecast (2026–2032). The aim is not just to present a point estimate but to allow decision-makers to stress-test plans against high‑ and low‑demand scenarios.

-

Raw-material sensitivity and procurement playbook — We map formulations to key mineral inputs (e.g., silica derivatives, calcium and boron systems, fluorine alternatives) and quantify how raw‑material volatility and substitution pathways affect cost and performance trade-offs.

-

Regulatory risk matrix — The study identifies jurisdictions where emissions and workplace‑safety limits are likely to accelerate adoption of alternative chemistries, and translates those regulatory trajectories into product roadmap implications for suppliers and steelmakers.

-

Manufacturing footprint and capability assessment — We benchmark spray‑drying capacity, R&D capabilities, and close‑coupled technical service teams to show which supplier profiles are best positioned to support sophisticated continuous casting operations.

-

Competitive playbooks and M&A readiness — Through a practical decision framework, we guide buyers and sellers on when bolt‑on acquisitions, JV structures, or capacity investments make strategic sense versus focusing on co‑development and long‑term supply agreements.

Competitive landscape — how to read the player map

The market is served by a mix of global specialists, national champions, and highly focused regional producers. Our report provides a through‑line on capability, channel strength, and technological differentiation across the vendor population. Key themes include:

-

Technology leaders with integrated service models: A few established suppliers combine broad formulation libraries with deep metallurgical support, enabling them to be preferred partners for large steel groups seeking consistency across multiple casting lines.

-

Strategic consolidators: Recent strategic moves by established refractories and specialty chemical firms demonstrate a push to broaden global platforms and capture value across adjacent steelmaking inputs.

-

Regional specialists delivering speed and customisation: Several local manufacturers remain highly relevant where proximity, spray‑dry infrastructure, and hands‑on process tuning are decisive for mill performance.

-

Small‑batch premium craft producers: There is a niche, but commercially meaningful, market segment for high‑quality, craft‑manufactured powders that serve premium or metallurgically challenging applications.

To convert this qualitative read into commercial action, the full report includes company‑level profiles and a negotiated sourcing map that helps procurement teams prioritise suppliers by capability, risk, and cost to serve.

Recent industry developments shaping 2026 strategy

-

Cross‑border portfolio actions: Strategic acquisitions and partnerships have expanded the global reach and product breadth of several major refractories players, accelerating standardisation of product lines and access to specialist formulations.

-

Targeted capacity expansions in growth markets: Several firms have announced local production increases and new plants to address logistics and tariff frictions — a trend that will influence sourcing choices for regionally focused steel operations.

-

Plant‑level innovation: Suppliers are increasingly investing in process controls and analytics that reduce variability in powder performance — an area that will amplify the value of technical service agreements.

Strategic imperatives for 2026 decision‑makers

-

Harden supply resilience: Build dual‑sourcing strategies for critical formulations and align contracts with suppliers that can demonstrate secure raw‑material channels and local contingency capacity.

-

Prioritise formulation roadmaps: Allocate R&D and procurement budgets toward low‑fluorine and carbon‑free alternatives where certification timelines and equipment compatibility indicate high near‑term adoption.

-

Use co‑development as a competitive moat: Steelmakers that co‑invest in tailored powders and process trials reduce operational risk and extract performance premiums; suppliers that offer rapid field service gain pricing power.

-

Evaluate M&A thoughtfully: For players pursuing growth through acquisitions, focus on targets that add speciality formulations, spray‑dry capacity, or proximity to major steel clusters rather than targets that only modestly increase volume.

-

Embed digital QC and traceability: Invest in quality‑analytics at the point of use to reduce casting variability — a low‑cost lever to capture substantial value through yield and surface‑quality improvements.

-

Integrate ESG into supplier selection: Environmental and personnel‑safety considerations around fluoride handling are increasingly material; choose partners with credible transition plans and transparent monitoring.

How leading stakeholders will use the report

-

Strategy teams: Validate investment timing and geographic priorities against scenario outputs that incorporate regulatory shifts and raw‑material substitution.

-

M&A and corporate development: Use our competitive diagnostics and target shortlists to screen acquisitions and to stress‑test valuations under different integration outcomes.

-

Procurement and supply chain: Translate formulation risk into contract structures, hedging strategies, and vendor performance metrics to reduce operational exposure.

-

R&D and process engineering: Benchmark internal formulation capabilities and identify near‑term co‑development partners to accelerate adoption of compliant, high‑performance powders.

Methodology and confidence drivers

Our analysis synthesises bottom‑up volumetric modeling, primary interviews with plant metallurgists and procurement leads, supplier plant visits, and a proprietary database of historical demand from 2020 through 2025. The forecast for 2026–2032 reflects a base CAGR of 3.85% and incorporates sensitivity cases that stress raw‑material price shocks and accelerated regulatory adoption. Market concentration is quantified in the report to help readers assess competitive dynamics and the implications for pricing and service levels.

Concluding perspective

For executives facing 2026 budget cycles, the mold flux market presents a classic combination of low headline growth but asymmetric supplier and product risks. Small shifts in formulation regulation, raw‑material availability, or supplier footprint can have outsized effects on casting performance and overall steelmaking economics. PW Consulting’s full report frames these inflection points and provides the practical toolset — from procurement checklists to M&A playbooks — that decision‑makers need to convert uncertainty into advantage.

To access the complete dataset, segmented analytics, supplier scorecards, and scenario workbooks that underpin these conclusions, please visit our report page or contact your PW Consulting representative. The full report preserves the commercial detail required to act with confidence in 2026 while offering the bespoke advisory support many clients will require to implement the recommendations.

For detailed analysis of this topic, please visit the official page: Mold Flux For Continuous Casting Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.