PW Consulting: Hinge Top Pill Pod Market Poised for 6.15% CAGR, Unlocking New Growth for Manufacturers

Hinge Top Pill Pod Market — Strategic Preview for 2026: Why PW Consulting’s Hinge Top Pill Pod Market Report Is a Must-Read for Executive Decision-Making

PW Consulting’s latest Hinge Top Pill Pod Market report is positioned as an operational playbook for commercial, procurement, regulatory, and M&A leaders preparing for the next phase of growth in solid oral medication packaging. Built from a rigorous 2020–2025 historical base and forward-looking 2026–2032 modeling, the study combines market sizing, scenario-based forecasts, supply-chain diagnostics, and executable commercial strategies. The market reached roughly USD 142.5 million in 2025 and is modeled to grow at a 6.15% compound annual growth rate through the forecast period, underscoring steady expansion and persistent opportunity across manufacturers, healthcare providers, and contract packagers.

Hinge Top Pill Pod Market

Why this report matters for 2026 strategic planning

- Timing for portfolio and procurement moves: The mid-single-digit CAGR and predictable year-on-year market expansion create a window where targeted investments—capacity additions, polymer sourcing agreements, or automation upgrades—can be planned with reasonable downside protection. Executives who wait for more volatility may face higher capital and supply costs.

- Regulatory alignment as a competitive moat: Hinge top pill pods are treated as Class I exempted devices for solid medication dispensers and must comply with FDA container-closure guidance. The report maps how early adoption of robust container-closure compatibility testing and documentation materially de-risks contracts with pharmaceutical customers and reduces time-to-market friction.

- Actionable supply-side playbook: With medical-grade polypropylene and LDPE as dominant feedstocks, the analysis highlights procurement levers—long-term offtake, dual-sourcing, and specification harmonization—that materially improve margin resilience in a world of polymer price cycles and regulatory scrutiny (REACH/RoHS/BPA-free expectations).

Market dynamics at a glance (what you need to know without the raw tables)

The market’s evolution over the last half-decade reflects two interlocking dynamics: incremental demand growth driven by aging populations and outpatient medication adherence programs, plus product innovation focused on user convenience (hinged closures, tamper-evidence and child-resistance overlays). Our model shows a steady increase from the 2020 base through 2025 to a market roughly USD 142.5 million in size, and continues to expand through 2032. That steady expansion favors companies that combine manufacturing efficiency with compliance and nimble commercial execution.

Hinge Top Pill Pod Market

Concentration analysis indicates a market where the top three players control a meaningful but not dominant share of industry revenue, while a slightly broader set of five firms increases that share materially. This structure creates pockets of pricing power and simultaneously leaves room for specialists and regional players to grow via service differentiation, technical customization, and local regulatory relationships.

Hinge Top Pill Pod Market

Competitive landscape — what to watch among incumbent and emerging suppliers

- SKS Bottle & Packaging (Watervliet, NY) — Known for a broad SKU range and strong retail/supplement market channels, SKS’s product breadth and customer-facing packaging innovation positions it well for programs focused on patient adherence. The firm’s emphasis on multiple color and size SKUs supports private-label strategies and quick turn prototyping.

- Thornton Plastics (USA) — Thornton’s polypropylene hinge vials illustrate the value of engineering a balance between material performance and cost. Expect them to compete on capacity for mid-sized runs and on relationships with regional distributors.

- Juvitus (USA) — Specialty sizing and incorporation of functional design elements (fill lines, integrated hinges) make Juvitus a candidate for pharmaceutical and supplement customers that require tighter dosing tolerance and clearer assembly specifications.

- Litesmith (USA) — With a focus on translucent, small-diameter hinge-top containers, Litesmith exemplifies a niche player leveraging form-factor innovation to serve non-traditional medical and consumer markets.

- LA Container (USA) — Child-resistant designs and ASTM-approved Squeezetops® stress the importance of safety certification in tender evaluations; LA Container’s positioning highlights how conformity to recognized standards drives premium contract wins.

- Tiantai Biolife & Gracepack (China) — These manufacturers demonstrate the continuing role of Asia-based suppliers in global sourcing strategies. Their scale and cost base make them important partners for large-volume programs, but buyers must weigh logistics, quality audits, and regulatory documentation when designing multi-source architectures.

