PW Consulting Forecast: Drone Inspection Systems to Skyrocket at an 18.5% CAGR Through 2032

Drone Inspection System Market 2026: Strategic Preview from PW Consulting

As organizations move from experimental pilots to volume deployments of unmanned aerial inspection, 2026 has become a pivot year for strategic decisions that will determine competitive position for the rest of the decade. PW Consulting’s latest Drone Inspection System Market report—anchored on a rigorous base year (2025) and a forecast window through 2032—distills market sizing, technology trajectories, regulatory inflection points, and supplier economics into a practical playbook for executives, procurement leads, and program managers. In short: this is not academic research. It is a roadmap for decisions you must make in 2026.

Drone Inspection System Market

Market at a glance: scale, pace, and concentration

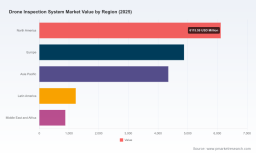

The market for drone inspection systems is expanding rapidly. Our model shows a robust compound annual growth rate (CAGR) of 18.5% across the forecast period, driven by accelerating asset digitization in energy, infrastructure, and heavy industry, alongside maturing autonomy and data analytics stacks. On the macro scale, the market value transitions from a strong 2025 base to more than triple that scale by 2032—an expansion that creates both commercial opportunity and execution risk for late movers.

Drone Inspection System Market

Industry structure remains mid-fragmented. The top three providers account for roughly one-third of the market by revenue, while the top five approach half of market share—indicating meaningful but not overwhelming concentration. That market structure produces opportunities for specialist players and system integrators to win business via vertical expertise, while also providing scale advantages to platform leaders.

Drone Inspection System Market

Why this report matters for 2026 decisions

- Procurement realism: We convert vendor claims into deployable cost models and time-to-value curves—so you can compare acquisition vs. “as-a-service” alternatives on consistent, defensible metrics.

- Regulatory scenarios: We map three near-term regulatory outcomes (conservative, enabling, and hybrid) and quantify their practical implications for BVLOS operations, Remote ID compliance, and cross-border deployments.

- Operational readiness: The report includes playbooks for pilot-to-scale maturity, addressing crew and skill requirements, data pipelines, and maintenance throughput to help you avoid common scaling failures.

- Vendor engagement kit: Our supplier evaluation matrix and contract checklist let teams accelerate RFP cycles while preserving negotiation leverage—particularly important as platform-IP and data-rights clauses become contentious.

Key drivers and constraints shaping 2026 strategies

Four dynamics are shaping 2026 decisions. First, autonomy and AI are shifting value from hardware toward software, analytics, and recurring services. Second, infrastructure owners increasingly demand continuous monitoring patterns (not episodic inspections), favoring “Drone-in-a-Box” and automated mission frameworks. Third, regulatory modernization—most notably developments in the United States and Europe—will define the practical timeline for widespread Beyond-Visual-Line-of-Sight (BVLOS) operations. Fourth, physical limits remain real: battery endurance constraints (typical flight windows remain bounded by current chemistry and payload trade-offs) materially affect mission architecture and operational cost.

Regulatory milestones are already influencing procurement: updated FAA enforcement policies in 2026 heighten operational accountability, while proposed performance-based BVLOS rules (Part 108) and Remote ID requirements are shifting compliance and systems design. In parallel, EASA’s ongoing SORA evolution introduces AI-risk modules that will affect autonomous mission certification in Europe. These developments force buyers to bake regulatory resilience into contract terms and systems design rather than treating certification as an afterthought.

Competitive landscape — who to watch and why

The competitive environment combines global platform suppliers, autonomous specialists, indoor-capable manufacturers, and service-led integrators. Our competitive analysis highlights strategic positioning rather than raw revenue figures—focusing on capability adjacency, go-to-market models, and likely consolidation paths.

- SZ DJI Technology Co., Ltd. (Shenzhen) remains a dominant hardware and payload supplier with a broad enterprise foothold. Their enterprise platforms—paired with thermal, RTK, and high-resolution imaging—continue to set the baseline for many inspection workflows. Expect DJI to reinforce integration partnerships with software vendors to protect platform stickiness.

