PW Consulting: Drone Inspection System Market to Skyrocket at 18.5% CAGR, Reaching USD 57.26 Billion by 2032

Drone Inspection System Market: Strategic Imperatives for 2026 — PW Consulting Industry Brief

As enterprises accelerate infrastructure digitalization, the drone inspection system market has entered a phase of strategic opportunity and operational maturity. PW Consulting’s latest market study — with a 2025 base year and a forward-looking horizon through 2032 — synthesizes five years of historical performance with robust scenario-based forecasts to equip boards, chief officers, and line managers for decisive investment in 2026. The headline picture is clear: after rising rapidly through the early 2020s, the market is set to continue expanding at a compound annual growth rate of 18.5% over the forecast period, moving from mid‑double‑digit billion-dollar scale in 2025 toward a multi‑tens‑of‑billions market by 2032. This pace creates a narrow window for market entry, capability consolidation, and platform leadership.

Drone Inspection System Market

Why this matters for 2026 decision cycles

-

Time-bound advantage: With rapid adoption among capital-intensive sectors (energy, utilities, construction, mining and others), first movers who align procurement, regulation, and operational integration in 2026 will realize outsized economic and safety benefits by 2028–2030.

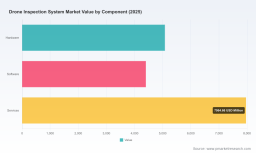

Drone Inspection System Market -

Platform convergence: Hardware, software, and services are converging into vertically integrated offerings. Buyers must avoid vendor lock-in risks while capturing value from combined systems — data capture hardware plus analytics-led services are where margin pools are migrating.

Drone Inspection System Market -

Regulatory inflection: Emerging rules for BVLOS, Remote ID, and AI-enabled autonomy are reshaping deployment viability. Organizations that design compliance into operational blueprints now will reduce time-to-scale as regulations mature.

What the PW Consulting report delivers (practical, actionable content)

-

Market sizing and scenarios: Our methodology, transparent assumptions, and sensitivity analyses provide enterprise-grade TAM/SAM/SOM frameworks calibrated for 2026 procurement planning and 3‑ to 5‑year budget cycles.

-

Operational playbooks: Step‑by‑step guides for pilot-to‑scale transitions, including sample BVLOS readiness checklists, tether and battery-swap operational designs, and site-level risk matrices.

-

Procurement and vendor selection tools: RFP templates, scoring rubrics, and total cost of ownership (TCO) models with customizable inputs so teams can compare “apples-to-apples” across hardware, software, and managed service options.

-

Technology evaluation: Comparative frameworks for sensing suites (visual, thermal, RTK/L1/L2 GNSS, LiDAR), autonomy stacks (onboard vs. cloud), and data management platforms — including guidance on integration with GIS/asset management systems.

-

Regulatory and compliance roadmap: Practical pathways to BVLOS, Remote ID compliance, and approaches to satisfy evolving AI risk assessments in different jurisdictions.

-

Commercial strategies: Go‑to‑market templates for vendors and procurement playbooks for asset owners (capex vs. opex, DaaS, pure service contracting), plus M&A and partnership blueprints for rapid capability acquisition.

-

Vendor scorecards and case studies: Confidential, evidence‑based assessments of leading vendors across reliability, autonomy, data fidelity, service coverage, and enterprise integrations.

Competitive landscape — what leaders and challengers are doing

The market exhibits moderate concentration: our CR3 and CR5 metrics indicate that top three vendors control just over a third of market revenue, while the top five approach half the market. This leaves significant room for specialized providers and new entrants to displace incumbents in targeted niches.

-

SZ DJI Technology: Continues to lead on platform scale and payload flexibility, offering enterprise-grade airframes with visual, thermal and high‑precision RTK payloads and automated data collection workflows. Their strength is hardware ubiquity and ecosystem integration.

-

SkySpecs: Specializes in autonomous wind-turbine blade inspection and analytics. Their focus on drivetrain diagnostics and vertical specialization demonstrates how deep domain expertise can command premium pricing and repeatable contracts in renewable energy.

-

Cyberhawk: Focused on critical infrastructure and complex asset classes, combining advanced sensors with aerial data management platforms. Their model highlights the importance of combining inspection capture with enterprise data pipelines.

-

Skydio: Differentiates through AI-powered autonomy and obstacle avoidance, enabling repeatable missions in challenging environments. Their software-centric approach shows how autonomy can reduce labor costs and improve consistency.

-

Flyability: Niche leadership in collision-tolerant indoor inspection solutions addresses the persistent need for confined-space, high-risk asset checks — an example of product innovation unlocking new inspection workflows.

-

Percepto: Offers Drone‑in‑a‑Box and persistent monitoring solutions for continuous site oversight, illustrating the shift from point-in-time inspections to recurring, automated monitoring regimes.

