PW Consulting: MMA‑Triazine H2S Scavengers Market Set to Expand at a 6.19% CAGR Through 2032

MMA Triazine H2S Scavengers Market — Strategic Outlook to 2026 and Beyond

Executive snapshot

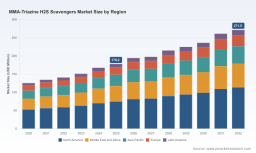

PW Consulting’s latest market study on MMA (monomethylamine) triazine H2S scavengers provides a forward-looking framework for 2026 corporate decision-making. Using 2025 as the base year and a historical window covering 2020–2025, the report models the market through 2032. Our forecast shows a steady expansion at a compound annual growth rate (CAGR) of 6.19%, reflecting the combined effects of upstream sour hydrocarbon activity, midstream integrity programs, and tightening environmental and safety standards. The market has grown materially since 2020 and is projected to roughly one-and-a-half times its 2025 scale by the end of the forecast horizon—evidence of durable, investable demand.

Mma Triazine H2S Scavengers Market

Why this matters for 2026 decision-makers

- Buy-side optimization: Procurement teams must recalibrate sourcing strategies to balance working capital, inventory buffers and activity-level specifications of scavenger formulations.

- Manufacturing & supply chain resilience: Specialty chemical players and oil & gas operators should test localized blending and contingency sourcing as trade measures and feedstock availability continue to shape landed costs.

- Regulatory alignment: Waste handling and by-product classification changes in key jurisdictions will materially affect operating expenses and end-of-life logistics for spent scavenger material.

- M&A and partnership signalling: The market structure presents targeted opportunities for asset-light suppliers, toll-blenders and feedstock integrators to accelerate portfolio coverage.

Market dynamics shaping near-term strategy

Several forces converge to define opportunity and risk in the MMA triazine H2S scavenger market in 2026:

Mma Triazine H2S Scavengers Market

- Feedstock dependence and synthesis constraints. Production chemistry for MMA-triazine rests on condensation pathways using monomethylamine and formaldehyde. Feedstock availability and pricing volatility propagate through lead times and supplier margins—making upstream visibility and strategic sourcing non-negotiable for both producers and large consumers.

- Regulatory headwinds around by-products. Triazine-derived solids formed during scavenging reactions (commonly termed dithiazines and related residues) are the subject of evolving waste-classification frameworks in multiple jurisdictions. Changing classification and landfill restrictions will alter total cost of ownership for popular formulations and create a premium for lower-residue chemistries or effective on-site handling solutions.

- Safety and emissions compliance. Continued emphasis on worker exposure and emissions thresholds in sour gas operations sustains demand for reliable scavengers as an operational control. This regulatory backdrop also raises the bar for supplier documentation, traceability and third-party validation.

- Trade policy and localized production. Recent tariff adjustments in key markets have led several suppliers to accelerate local production or blending capacity to preserve competitiveness. Expect strategic investments in near-market toll blending and flexible packaging to reduce landed-cost sensitivity.

- Formulation and application evolution. End-users are increasingly selecting scavenger formulations not only on unit activity but on total lifecycle impacts—handling ease, corrosion profile, downstream contamination risk and waste footprint. This is propelling demand for application-specific chemistry variants and on-site custom blending services.

Segmentation — what the report analyzes (without giving away proprietary splits)

PW Consulting’s report structures the market along the familiar axes of region, formulation type and application, then overlays practical decision tools for each slice. Rather than reproducing discrete allocation tables here, the report demonstrates how those segmentation layers interact and where margin pools actually live. Key analytical features include:

Mma Triazine H2S Scavengers Market

- End-to-end TCO models that compare activity-level chemistry choices across upstream, midstream and downstream operating contexts.

- Scenario analysis for demand sensitivity under differing sour-gas production and regulatory scenarios across the forecast window.

- Provider capability mapping that links formulation types (e.g., water-dominant vs. solvent-dominant systems) to deployment realities such as injection hardware compatibility and waste management.

Competitive landscape — leading players and what differentiates them

The market exhibits moderate concentration by value, with a measurable share controlled by a handful of larger suppliers and a diverse long tail of regional manufacturers. This structure creates both opportunities for consolidation and niches for specialized service providers.

- Foremark Performance Chemicals (League City, Texas; https://foremarkperformance.com) — Foremark’s branded PureMark® family targets both mercaptan removal and liquid hydrocarbon streams. Their positioning emphasizes field-proven formulations and packaged solutions for operators seeking low-risk swaps.

