PW Consulting: HDI Biuret Market to Rise from USD 540.24 Million in 2025 to USD 804.29 Million by 2032 (2026–2032 Forecast) at a 5.85% CAGR — Asia‑Pacific Leads with USD 232.13M, Top 3 Hold 62.45%

Hdi Biuret Market 2026 Strategic Outlook — PW Consulting Industry Brief

Executive summary

PW Consulting today releases a strategic brief drawn from our forthcoming Hdi Biuret Market report, offering an operationally focused intelligence package tailored for corporate decision-makers preparing for 2026. The market for HDI biuret has shown steady expansion through the early 2020s, rising from roughly USD 410 million in 2020 to an estimated USD 540 million in 2025. Our modelling indicates continued growth at a compound annual growth rate of approximately 5.85% across the 2026–2032 forecast window, with an expected market value approaching the mid‑to‑upper USD 700–800 million range by 2032. This trajectory reflects a confluence of regulatory pressure on VOCs, adoption of high‑solids and waterborne polyurethane systems, and incremental capacity additions by major producers.

Hdi Biuret Market

Why this matters for 2026 decisions

For executive teams making capital-allocation, product-development, procurement, and M&A choices in 2026, HDI biuret represents a mid‑growth specialty chemical with outsized strategic implications for polyurethane coatings portfolios. The market’s steady CAGR masks underlying volatility in raw-material costs, regional supply balances, and technology shifts (notably the push toward bio‑content and low‑viscosity, high‑solids chemistries). Decisions taken next year about plant capacity, upstream integration, supplier partnerships, and formulation investments will materially affect margins and market access through the latter half of the decade.

Hdi Biuret Market

Market dynamics shaping 2026 strategy

- Regulatory acceleration: Global VOC reduction policies and ongoing enforcement of chemical safety frameworks are accelerating uptake of HDI‑biuret‑based high‑solids and waterborne 2K systems. Suppliers and formulators that can demonstrate compliance while maintaining performance will capture disproportionate share gains.

- Product innovation: Demand is bifurcating between classical weather‑stable, non‑yellowing grades for topcoats and engineered low‑viscosity derivatives enabling higher solids and better application properties. New product launches through 2025–2026 show this technology axis is a primary battleground.

- Supply-side shifts: Recent and announced capacity expansions by key producers are changing regional supply dynamics. Where expansions align with downstream infrastructure and logistical efficiencies, they compress margins for higher‑cost imports and reshape sourcing strategies.

- Raw-material volatility and regional pricing spreads: Feedstock and HDI monomer prices have shown meaningful regional variance, contributing to strategic sourcing arbitrage and spurring some manufacturers to pursue integration or long‑term procurement contracts to stabilize costs.

- Market concentration: The HDI biuret industry remains concentrated, with the top three and top five suppliers collectively commanding a significant share of global supply — a structural reality that amplifies the strategic importance of supplier relationships, contractual terms, and supply resilience planning.

Competitive landscape — what corporate strategists need to know

Our competitive analysis synthesizes public disclosures, product portfolios, and recent strategic moves across the leading producers. These firms are shaping the market through new product introductions, capacity investments, and strategic supply agreements. Key imperatives for 2026 include assessing supplier roadmaps for bio‑content and waterborne‑optimized chemistries, evaluating the availability of low‑viscosity and high‑solids grades for targeted applications, and mapping each supplier’s geographic capacity against expected regional demand.

Hdi Biuret Market

- Covestro AG (Leverkusen, Germany): Continues to invest in sustainable hardener chemistries, recently launching a bio‑content line designed for automotive refinish and architectural applications. For OEMs and tier‑one suppliers, Covestro’s product positioning signals a competitive shift toward sustainability‑led procurement criteria.

- BASF SE (Ludwigshafen, Germany): With strategic expansion of HDI‑based polyisocyanate capacity in Europe, BASF is reinforcing its supply options for transportation and industrial coatings customers; procurement teams should re‑evaluate regional sourcing strategies in light of enhanced European throughput.

- Wanhua Chemical Group (Yantai, China): Large‑scale capacity additions in Asia are expanding cost‑competitive supply into global markets; formulators and distributors must model the pricing and logistics impacts of increased Asian output when negotiating supply terms.

- Vencorex Holding SAS (France): Long‑term supply agreements for waterborne 2K clearcoats highlight the strategic value of secured off‑take arrangements. Companies seeking product stability should examine contractual structures similar to these multi‑year agreements.

