PW Consulting: Photoresist Photosensitizer Market Poised for 8.01% CAGR During 2026–2032

Photoresist Photosensitizer Market: Strategic Imperatives for 2026 — A PW Consulting Preview

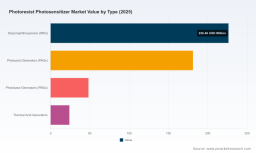

As semiconductor and advanced display manufacturers accelerate node migration and packaging complexity, the upstream chemistry that enables pattern fidelity — photoresist photosensitizers — is becoming a strategic linchpin. PW Consulting’s new market study, grounded in 2020–2025 historical analysis and extending to a 2026–2032 forecast horizon, quantifies that lens and translates it into decision-grade guidance for 2026. The market, which reached roughly USD 480 million in 2025, is projected to expand at a compound annual growth rate (CAGR) of approximately 8.0% through 2032, reaching an estimated USD 823 million by the end of the forecast period. This briefing highlights the report’s strategic value while intentionally withholding the granular segment tables and regional allocations that are available in the full report.

Photoresist Photosensitizer Market

Why this market matters for 2026 decision-makers

Photosensitizers — including photoacid generators (PAGs), photobase generators (PBGs) and allied compounds — are not mere inputs; they materially determine lithographic performance (sensitivity, line-edge roughness, outgassing and resolution) and therefore the viability of new process nodes and packaging paradigms. The combination of accelerating adoption of EUV-tailored chemistries, heightened regulatory scrutiny of legacy chemistries (notably PFAS-related species), and concentrated supply among a handful of advanced-materials manufacturers creates a distinct set of strategic risks and opportunities for equipment OEMs, fabless firms, integrated device manufacturers (IDMs), wafer foundries and materials suppliers.

Photoresist Photosensitizer Market

Core strategic imperatives for 2026

-

Supply-Chain Resilience and Sourcing: The market’s growth trajectory amplifies exposure to single-source or single-country risk. Firms should prioritize supplier-mapping, dual-sourcing of critical PAG chemistries, and long-lead inventory strategies for EUV-grade photosensitizers where qualification cycles are lengthy.

Photoresist Photosensitizer Market -

Technology Roadmapping: R&D and product roadmaps must explicitly account for chemistry-performance trade-offs across ArF, ArF-immersion and EUV regimes. Early engagement with materials suppliers to co-develop low-outgassing, low-impurity PAG systems reduces qualification time at advanced nodes.

-

Regulatory & Sustainability Readiness: PFAS and related regulatory actions are moving from regional to global relevance. Companies should accelerate transition programs toward low- or no-PFAS process chemistries and invest in wastewater treatment/monitoring to limit downstream compliance exposure.

-

M&A and Partnership Playbook: The market exhibits high concentration among incumbents with specialized know-how. Targeted partnerships, minority investments, or bolt-on acquisitions of niche photosensitizer specialists can be faster routes to capability than greenfield development.

-

Cost-to-Serve Optimization: As photosensitizers represent a meaningful share of photoresist raw-material volume, procurement levers — long-term offtakes, joint development agreements, and co-financed capacity expansions — can materially improve margin profiles for both suppliers and buyers.

What PW Consulting’s report delivers (actionable, not academic)

The full study is designed as an operator’s playbook for 2026: it combines quantitative forecasting with practical tools to inform capital allocation, partnership selection, and risk mitigation. Key deliverables include:

-

Executive dashboards synthesizing market growth scenarios and sensitivity analyses that link node adoption curves to photosensitizer demand.

-

Supplier risk matrix and qualification timeline templates tailored to EUV and sub-5nm transitions — including recommended test protocols to accelerate qualification cycles.

-

Regulatory heatmaps and mitigation plans addressing PFAS scrutiny, effluent management, and likely regional regulatory trajectories through 2032.

-

Commercial playbooks for procurement, including contracting templates, inventory heuristics, and sample supplier negotiation language for joint development and capacity reservation.

-

Investment prioritization frameworks that score opportunities across technology readiness, addressable demand, and exit optionality for M&A or venture groups.