- Hexion Inc. (Columbus, Ohio; https://www.hexion.com) — Hexion leverages its broader amine and triazine expertise to offer a range of MEA- and MMA-based chemistries. Their strength lies in regulatory-compliant documentation and scale manufacturing capabilities.

- Q2 Technologies (USA; https://q2technologies.com) — A wholesale specialist known for high-activity MEA-triazine products and custom additive packages; Q2 is also an early mover in supporting MMA-triazine adoption across phases.

- Venus Ethoxyethers (Goa, India; https://www.venus-goa.com) and Jay Dinesh Chemicals (India; https://www.jaydinesh.com) — These regional manufacturers compete on cost and speed-to-market, serving local oil & gas clusters and global customers via competitive export offerings.

- International Chemical Group (ICG; https://www.intlchemgroup.com), Novamen Inc. (Canada; https://www.novamen.ca), OneCor (USA; https://onecor.com), and Geocon Products (India; https://www.geoconproducts.com) — Each brings variant strengths: activity-level customization, on-site blending for large-volume customers, and targeted field support for Gulf and North American operations.

PW Consulting’s supplier scorecards assess chemistry breadth, documentation rigor, supply security, on-site support capability and environmental handling programs. Those wishing to make sourcing decisions in 2026 will want to prioritize suppliers that combine validated field performance with demonstrated waste-management solutions.

Operational playbook for 2026

Companies that move early on the following actions will mitigate risk and preserve margin as the market evolves:

- Validate activity targets in controlled field trials. Lab-only equivalence often misses scale-dependent by-product formation and injection-packing effects—budget for short, instrumented pilot runs before full-scale conversion.

- Lock flexible contracting with option tranches. Include clauses for activity, residue levels and waste-recovery support to align incentives between buyer and supplier.

- Invest in near-market blending or toll-manufacturing partnerships. This reduces exposure to trade measures and can shorten lead times for tailored formulations.

- Design-for-disposal: incorporate on-site solid-removal equipment and qualified third-party handlers into procurement evaluation to control downstream compliance costs.

- Set up cross-functional governance. Procurement, HSE, production and field engineering must jointly validate supplier claims and sign off on trial results.

M&A, investment and R&D priorities

The sector’s competitive profile—where a few firms hold a significant but not dominant share—creates a fertile environment for strategic transactions and targeted investment. Priority plays include:

- Toll-blending footprints in tariff-sensitive markets: acquiring small, well-located blending assets can neutralize landed-cost disadvantages quickly.

- Vertical integration into key feedstocks or contract manufacturing agreements with monomethylamine producers—this is especially valuable for suppliers aiming to stabilize margins and guarantee activity payloads.

- R&D focused on lower-residue scavengers and on-site degradation or capture solutions. Proprietary approaches to minimize persistent solid formation will be a differentiator as waste regulations tighten.

- Data-enabled service models that pair material supply with monitoring, dosing optimization and residue analytics—moving from a product sale to a performance contract can unlock premium pricing.

What the full PW Consulting report delivers

Our 200+ page deliverable is built for practitioners who need executable intelligence in 2026. Highlights include:

- Transparent methodology and a live financial model covering historicals, 2026 baseline and 2032 forecasts with scenario toggles.

- Supplier scorecards and contact maps, including capability matrices for chemical activity, documentation and service levels.

- Operational playbooks: procurement templates, pilot-test protocols and a checklist for environmental and field acceptance.

- Regulatory impact matrix and waste-handling decision tree calibrated against recent policy shifts in major jurisdictions.

- Case studies that quantify lifecycle costs in upstream, midstream and downstream environments—illustrating where value is captured and lost.

Consistent with our “trailer” approach, the executive narrative here summarizes the most actionable themes without reproducing the report’s proprietary segmentation tables and supplier benchmarking scores, which are reserved for the full report.

Next steps for leaders

For organizations evaluating exposure to sour hydrocarbon operations, PW Consulting recommends three immediate moves for 2026:

- Commission a 90-day pilot and TCO assessment using at least two distinct chemistry suppliers; require vendor data on residue formation and disposal pathways.

- Perform a tariff and landed-cost stress test to determine the threshold for localized blending investment or partner selection.

- Map regulatory trajectories for waste classification in your primary operating jurisdictions and engage legal/HSE counsel to update contracts and contingency plans.

For a detailed strategic brief, supplier scorecards and the full financial model referenced above, please consult the PW Consulting MMA Triazine H2S Scavengers Market report on our publications page. The full report contains the granular segmentation and benchmarking data necessary to convert insight into high-confidence 2026 decisions.

For detailed analysis of this topic, please visit the official page: Mma Triazine H2S Scavengers Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.