PW Consulting: 4,4'-Diphenylmethane Diisocyanate Market to Expand at 5.18% CAGR Through 2032, New Report Says

44 Diphenylmethane Diisocyanate (MDI) Market — Strategic Outlook 2026: PW Consulting Report Preview

Executive summary

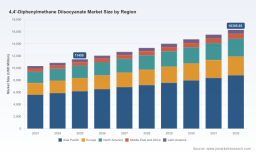

PW Consulting today releases a preview of its 44 Diphenylmethane Diisocyanate (MDI) Market report, an action-oriented research asset designed to inform board-level and operational decisions across the polyurethane value chain in 2026. Built on a 2025 base year with historical analysis covering 2020–2025 and a forecast horizon to 2032, the model projects the global MDI market to grow from an observed USD 11,450.0 Million in 2025 to USD 16,305.65 Million by 2032 — a compound annual growth rate (CAGR) of 5.18% over the 2026–2032 forecast period. The market remains concentrated, with the top three producers accounting for a majority share (CR3 ~54.2%) and the top five controlling over four-fifths of supply (CR5 ~82.15%).

44 Diphenylmethane Diisocyanate Market

Why this report matters for 2026 decisions

- Pricing & commercial strategy: with recent supplier-driven price adjustments and volatile feedstock costs, executives need granular scenarios to set list/contract prices, index clauses, and short-to-medium-term margin recovery plans.

- Procurement & hedging: buyers and upstream players require cost-pass-through models and feedstock sensitivity analyses to design procurement contracts and hedging strategies during periods of benzene/aniline price volatility.

- Capex & capacity planning: manufacturers and investors must align capacity expansions or brownfield debottlenecking with realistic demand trajectories, technology choices, and regional regulatory risk.

- Regulatory compliance & product stewardship: evolving policy actions are reshaping acceptable formulations and go-to-market strategies for spray foam and other end-uses — an immediate compliance playbook is essential.

- M&A and JV prioritization: market concentration, differentiated product positioning, and feedstock exposure create identifiable acquisition targets and partnership candidates; the report tiers candidates and quantifies value levers.

What the report delivers — actionable, not academic

PW Consulting’s MDI report is designed as a practical toolkit for decision-makers. It combines an auditable market model with scenario simulations and execution roadmaps, including:

44 Diphenylmethane Diisocyanate Market

- Integrated demand model across applications and regions (historical 2020–2025 and forecast 2026–2032), with transparent assumptions and sensitivity toggles for price, GDP, construction activity, and automotive production intensity.

- Supply-side overlay covering global production assets, utilization curves, planned start-ups, and potential outage risks — with supplier-level maps and concentration metrics to support contract negotiation and contingency planning.

- Cost build-ups and margin stress tests driven by feedstock dynamics (aniline, benzene) and energy inputs, enabling true-to-market gross margin simulations under multiple pricing regimes.

- Regulatory risk matrix assessing trade remedy actions, product stewardship requirements, and jurisdictional compliance obligations, accompanied by prescribed mitigation pathways.

- Commercial playbooks for producers, distributors, and OEMs: value-based pricing, contractual clauses for pass-through mechanics, inventory and logistics optimization, and downstream co-development opportunities.

- M&A playbook: valuation heuristics tailored to MDI assets, integration risk checklists, and a prioritized target list based on strategic fit and exposure.

- Interactive dashboards and downloadable data packs for rapid scenario iteration by finance, procurement, and strategy teams.

Competition and strategic positioning

The MDI industry is dominated by a small set of integrated chemical majors and regional leaders. PW Consulting’s assessment highlights several strategic archetypes among incumbent suppliers:

44 Diphenylmethane Diisocyanate Market

- Integrated global champions with scale and asset flexibility (examples include Wanhua Chemical Group, BASF SE, Covestro AG). These players leverage integrated upstream and downstream platforms to optimize margins across cyclical swings.

- Regional specialists with focused cost advantages and customer intimacy (e.g., Kumho Mitsui, Tosoh). These companies often capture profit pools in adjacency markets where local logistics and service are differentiators.

- System providers and formulators (e.g., Huntsman, Dow) that combine MDI supply with formulated systems and technical services — enabling higher value capture downstream.