Competitive dynamics: who to watch and why

The photosensitizer supply ecosystem remains anchored by a small number of highly capable specialty-chemicals firms with deep process expertise and customer intimacy. Several corporate profiles merit particular attention in 2026 strategic planning:

-

Tokyo Ohka Kogyo (TOK): A leading global photoresist supplier with active expansion in EUV-capable production. Recent facility investments indicate deliberate capacity hedging for next-generation nodes and reinforce TOK’s position as a reliable strategic partner for fabs moving to EUV.

-

JSR Corporation: Continues to push high-resolution resist chemistry innovation, with a new EUV-targeted product family launched to address sub-5nm patterning challenges. Their roadmap suggests a strong focus on collaborative development with leading foundries.

-

FUJIFILM (Electronic Materials & Wako): Offers broad photoresist portfolios and high-purity photosensitizer supplies. Their vertically integrated stance allows rapid iterations between resist formulation and photosensitizer tuning — a competitive advantage for customers seeking shortened qualification cycles.

-

Shin-Etsu Chemical: A stalwart in ArF and immersion resists with recent product introductions aimed at advanced DRAM nodes; their incremental innovation reduces risk for major memory manufacturers.

-

DuPont and Merck (EMD): Global chemical leaders with technology depth and supply-chain reach, well positioned to serve multinational fabs and to support scale-ups for new chemistries.

-

Specialist players (Toyo Gosei, FUJIFILM Wako, Allresist and niche firms across Asia and Europe): These firms are often the source of chemistry breakthroughs and offer acquisition or partnership upside for buyers seeking differentiated PAG/PBG capability.

Recent industry developments reinforce these themes: facility expansions focused on EUV-compatible resists, the launch of new high-resolution EUV products, and continued conference-level knowledge sharing on photopolymer science. These moves signal both demand momentum and a strategic race to lock in qualified chemistries as fabs bring sub-5nm capacity online.

Risk landscape and mitigation

-

Regulatory: The PFAS issue is no longer hypothetical. Reported PFOS concentrations in some wastewater streams have driven increased monitoring and potential restrictions. Firms should accelerate alternatives screening and invest in analytical capabilities to validate sub-ppm impurity targets.

-

Geopolitical/Supply: High-end resists and associated photosensitizers remain dominated by a small group of suppliers concentrated in specific geographies. Scenario planning should include export control shocks and accelerated localization strategies for critical materials.

-

Technical: Advanced nodes impose stringent impurity and outgassing thresholds. Buyers need to treat photosensitizer qualification as a joint engineering project with suppliers rather than a transactional procurement event.

Practical 90/180/365-day roadmap for executives

-

First 90 days: Commission a supplier-risk assessment, identify single points of failure for EUV-relevant chemistries, and start priority conversations with incumbent suppliers to secure short-term supply and initiate co-development agreements where needed.

-

Next 180 days: Run technical co-validation pilots for prioritized photosensitizer systems, finalize environmental compliance audits, and model the P&L impact of alternative chemistry adoption and inventory strategies.

-

Within 365 days: Execute strategic partnerships, finalize contingency supplier panels, and integrate low-PFAS chemistries into product roadmaps with a clear path to qualification across key fabs.

Where PW Consulting adds unique value

Unlike generic market briefs, this study connects market-size trajectories to practical execution tools: supplier qualification templates, chemistry-performance scorecards, regulatory heatmaps, and an investment-ranking matrix built for board-level prioritization. Our analysis blends primary interviews with materials scientists, purchasing directors, and fab process engineers, creating an actionable bridge between chemistry R&D and procurement strategy.

Next steps and how to access the full intelligence

This preview is intended to frame the strategic choices that will define winners and losers in 2026. The full PW Consulting Photoresist Photosensitizer Market report includes the complete forecast model, scenario-based demand curves, supplier benchmarking with contactable diligence notes, and downloadable implementation templates. For organizations making 2026 capital and sourcing decisions — particularly those engaged in EUV deployment, DRAM scaling, or advanced packaging — the full report provides the granular segmentation, supplier scorecards, and regulatory-compliance playbooks necessary to move from strategy to execution.

To obtain the complete report and our accompanying strategic workshop offer for executive teams, please visit the PW Consulting report landing page or contact our industry advisory desk. Early subscribers are offered a complimentary 90-minute strategy session to align the report’s insights with their 2026 planning cycles.

For detailed analysis of this topic, please visit the official page: Photoresist Photosensitizer Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.