- Evonik, Asahi Kasei, Tosoh, Mitsui, Huntsman, Kowa: Each of these firms offers differentiated product attributes — from hydrophilicity enhancements for high‑solids waterborne systems to low‑viscosity derivatives for high‑solids maintenance coatings. Their R&D roadmaps and targeted launches will dictate formulation choices for coatings OEMs through 2026 and beyond.

Practical recommendations for executives planning 2026 moves

- Prioritize formulation investments that reduce VOCs while preserving application performance. Target R&D and capex toward low‑viscosity, high‑solids chemistries and waterborne systems that align with regional VOC regulation trajectories.

- Secure diversified supply lines and consider anchoring long‑term off‑take contracts. Given recent capacity additions and the concentrated supplier base, long‑term agreements can provide cost visibility and priority access to constrained grades.

- Hedge feedstock exposure and monitor regional pricing spreads. Differential raw‑material pricing across regions can be exploited via procurement strategies that combine local sourcing, spot hedging, and selective vertical integration.

- Embed regulatory scenarios in product roadmaps. Build compliance buffers into specifications — for example, conservative residual monomer thresholds and pre‑emptive labeling and safety data updates for REACH and other regimes.

- Evaluate strategic M&A and JV options to accelerate market entry or secure technology access. Smaller specialized producers and technology developers can provide rapid access to bio‑content platforms and niche chemistries that would take longer to develop in‑house.

- Operationalize a 90‑ to 180‑day readiness plan for tariff and logistics shocks. Tariff proposals affecting aliphatic isocyanates have been discussed in several markets; scenario planning should include inventory, routing, and contract renegotiation contingencies.

What the PW Consulting Hdi Biuret Market report delivers (practical, actionable content)

Our full report is constructed as an executive toolkit for companies making hard decisions in 2026. Highlights include:

- Detailed market model (historical 2020–2025, base year 2025, forecast 2026–2032) with sensitivity scenarios and clear assumptions—enabling bespoke “what‑if” modelling for capex and commercial planning.

- Supplier matrix and capacity map with head‑to‑head profiling of technology platforms, strategic priorities, and commercial levers.

- Price‑deck and input‑cost analysis tracing HDI monomer and HDA feedstock dynamics, inclusive of regional differentials and margin implications.

- Regulatory and trade‑policy playbook that translates compliance requirements into product specs, labeling and formulation checklists for launch readiness.

- Go‑to‑market modules for formulators and coatings producers, including channel prioritization for automotive refinish, industrial maintenance, and waterborne topcoats.

- Supply‑chain risk heatmap and mitigation scenarios covering capacity shortages, tariff shocks, and logistics disruptions.

- M&A and partnership shortlist with criterion‑based scoring for near‑term bolt‑on targets and technology acquisitions.

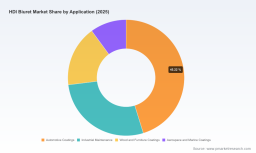

Note: this brief intentionally omits the full segmentation tables, regional and application‑level percentage splits, and transactional level pricing found in the full report to preserve the report’s proprietary value. Those detailed data assets are available only in the complete PW Consulting deliverable.

Methodology and reliability

Our findings reflect a multi‑tiered methodology: bottom‑up market building from product and application shipments, supplemented with primary interviews across supply chain nodes, company disclosures, proprietary pricing datasets, and regulatory source material. The base year is 2025, with a historical window covering 2020–2025 and a forecast spanning 2026–2032. We stress‑tested our base case with upside and downside scenarios to capture sensitivity to raw‑material volatility, regulatory tightening, and accelerated substitution trends.

How to use this intelligence in 2026

Leaders should treat the HDI biuret market as a strategically important specialty input where modest shifts in formulation or supply strategy yield meaningful commercial outcomes. Practical next steps for 2026 include: commissioning a short‑form supplier due diligence focused on sustainability credentials and lead times; running integrated price‑to‑profit models for key coatings product lines; and testing one pilot formulation upgrade to a high‑solids or waterborne system to validate performance and cost impacts.

Closing and next steps

PW Consulting’s Hdi Biuret Market report is positioned as an actionable playbook for companies intending to enter, defend, or expand in this specialty chemicals arena over the next seven years. The market’s steady growth, concentrated supply base, and ongoing product innovation make 2026 a decisive planning year. For access to the full dataset, proprietary segmentation, and the comprehensive suite of strategic tools, visit the PW Consulting report page and request the full Hdi Biuret Market report and accompanying advisory engagement options.

For detailed analysis of this topic, please visit the official page: Hdi Biuret Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.