Recent commercial moves within the supplier base have material implications for pricing and availability. Notable developments include supplier-led price increases announced in 2025 and 2026 that signal an effort to restore margins in the face of higher feedstock costs. These supplier actions should be read as part of a broader rebalancing between demand elasticity, inventory strategy, and regulatory pressure — not as isolated events.

Feedstock and supply-chain dynamics

Feedstock economics remain the single largest determinative factor for MDI cost and pricing. PW Consulting’s model integrates the latest input-cost indicators: for example, aniline prices have shown upward pressure in early 2026, driven by benzene cost trends and tighter aromatic markets. These movements materially affect producer cost curves and the cadence of pass-through into finished product prices. The report provides a multi-layered view of feedstock exposure by plant, supplier contractual terms, and logistics chokepoints, enabling risk-weighted procurement strategies and inventory policy design.

Regulatory developments and product stewardship

Regulatory actions that emerged in 2025–2026 introduce new compliance layers for MDI producers and downstream formulators. Preliminary trade determinations and state-level product stewardship mandates are changing commercial dynamics across several high-value end-uses. PW Consulting’s regulatory module quantifies potential tariff and non-tariff impacts, models compliance cost scenarios, and outlines remediation paths — from reformulation timelines to customer notification and labeling programs.

Implications of recent market events

- Supplier price announcements (multiple rounds during 2025–2026) reflect a coordinated market response to feedstock inflation and capacity utilization dynamics; buyers should prepare for tiered contract strategies and index-linked pricing to mitigate volatility.

- Feedstock inflation has accelerated cost push through the value chain; procurement must evaluate forward coverage vs. spot exposure using the model’s sensitivity analyses.

- Trade and product-level regulatory actions increase the premium on traceability, testing, and compliant formulations — areas where early investments reduce downstream commercial disruption.

Strategic recommendations for 2026

For C-suite and functional leaders shaping strategies in 2026, PW Consulting recommends a pragmatic, phased approach:

- Short term (0–12 months): implement dynamic pricing and contract clauses tied to agreed feedstock indices; increase visibility into supplier inventories and logistical lead times; initiate targeted cost-to-serve reviews for high-value customers.

- Medium term (12–36 months): re-evaluate capex cadence — prioritize brownfield debottlenecking and modular expansions over greenfield builds unless supported by long-term offtake contracts; invest in downstream system capabilities to capture value beyond commodity MDI.

- Long term (36+ months): pursue strategic partnerships or M&A to secure feedstock upstream exposure, diversify manufacturing footprints, and lock in technology differentiation (high-purity grades, low-emissions processes, circular chemistries).

- Risk management: adopt a layered hedging program combining physical coverage, term contracts with pass-through mechanics, and selective financial hedges; maintain a regulatory watchboard and preparedness playbook for jurisdictional compliance shifts.

How to use the full report

This preview is intentionally diagnostic: it highlights the analytical depth and decisioning frameworks available in PW Consulting’s full 44 Diphenylmethane Diisocyanate Market report while withholding granular sub-segmentation datasets to protect the report’s proprietary value. The full deliverable provides:

- Downloadable market models and editable scenario workbooks.

- Granular segmentation by region, product type, and application with time-series data and underlying assumptions (useful for contract negotiations, investment memos, and internal planning).

- Company-level profiles with asset maps, recent moves, and strategic SWOTs, plus a prioritized target list for M&A or partnerships.

- Customizable dashboards for procurement, finance, and strategy teams to stress-test plans under regulatory, price, and demand shocks.

Organizations that need to operationalize decisions in 2026 — whether to renegotiate supply contracts, greenlight an investment, or reposition a product portfolio in response to regulatory change — will find the full report’s models and roadmaps indispensable. To request access to the full dataset, scenario models, and executive briefings, please contact PW Consulting via our report distribution channels.

Closing perspective

MDI remains a structurally important chemical within polyurethane value chains, with steady growth driven by insulation, industrial systems, and engineered elastomers. The 2026 decision calendar will be shaped by a confluence of higher feedstock costs, supplier price discipline, regulatory tightening, and strategic consolidation among incumbents. PW Consulting’s report turns these macro forces into executable options — enabling leadership teams to move from reactive posture to proactive advantage.

For detailed analysis of this topic, please visit the official page: 44 Diphenylmethane Diisocyanate Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.