-

Terra Drone: Blends platform and cloud services with cost-focused indoor inspection hardware, showing how regional engineering and local go‑to‑market strategies can lower barriers for operators.

-

Censys: Recent public BVLOS demonstrations underscore the viability of long-range missions over utility corridors and the commercial signaling effect of live demos for regulatory acceptance.

-

Drone Volt and AeroVironment: Provide specialized airframes and solutions for industrial customers; their presence reflects the ongoing importance of tailored hardware suppliers in enterprise stacks.

Taken together, these profiles illustrate a market where differentiation is achieved through combinations of autonomy, domain specialization, persistent monitoring capabilities, and data‑centric services rather than hardware alone.

Regulatory and operational headwinds (and how to plan around them)

-

Enforcement and safety: The tightened enforcement posture by the FAA in 2026 — requiring legal actions where drone operations threaten public safety or violate airspace rules — elevates the importance of robust operational governance. Operators must adopt legal counsel engagement, hardened SOPs, and compliance audits as default components of any deployment.

-

BVLOS normalization: The FAA’s proposed Part 108 performance-based rules and the reopening of comment periods mean that organizations should build BVLOS pilots that produce regulatory artifacts (detect-and-avoid validation, risk assessments). These artifacts accelerate approval pathways under new performance-based regimes.

-

Remote ID and data governance: Mandatory Remote ID enforcement and the EU’s harmonized SORA updates — now incorporating AI risk assessments — make identity, telemetry security, and model explainability operational requirements. Security-by-design must be integrated into vendor evaluations and data retention policies.

-

Hardware constraints: Battery endurance remains a tangible technical constraint. Our operational playbooks prioritize hybrid architectures (tethered systems, battery swaps, redundant fleets), mission sequencing, and localized staging to mitigate endurance limits and maximize inspection coverage.

Recent signals to watch

-

Censys’ February 2026 public BVLOS demonstration — a long-range dual-leg mission — materially advances the narrative around infrastructure-scale BVLOS feasibility and will influence utility procurement timetables for 2026 pilots.

-

Terra Drone’s 2025 launch of an affordable Japan-made indoor inspection drone signals continued innovation at the cost-performance frontier for confined-space inspection needs.

-

Regulatory moves in 2025–2026 across FAA and EASA will increasingly favor operators who can demonstrate documented safety cases and AI governance frameworks.

Recommended 2026 playbook for enterprise leaders

-

Prioritize pilots that create regulatory-grade evidence. Design pilot programs with traceable risk assessments, detect-and-avoid validation, and data retention to accelerate BVLOS approvals.

-

Shift procurement evaluation criteria from unit price to system economics: include data integration costs, analyst time savings, and lifecycle maintenance in TCO models.

-

Adopt a composable architecture: combine best-in-class autonomy, sensor suites, and cloud analytics to avoid vendor lock-in and preserve optionality as AI and regulation evolve.

-

Invest in operational maturity: build in governance, insurance, and incident response capabilities before scaling operations to minimize regulatory friction and liability.

-

Explore partnership and M&A pathways: identify niche vendors with domain expertise as targets for strategic acquisition or exclusive partnership to accelerate capability acquisition.

-

Plan for persistent monitoring: design workflows that transition from periodic inspection to continuous oversight where ROI favors anomaly detection and predictive maintenance.

Next steps — how to use PW Consulting’s analysis

PW Consulting’s full Drone Inspection System Market report is structured as an operational kit for 2026 decision-making: it delivers validated market sizing, scenario outcomes, vendor scorecards, procurement templates, and tactical playbooks. The executive summary and methodology sections give immediate inputs for budgeting and board-level discussions, while the annexes include downloadable templates and vendor RFP language for procurement teams. In keeping with our “preview” approach, we present strategic findings and implications here while preserving the detailed segment tables, region- and application-level forecasts, and proprietary vendor scoring matrices for the full report.

For organizations planning capex and opex commitments in 2026, the choices made this year — which pilots to run, which partners to qualify, how to structure data contracts, and how to evidence safety for BVLOS — will determine operational advantage as the market accelerates. PW Consulting’s analysis isolates the decisions that create optionality and reduce downside risk; the full report contains the detailed models and templates needed to operationalize those recommendations.

Contact and access

To obtain the full report, vendor scorecards, and deployment toolkits that underpin the strategic recommendations summarized here, visit PW Consulting’s research portal or contact our industry team to arrange a briefing. We provide tailored executive workshops that translate the market scenarios into specific 12–36 month roadmaps for enterprise deployment or vendor go‑to‑market acceleration.

For detailed analysis of this topic, please visit the official page: Drone Inspection System Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.