- Skydio, Inc. (Redwood City) brings advanced autonomy and obstacle-avoidance capabilities that excel in complex asset environments. Skydio’s trajectory is toward deeper verticalization—embedding autonomy within workflow integrations for utilities and infrastructure.

- Percepto Ltd. and similar Drone-in-a-Box providers are accelerating moves into continuous monitoring. Their value proposition is operational continuity with lower recurring labor cost; their success will be determined by service SLAs and integration with site OT/IT systems.

- Specialists such as SkySpecs, Cyberhawk, and Flyability are differentiating on domain expertise—wind, critical infrastructure, and confined spaces respectively—turning sector knowledge into higher-margin services and data products.

- Regional integrators and long-range innovators (e.g., Censys Technologies, Terra Drone) are proving flight concepts—BVLOS missions and affordable indoor platforms—that change the economics for linear assets and enclosed infrastructures.

- Legacy aerospace and UAS suppliers (AeroVironment, Drone Volt) remain relevant where certifiable platforms, supplier reliability, and defense-grade supply chains are required.

Recent developments underscore these trends: a public, long-range BVLOS demonstration by Censys in early 2026 validated extended-mission concepts for critical infrastructure, while Terra Drone’s product launches for indoor inspection further commoditize affordable, purpose-built platforms. These events are symptomatic: technical feasibility is moving faster than many procurement and regulatory processes can adapt.

How senior leaders should translate insight into action in 2026

- Define pilot success metrics today: Use financial and operational KPIs tied to inspection frequency, defect-detection uplift, and downstream maintenance savings. Avoid vague “efficiency” targets that fail to guide scale decisions.

- Build layered procurement strategies: Combine platform purchases for proprietary use cases with outcome-based contracts for extended monitoring. Manage vendor lock-in by specifying data export and interoperability clauses.

- Invest in data ops, not just drones: The real value is in measurement consistency, change detection, and integration with asset-management systems. Treat data pipelines, labeling, and model governance as first-class investments.

- Engage regulators early: Participate in BVLOS trials, submit practical use-cases during comment periods, and structure testbeds to inform site-specific risk cases. Regulatory engagement shortens deployment timelines and reduces unexpected compliance costs.

- Plan for incremental scale: Design for modular expansion—pilot, industrialize, and industrial-scale—so that each step delivers measurable ROI and lessons learned.

What the PW Consulting report delivers

PW Consulting’s full report is structured for operational uptake. Key deliverables include:

- Validated market-sizing models with sensitivity scenarios calibrated to regulatory outcomes and battery-technology trajectories;

- Supplier benchmarking across technology, service delivery, and commercial terms, plus a customizable vendor short-listing tool;

- Practical pilot-to-scale playbooks including staffing profiles, mission architectures, and procurement templates;

- Regulatory scenario matrices and a prioritized action checklist for legal, safety, and compliance teams;

- ROI calculators and contract clauses that reconcile hardware amortization, service fees, and expected maintenance savings;

- Case studies and real-world lessons from recent demonstrations and product launches that illuminate pitfalls and accelerants.

We intentionally present our findings to equip decision makers with both strategic framing and operational checklists—while preserving detailed segment-level tables and client-ready appendices for subscribers. The executive preview you are reading is designed to convey confidence and direction without disclosing the granular segment allocations that are reserved for the full report.

Closing: the strategic window for 2026

2026 is a year for pragmatic moves: secure demonstrable wins that validate your operating model, while establishing contractual and technical foundations for scale. Whether your priority is reducing inspection cycle time, improving defect detection, or moving toward continuous site monitoring, the choices you make this year—vendor commitments, data architecture, regulatory engagement—will determine which organizations capture disproportionate value from the rapid market expansion ahead.

PW Consulting’s Drone Inspection System Market report synthesizes market scale, competitive dynamics, regulatory risk, and deployment playbooks into a single, action-oriented reference. For teams responsible for procurement, operations, or strategy, the full report provides the granular scenario analysis and vendor intelligence required to convert 2026 momentum into sustainable advantage.

For detailed analysis of this topic, please visit the official page: Drone Inspection System Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.