For decision-makers, the competitive takeaway is simple: success in the next 18–36 months will be determined not by commodity price alone but by the ability to integrate material specifications, regulatory readiness, and commercial agility into customer-facing value propositions. Our report profiles each major supplier across seven dimensions—capacity, quality systems, product breadth, regulatory certifications, geographic reach, service levels, and price positioning—providing the comparative view executives need to prioritize partners.

Regulatory and materials considerations that change procurement behavior

- FDA container-closure expectations: The report breaks down what “good documentation” looks like for hinge top applications and how early validation of container-closure compatibility can shorten approval timelines and avoid costly redesigns after contract award.

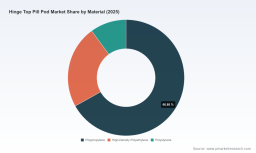

- Material selection and sterilization routes: Polypropylene’s durability and chemical resistance make it the material of choice for most hinge top pods intended for dry, oral solids. The report maps where LDPE and polystyrene remain relevant, and where gamma sterilization or other sterilization modalities are technically appropriate and commercially practical.

- Design limitations: Hinge top containers are not engineered for liquids. For procurement and product teams, the report provides a decision matrix to avoid misapplication risk and related product liability.

What’s inside the report — practical, implementable deliverables

We designed this study to be a toolkit for operators, not an academic compendium. Deliverables include:

- Scenario-based revenue and supply models covering conservative, base, and upside cases across the 2026–2032 horizon (with sensitivity to polymer cost and regulatory delays).

- A supplier due-diligence checklist tailored to hinge top pod manufacturing, including audit protocols, testing requirements, and contractual warranties that purchasers should demand.

- Cost-to-serve and margin-improvement playbooks for manufacturers, with prioritized CAPEX and digitalization levers to improve throughput and lower per-unit costs.

- A commercialization guide for contract packagers and brand owners on SKU rationalization, private-label strategies, and e-commerce fulfillment optimizations for medication adherence solutions.

- An M&A heat map identifying target profiles, likely synergies, and integration risks for acquirers looking to consolidate capabilities in design, regulatory compliance, and regional fulfillment.

Executive recommendations for 2026 action plans

- Buy-side leaders: Implement a two-tiered sourcing strategy—secure long-term agreements with proven, certified suppliers for core SKUs while maintaining flexible secondary suppliers to manage price and capacity shocks.

- Manufacturers: Prioritize investments in quality systems and documentation that align with FDA container-closure expectations; firms that can demonstrate rigorous compatibility testing will command better access to pharmaceutical contracts.

- Private equity and M&A teams: Focus on targets that bring regulatory advantages (certifications, testing labs) and deep channel relationships with pharmacies and medical retailers; integration of these assets can unlock outsized synergies.

- Product teams and brand owners: Reassess SKU proliferation; consolidation of SKUs combined with improved patient-centric features (child-resistance, clear dosing guides) can increase sell-through while reducing logistics complexity.

Methodology and credibility

PW Consulting’s analysis synthesizes bottom-up primary interviews with suppliers and purchasers, bill-of-materials and cost benchmarking, polymer market input, and regulatory mapping. The forecast uses scenario analysis driven by demand signals from outpatient care trends and supplementation markets, and is stress-tested against polymer price volatility and regulatory-adoption lags. For competitive benchmarking, we examined capacity footprints, product portfolios, and certification profiles across established and emerging vendors.

Conclusion — a strategic window for decisive, low-regret moves

As the hinge top pill pod market continues its steady climb, the strategic value of having a playbook cannot be overstated. Whether you are a procurement leader aiming to lock in supply at competitive terms, a manufacturer plotting capacity investments, or an investor evaluating consolidation opportunities, the next 12–24 months will reward those who combine regulatory foresight with disciplined commercial execution.

PW Consulting’s Hinge Top Pill Pod Market report is intentionally designed to be immediately actionable: it surfaces the levers that move margins, shortens decision cycles by clarifying regulatory requirements, and highlights partner-selection criteria that materially reduce execution risk. For the complete dataset, granular segmentation, supplier scorecards, and downloadable models needed to execute on these recommendations, please visit the full report page.

For detailed analysis of this topic, please visit the official page: Hinge Top Pill Pod Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.